[ad_1]

CatLane

Creator’s Notice: This two-part article is a really detailed evaluation of AGNC Funding Corp.’s (NASDAQ:AGNC) earnings assertion (technically talking, the corporate’s “consolidated assertion of complete earnings (loss)”). I proceed to carry out such a detailed quarterly evaluation for readers who wish to totally perceive AGNC’s ever-changing mortgage-backed securities (“MBS”)/funding portfolio and danger administration methods. The accounts/matters mentioned inside this collection of articles are additionally precious for any investor that has an curiosity throughout the fixed-rate company and broader mortgage actual property funding belief (mREIT) sector. For readers who simply need the summarized account projections, I might recommend to scroll right down to the “Conclusions Drawn” part close to the underside of every a part of the article.

Focus of Article:

The main focus of this text is to supply an in depth projection of AGNC’s complete earnings (loss) for the second quarter of 2022. Previous to outcomes being supplied to the general public on 7/25/2022 (through the corporate’s quarterly press launch), I wish to analyze AGNC’s consolidated assertion of complete earnings (loss) and supply readers a common route on how I imagine this current quarter has panned out. I imagine this quarter has a heightened degree of significance to readers as a result of current occasions surrounding the Federal Open Market Committee’s (“FOMC”) choice relating to financial coverage and sure world macroeconomic occasions which impacted the yield curve and the general market “throughout the board”.

Particularly, there was heightened significance relating to the FOMC’s choice relating to the Federal (“FED”) Funds Fee and actions throughout the London Interbank Supplied Fee (LIBOR). This contains the pretty current common flattening of the yield curve and pretty current notable rise in unfold/foundation danger. Within the case of AGNC (and company mREIT firms as an entire), unfold/foundation danger is just the connection of valuation fluctuations of sure investments (particularly company MBS) in relation to valuation fluctuations of spinoff devices/hedges (particularly rate of interest payer swaps, payer swaptions, and (brief) U.S. Treasury securities). As a result of size of the fabric lined, I imagine it’s mandatory to interrupt this projection article into two elements.

Aspect Notice: Predicting an organization’s accounting figures throughout the mREIT sector is often harder when in comparison with different sectors as a result of varied hedging and asset portfolio methods which are carried out by administration every quarter. As such, there are a number of assumptions used when performing such an evaluation. AGNC’s precise reported values might differ materially from my projected values inside this text as a result of unexpected circumstances (even when this has been a uncommon incidence since I started overlaying AGNC greater than 9 years in the past). Such variances might happen as a result of administration deviates from an organization’s prior enterprise technique and pursues a brand new technique that was not beforehand disclosed or anticipated. One other notable variance might happen as a result of variations of opinion relating to sure lifetime prepayment forecasts which have a excessive diploma of “managerial judgement”. Readers ought to concentrate on these potentialities. All projections inside this text are my private estimates and mustn’t solely be used for any investor’s shopping for or promoting selections. All precise reported figures which are above the imply of my account projections will likely be deemed an “outperformance” in my judgment. All precise reported figures which are beneath the imply of my account projections will likely be deemed an “underperformance” in my judgment. Until in any other case famous, all figures beneath are for the “three-months ended” (quarterly) timeframe.

By understanding the traits that occurred inside AGNC’s operations throughout the second quarter of 2022, one can apply this info to sector friends as nicely (in any case for comparative functions). As such, the dialogue/evaluation beneath is just not solely relevant to AGNC however to the fixed-rate company mortgage actual property funding belief (mREIT) sector as an entire. This contains, however is just not restricted to, the next fixed-rate company mREIT friends: 1) ARMOUR Residential REIT Inc. (ARR); 2) Cherry Hill Mortgage Funding Corp. (CHMI); 3) Dynex Capital Inc. (DX); 4) Invesco Mortgage Capital Inc. (IVR); 5) Annaly Capital Administration Inc. (NLY); 6) Orchid Island Capital Inc. (ORC); and 7) Two Harbors Funding Corp. (TWO). It must be famous CHMI and TWO are additionally thought of fixed-rate company + mortgage servicing rights (“MSR”) mREIT friends and may very well be categorised as a separate sub-sector.

Consolidated Assertion of Complete Earnings (Loss) Overview:

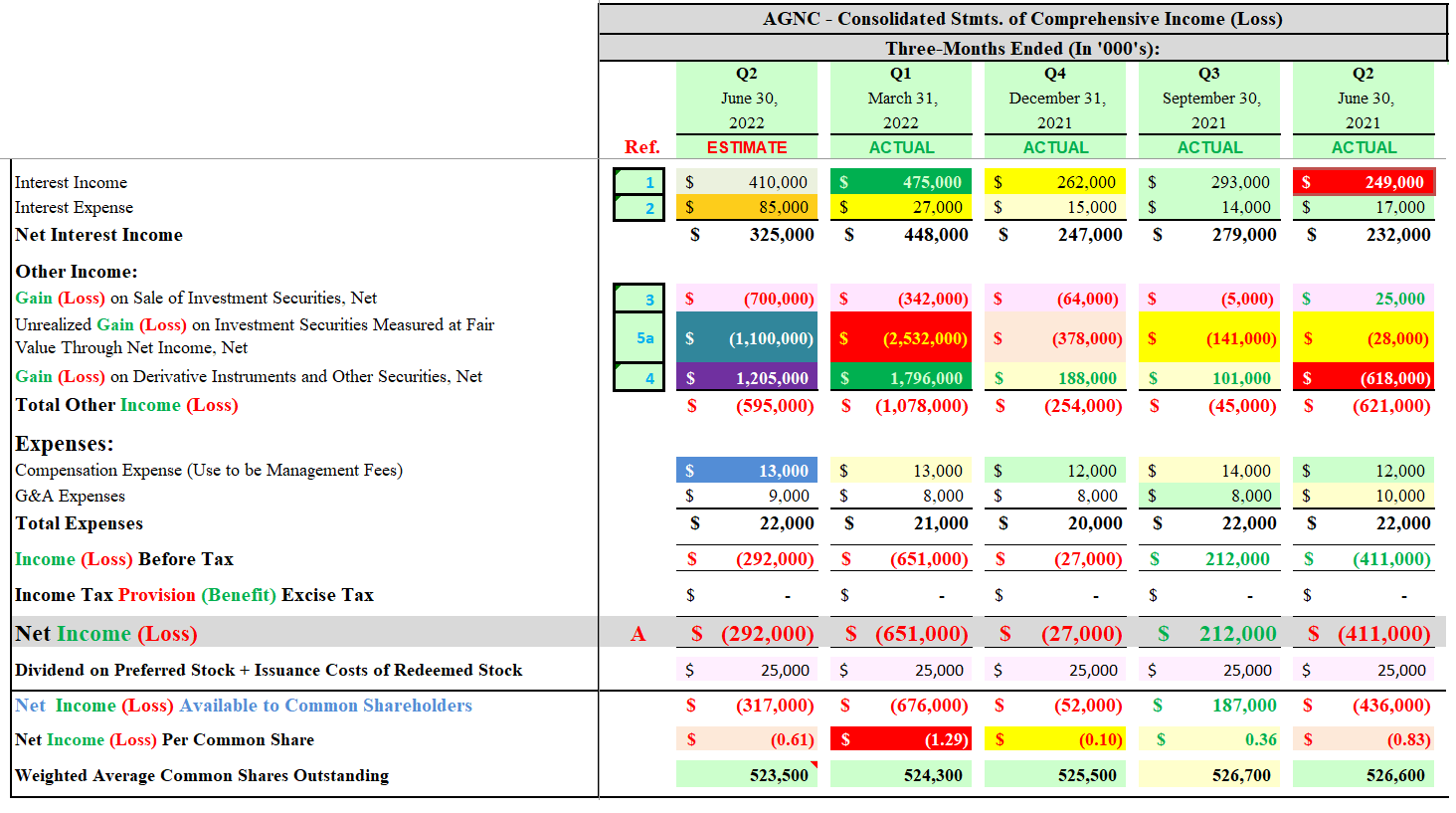

Utilizing Desk 1 beneath as a reference, allow us to first have a look at AGNC’s quarterly consolidated assertion of complete earnings (loss) for the second quarter of 2022 (ESTIMATE column). Desk 1 additionally supplies AGNC’s complete earnings (loss) for the prior 4 quarters (ACTUAL columns) for comparative functions.

Desk 1 – AGNC Quarterly Consolidated Statements of Complete Earnings (Loss)

The REIT Discussion board

(Supply: Desk created by me, partially utilizing knowledge obtained from AGNC’s quarterly investor presentation slides)

Desk 1 above is the principle supply of summarized knowledge relating to AGNC’s web earnings (loss) quantity. As such, all materials accounts inside Desk 1 will likely be individually analyzed and mentioned in corresponding order to the boxed blue reference subsequent to the June 30, 2022 column. PART 1 of this text will embrace an evaluation of the next accounts: 1) curiosity earnings; 2) curiosity expense; 3) acquire (loss) on sale of funding securities, web; and 4) acquire (loss) on spinoff devices and different securities, web (together with a number of “sub-accounts”).

1) Curiosity Earnings:

- Estimate of $410 Million; Vary $360 – $460 Million

- Confidence Inside Vary = Reasonable

- See Boxed Blue Reference “1” in Desk 1 Above and Desk 2 Beneath Subsequent to the June 30, 2022 Column

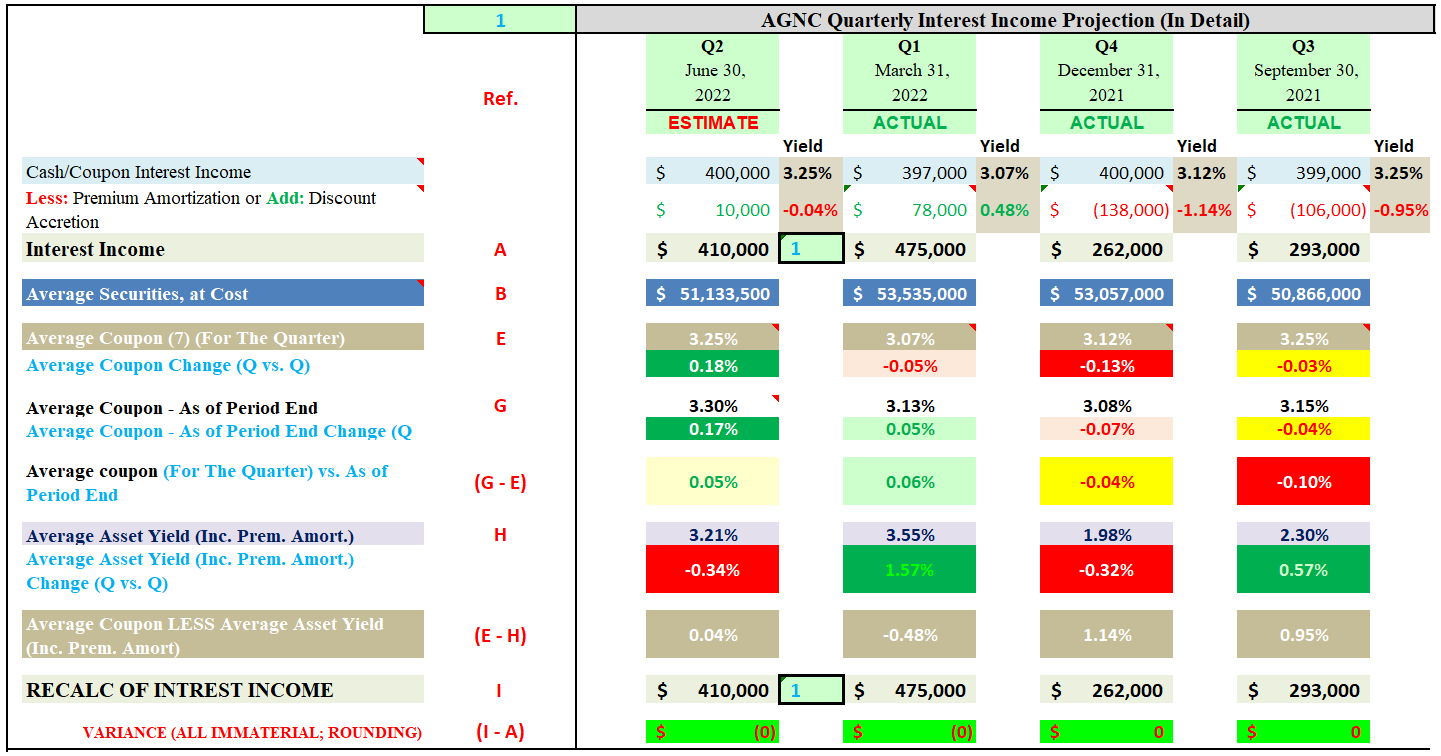

AGNC’s curiosity earnings is comprised of the next two sub-accounts: a) money curiosity earnings; and b) premium amortization, web. I present my projection for these two figures in Desk 2 beneath. There won’t be an similar sheet AGNC supplies that matches the info I’ve ready in Desk 2 beneath.

Desk 2 – AGNC Quarterly Curiosity Earnings Projection

The REIT Discussion board

(Supply: Desk created by me, partially utilizing AGNC knowledge obtained from the SEC’s EDGAR Database)

The primary element of AGNC’s curiosity earnings is the corporate’s money curiosity earnings sub-account. Two assumptions must be famous inside Desk 2 above when projecting AGNC’s money curiosity earnings for the second quarter of 2022. First, I’m projecting AGNC’s “common securities, at price” steadiness decreased by ($2.4) billion for the second quarter of 2022 when in comparison with the prior quarter ($51.1 billion versus $53.5 billion). I might take into account this a minor lower. This might proceed to be modestly beneath AGNC’s on-balance sheet MBS portfolio steadiness previous to the market’s COVID-19 “pandemic panic”. Almost all the 20 mREIT sector friends I presently cowl skilled both margin calls from debt counterparties or voluntarily diminished leverage so as to increase money/liquidity in early 2020.

Most mREIT friends have but to totally enhance every firm’s funding portfolio dimension to pre-COVID-19 ranges. Throughout the first quarter of 2020, AGNC diminished the corporate’s funding portfolio by roughly (25%) primarily based on truthful market worth (“FMV”). This was a much less extreme decline when in comparison with a median web lower of (40%) for the 7 company mREIT friends I presently cowl (excluding IVR who “switched” to a fixed-rate company mREIT put up March 2020). For AGNC, this could really be seen as a constructive catalyst/development (a much less extreme decline immediately ends in extra web unfold earnings being generated). On this occasion, AGNC’s traditionally larger money place benefited this specific fixed-rate company mREIT peer. Partially offsetting this decline, AGNC elevated the corporate’s web lengthy “to-be-announced” (“TBA”) MBS place throughout the first quarter of 2020 (which doubtless remained considerably elevated by means of nearly all of the second quarter of 2022) which is an off-balance sheet technique of investing in and financing generic company MBS.

Second, I’m projecting a minor-modest enhance to AGNC’s “weighted common coupon” (“WAC”) for the second quarter of 2022 when in comparison with the prior quarter (3.25% versus 3.07%). This projection elements in AGNC’s TBA MBS place, portfolio reinvestment, proportion of 15-year fixed-rate company MBS versus 30-year, and the online motion of mortgage rates of interest throughout the prior 2 quarters. Whereas mortgage rates of interest/U.S. Treasury yields moved notably larger throughout the first and second quarters of 2022, I imagine AGNC held on to a majority of the corporate’s present on-balance sheet MBS whereas deploying a little bit of capital/proceeds into larger coupons. Nonetheless utilizing Desk 2 above as a reference, when combining the 2 elements mentioned above, I’m projecting a money curiosity earnings enhance of $Three million for the second quarter of 2022 when in comparison with the prior quarter ($400 million versus $397 million).

The second element of AGNC’s curiosity earnings is the corporate’s premium amortization, web sub-account. Throughout a rising rate of interest surroundings, typically a lower in prepayments will happen as a result of a decrease variety of householders have mortgages which have the next rate of interest when in comparison with present market rates of interest. As such, the attractiveness of a mortgage refinance decreases. Consequently, prepayment danger typically decreases whereas extension danger will increase. Subsequently, the typical lifetime of AGNC’s fixed-rate company MBS portfolio typically lengthens. This might immediately result in a decrease quarterly premium amortization expense. The precise reverse typically happens throughout a falling rate of interest surroundings. As well as, seasonality traits must also be thought of when analyzing/projecting this account.

MBS pricing will likely be mentioned in PART 2 of this text whereas U.S. Treasury yields/pricing will likely be mentioned later in PART 1 (throughout the derivatives account). Mortgage rates of interest/long-term U.S. Treasury yields usually have an analogous, direct relationship. By way of analysis, I’ve decided a majority of AGNC’s MBS holdings skilled a comparatively unchanged-minor lower in “conditional prepayment fee” (“CPR”) percentages throughout the quarter. This contains contemplating intra-quarterly methods executed by administration (larger coupon specified pool and generic MBS).

I imagine the corporate’s “lifetime” CPR as of 6/30/2022 will barely lower from its 3/31/2022 degree. As such, I’m projecting a minor-modest adjustment to happen. Utilizing Desk 2 above as a reference, together with the idea of a barely smaller common on-balance sheet MBS portfolio steadiness (minor constructive issue), slightly-modestly decrease weighted common buy value (constructive issue), a continued a lot larger proportion of 30-year fixed-rate company MBS versus 15-year (slight constructive issue), and a minor lower in lifetime CPR share (constructive issue), I’m projecting low cost accretion, web lower of ($68) million for the second quarter of 2022 when in comparison with the prior quarter ($10 million versus $78 million).

When my projections for the money curiosity earnings and premium amortization, web expense/low cost accretion, web earnings sub-accounts are mixed, I’m projecting AGNC’s curiosity earnings to lower by ($65) million for the second quarter of 2022 when in comparison with the prior quarter ($410 million versus $475 million).

2) Curiosity Expense:

- Estimate of $85 Million; Skewed Vary $55 – $135 Million

- Confidence Inside Vary = Excessive

- See Boxed Blue Reference “2” in Desk 1 Above and Desk Three Beneath Subsequent to the June 30, 2022 Column

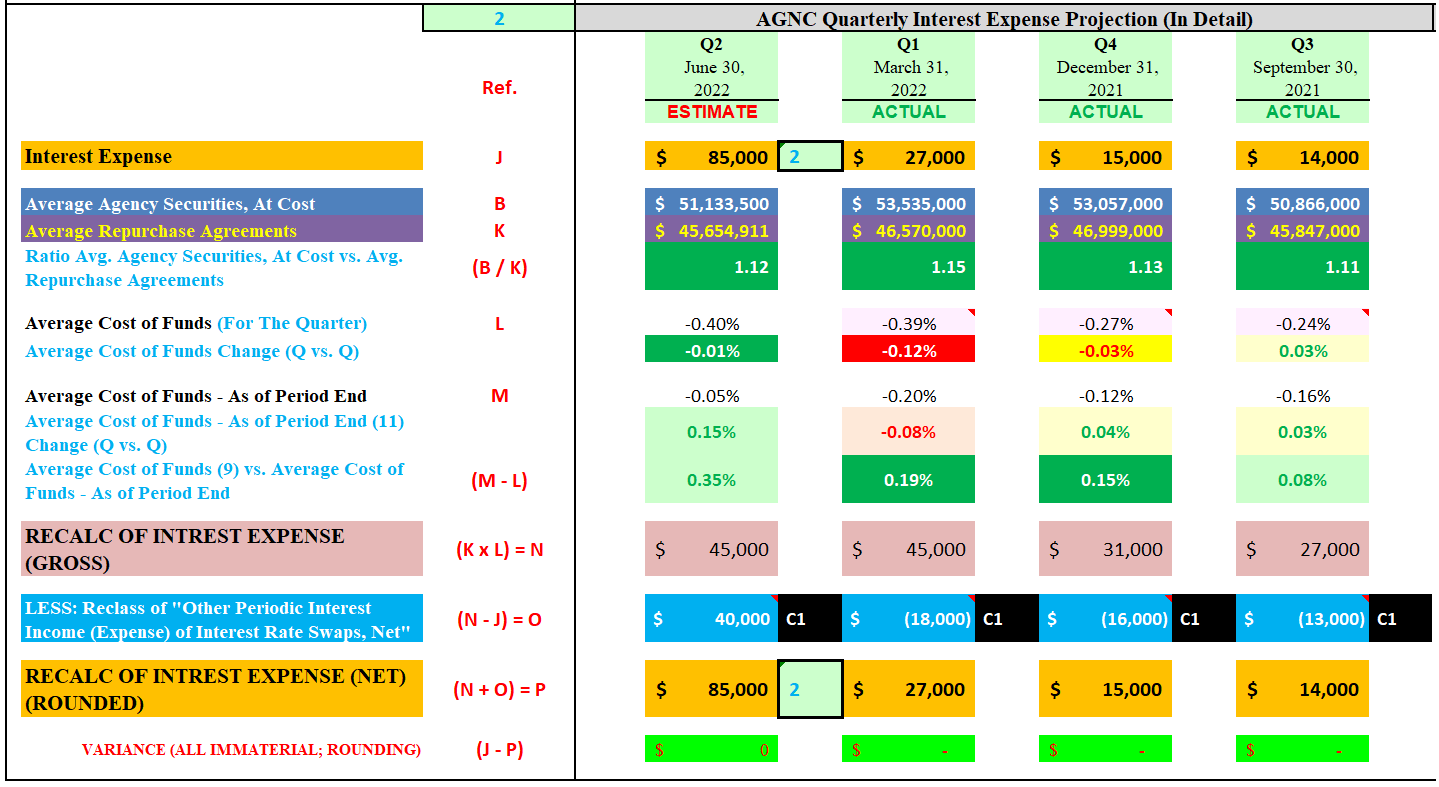

Now allow us to check out AGNC’s curiosity expense account. I present my projection for this determine in Desk Three beneath. I’ve gathered particular info derived from a number of tables/charts for a extra detailed evaluation of AGNC’s curiosity expense account.

Desk 3 – AGNC Quarterly Curiosity Expense Projection

The REIT Discussion board

(Supply: Desk created by me, partially utilizing AGNC knowledge obtained from the SEC’s EDGAR Database [link provided below Table 2])

To venture AGNC’s quarterly curiosity expense, one takes the quarterly common of the corporate’s excellent repurchase agreements (see purple reference “Ok”) and multiplies this quantity by the quarterly common price of funds fee (see purple reference “L”). As soon as this determine is calculated, one must again out a portion of the quarterly curiosity earnings (expense) in relation to AGNC’s rate of interest payer swaps. This reclassified quantity is accounted for inside AGNC’s acquire (loss) on spinoff devices and different securities, web account. This account will likely be projected later within the article. The ultimate calculated quantity is AGNC’s quarterly curiosity expense determine (see purple reference “P”). There’s additionally one other methodology that may be carried out to venture AGNC’s curiosity expense account (together with a reclassification quantity). Nevertheless, for functions of this text, I’ll solely give attention to the methodology proven in Desk Three above.

Two assumptions must be famous inside Desk Three when projecting AGNC’s quarterly curiosity expense determine for the second quarter of 2022. First, allow us to calculate an acceptable quarterly “common repurchase agreements” steadiness. Based mostly on an earlier calculated determine inside AGNC’s curiosity earnings account (see Desk 2 above), I’m projecting the corporate had a quarterly common securities at price steadiness of $51.1 billion for the second quarter of 2022. If one takes this determine and divides it by the quarterly common of AGNC’s excellent repurchase agreements steadiness, a calculated “ratio of common securities versus common repurchase agreements” is projected (purple reference “B / Ok”). This ratio has been in a spread of 1.11-1.15 throughout the prior 4 quarters. For the second quarter of 2022, I’m utilizing a ratio of 1.12 (being a bit cautious with this ratio). When calculated, this steadiness is projected to be $45.7 billion (purple shading; yellow font). It is a projected lower of ($0.9) billion for the second quarter of 2022 when in comparison with the prior quarter ($45.7 billion versus $46.6 billion).

Second, allow us to now receive an acceptable quarterly common price of funds fee. I’m projecting a rise of 1 foundation level (“bp”) relating to AGNC’s common price of funds fee for the second quarter of 2022 when in comparison with the prior quarter (0.40% versus 0.39%). Merely put, a rise in repo rates of interest much less the rise in curiosity earnings from AGNC’s rate of interest payer swaps. As talked about earlier, all curiosity earnings (expense) in relation to AGNC’s rate of interest payer swaps is reclassified out of this particular account. As such, a portion of the quarterly common price of funds fee is just not in relation to AGNC’s excellent repurchase agreements. AGNC’s curiosity expense relating to the corporate’s excellent repurchase agreements is predicated on a small fixed-rate share and a variable-rate share primarily primarily based on LIBOR. Throughout the second quarter of 2022, repurchase settlement rates of interest had a reasonably comparable fluctuation when in comparison with present/“spot” U.S. LIBOR (enhance all through the quarter).

Now that we’ve got decided AGNC’s common repurchase agreements steadiness and common price of funds fee, allow us to calculate the corporate’s curiosity expense for the second quarter of 2022. Nonetheless utilizing Desk Three above as a reference, after a projected reclassification of $40 million in relation to the online periodic curiosity earnings (expense) relating to AGNC’s rate of interest swaps, I’m projecting the corporate’s curiosity expense to extend $58 million for the second quarter of 2022 when in comparison with the prior quarter ($85 million versus $27 million).

3) Achieve (Loss) on Sale of Funding Securities, Internet:

- Estimate of ($700) Million; Vary ($900) – ($500) Million

- Confidence Inside Vary = Reasonable

- See Boxed Blue Reference “3” in Desk 1 Above Subsequent to the June 30, 2022 Column

AGNC’s acquire (loss) on sale of funding securities, web account may be considerably tough to precisely venture at occasions. By way of detailed analysis and knowledge compilation, one can venture (to an inexpensive diploma) how administration “ought to” act inside any given quarter relating to purchases and gross sales. Nevertheless, I stress beforehand this won’t be an “actual science” every quarter. There will likely be some variances that happen in 1 / 4 if extra/much less gross sales and/or purchases really happen versus initially projected. Moreover, unanticipated quarterly adjustments within the share of coupons/maturities held throughout the MBS portfolio would trigger a slight-modest deviation in asset valuations. At periodic intervals, administration supplies some readability on the corporate’s supposed technique relating to funding gross sales when mortgage rates of interest/long-term U.S. Treasury yields rise or fall. Nevertheless, a number of assumptions nonetheless must be made.

Subsequently, this specific account is immediately tied to AGNC’s “unrealized acquire (loss) on funding securities measured at FMV by means of web earnings, web” and “unrealized acquire (loss) on available-for-sale (“AFS”) securities, web” accounts that will likely be mentioned in PART 2 of this text. If AGNC’s acquire (loss) on sale of funding securities, web precise quantity is above or beneath my projected determine/vary, the variance is robotically offset in these two different accounts. As such, my mixed projected figures can be precisely represented. This consideration has been confirmed right in quite a few prior quarters over the previous 9+ years. In my skilled opinion, these three accounts ought to actually be checked out as one mixed account. The unrealized acquire (loss) on funding securities measured at FMV by means of web earnings, web and unrealized acquire (loss) on AFS securities, web accounts have an instantaneous affect on BV whereas the acquire (loss) on sale of funding securities, web account is merely a reclassification out of the unrealized accounts. Readers ought to perceive this notion previous to this account’s evaluation.

When in comparison with the prior quarter, I’m anticipating a bigger quantity of exercise inside this account throughout the second quarter of 2022. As such, I’m projecting an “funding bought, at price” quantity of ($12.5) billion for the second quarter of 2022. The extra essential determine to debate is just not the quantity of funding securities bought however whether or not a acquire (loss) occurred from the quarterly gross sales. As of 12/31/2021, AGNC had an amassed different complete acquire (“OCI”) steadiness of $301 million. This steadiness switched to an amassed different complete loss (“OCL”)to ($190) million as of three/31/2022. MBS pricing notably decreased, in all decrease coupons, throughout the second quarter of 2022 and that must be thought of.

The full quantity of AGNC’s web realized acquire (loss) can be depending on which specific funding securities have been bought and at what time throughout the quarter these gross sales occurred. When taking all elements above into consideration, I’m projecting AGNC will report a web realized loss on the sale of funding securities of ($700) million for the second quarter of 2022.

4) Achieve (Loss) on By-product Devices and Different Securities, Internet:

- Estimate of $1.21 Billion; Vary $955 Million – $1.46 Billion

- Confidence Inside Vary = Reasonable

- See Boxed Blue Reference “4” in Tables Four and 6 Beneath Subsequent to the June 30, 2022 Column

Projecting AGNC’s acquire (loss) on spinoff devices and different securities, web account is an evaluation that includes a number of sub-accounts. This contains making assumptions inside these spinoff sub-accounts throughout the present quarter. One won’t ever “totally” know administration’s derivatives actions for any given quarter till outcomes are supplied to the general public. Nevertheless, one can perceive AGNC’s general danger administration technique and make a projection on these spinoff sub-accounts utilizing the balances that have been represented on the finish of the earlier quarter. Such an in depth evaluation is smart to carry out as a result of typical occasions that unfold with regard to MBS costs, the fastened pay fee on newly created/present rate of interest swaps, and U.S. Treasury yields. When utilizing this technique, together with deciding particular quarterly assumptions, I’ve usually supplied accurate-highly correct projections inside this account over the previous 9+ years; together with over varied cycles/eventualities.

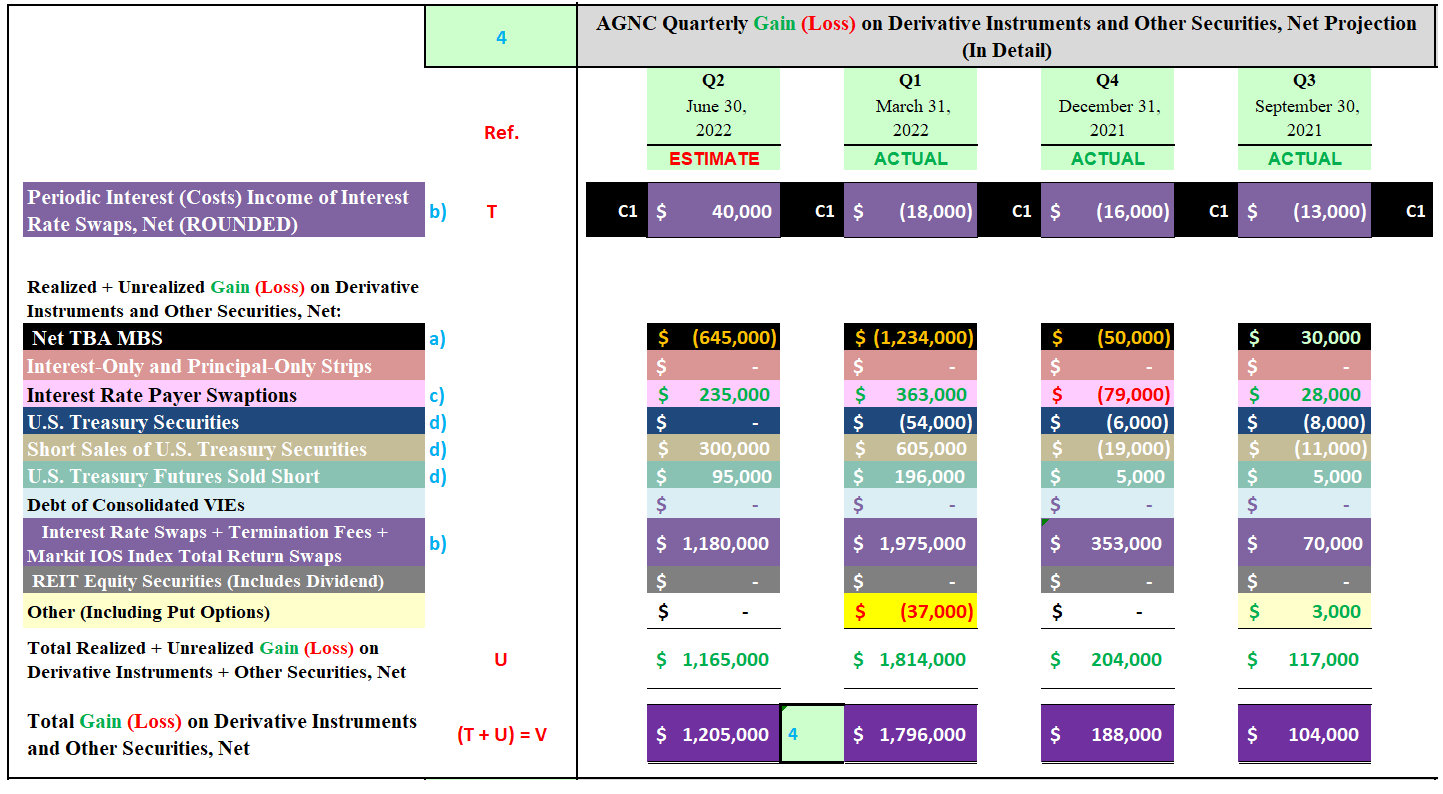

Now allow us to check out AGNC’s acquire (loss) on spinoff devices and different securities, web account. I present my projection for this determine in Desk Four beneath. All projected (ESTIMATE) sub-account figures are calculated and derived from a number of tables/charts that won’t be proven inside this specific article.

Desk 4 – AGNC Quarterly Achieve (Loss) on By-product Devices and Different Securities, Internet Projection (All Sub-Accounts)

The REIT Discussion board

(Supply: Desk created by me, partially utilizing AGNC knowledge obtained from the SEC’s EDGAR Database [link provided below Table 2])

Inside AGNC’s acquire (loss) on spinoff devices and different securities, web account is the next 4 materials sub-accounts that will likely be mentioned beneath: a) TBA MBS; b) rate of interest swaps; c) rate of interest swaptions; and d) U.S. Treasury securities. Every of the 4 materials spinoff sub-accounts will likely be individually analyzed and mentioned in corresponding order of the blue references below the “Ref.” column in Desk Four above.

a) TBA MBS (Internet Lengthy Place as of three/31/2022):

- Estimate of ($645) Million; Vary ($845) – ($445) Million

- Confidence Inside Vary = Reasonable

- See Black Highlighted, Blue Referenced Sub-Account “a)” in Desk Four Above Subsequent to the June 30, 2022 Column

Allow us to first briefly get accustomed with such a spinoff instrument. Sometimes, AGNC makes use of a mixture of each lengthy and (brief) TBA MBS contracts throughout any given quarter. AGNC enters into TBA contracts with an extended place the place it agrees to purchase, for future supply, MBS with sure predetermined costs, face quantities, issuers, coupons, and acknowledged maturities. AGNC enters into TBA contracts with an extended place as an off-balance sheet technique of investing in and financing MBS. Since TBA contracts with an extended place are in the end an extension of the steadiness sheet, this will increase AGNC’s “in danger” leverage. AGNC enters into TBA contracts with a (brief) place the place it agrees to promote, for future supply, MBS with sure predetermined costs, face quantities, issuers, coupons, and acknowledged maturities. Since TBA contracts with a (brief) place are in the end a discount of the steadiness sheet, this decreases AGNC’s in danger leverage.

There are two most important elements that affect this spinoff sub-account’s valuation in any given quarter. The primary issue is the online greenback roll (“NDR”) earnings (expense) generated on AGNC’s web lengthy (brief) TBA MBS place. The second issue is the realized valuation acquire (loss) upon the settlement of all TBA MBS contracts and the unrealized valuation acquire (loss) on all contracts which have but to be settled on the finish of the quarter.

AGNC had a web lengthy TBA MBS place of $19.6 billion as of three/31/2022 (primarily based on notional quantity). AGNC decreased the corporate’s web lengthy TBA MBS place by ($7.1) billion throughout the first quarter of 2022. Not like most of 2017-2018, greenback roll financing throughout most coupons remained much less engaging throughout 2019-early 2020. I imagine this was one of many most important the explanation why AGNC, AAIC, ARR, and NLY diminished their dividend per share charges throughout this timeframe (all mREIT friends who modestly-heavily make the most of the ahead TBA market; pre-COVID-19 traits). Nevertheless, popping out of the preliminary COVID-19 pandemic panic, greenback roll financing grew to become engaging as soon as once more; particularly in decrease coupons. Implied financing charges even turned unfavourable throughout 2020-2021 inside some coupons (which was a constructive catalyst/development).

Persevering with a development skilled throughout most of 2019, larger coupon “specified pool” MBS skilled a larger “choice” versus larger coupon generic TBA MBS as a result of general macroeconomic traits throughout the broader mortgage universe (rise in prepayment danger). As such, administration diminished publicity to larger coupon generic TBA MBS whereas rising publicity to decrease coupon generic TBA MBS throughout the second, third, and fourth quarters of 2020. This common development has continued throughout the first-fourth quarters of 2021. Nevertheless, with the short rise in mortgage rates of interest/longer-term U.S. Treasury yields, this sample started to shift throughout the first quarter of 2022 which I imagine continued throughout the second quarter of 2022.

Nevertheless, having a proportionately giant web lengthy TBA MBS place heading into 2022 led to disastrous outcomes from a valuation perspective. Merely put, decrease coupon generic MBS pricing rapidly, and notably, decreased throughout the first quarter of 2022. AGNC took a minor constructive step with reversing to a web (brief) place throughout the 30-year fixed-rate company MBS with a 2.00% coupon as of three/31/2022. Nevertheless, this web (brief) place was very minor in comparison with the rest of AGNC’s web lengthy place within the 2.50% – 4.00% coupons. Even with continued engaging greenback roll financing, the era of this specific earnings was vastly “trumped” by extraordinarily extreme quarterly MBS valuation losses throughout the second quarter of 2022. Particular fixed-rate company MBS value adjustments will likely be proven in PART 2 of this projection article.

Since 30-year fixed-rate company TBA MBS throughout all coupons skilled various severities of value decreases, though greenback roll financing remained pretty attractive-attractive, I imagine AGNC needed to, in any case, merely keep the corporate’s web lengthy place by the tip of the second quarter of 2022. If something, a smaller web lengthy TBA MBS place would have made sense from a valuation standpoint.

By way of an in depth evaluation that will likely be omitted from this specific article, when combining the corporate’s projected quarterly NDR earnings and web valuation loss, I’m projecting AGNC’s TBA MBS place had a complete web valuation lack of ($645) million for the second quarter of 2022.

b) Curiosity Fee Swaps (Internet (Quick) Place as of three/31/2022):

- Estimate of $1.22 Billion; Vary $1.02 – $1.42 Billion

- Confidence Inside Vary = Reasonable

- See Purple Highlighted, Blue Referenced Secondary Sub-Accounts “b)” in Desk Four Above Subsequent to the June 30, 2022 Column

Allow us to first focus on the current historical past of this spinoff sub-account which can result in a greater understanding of my projected whole web valuation acquire for the second quarter of 2022. AGNC had a web (brief) rate of interest swaps place of ($51.1) billion as of three/31/2022 (primarily based on notional quantity). AGNC decreased the corporate’s web (brief) rate of interest payer swaps place by $0.1 billion throughout the first quarter of 2022.

As identified earlier, AGNC barely lowered the corporate’s mixed on- and off-balance sheet MBS portfolio throughout the first quarter of 2022. AGNC barely decreased the corporate’ on-balance sheet MBS portfolio and whereas slightly-modestly reducing its off-balance sheet web lengthy TBA MBS place. As such, when all different elements are held fixed, a comparatively comparable hedge place is relevant when merely “sustaining” one’s danger administration technique. AGNC needed to turn into a bit extra “defensive” relating to the corporate’s danger administration technique.

Strictly from a valuation perspective, it was not essentially the most advantageous choice to mainly keep one’s hedging protection ratio throughout the first and second quarters of 2022. An excellent bigger web (brief) place would have led to a extra enhanced web valuation acquire. Merely put, together with the notable rise in unfold/foundation danger over the previous 12 months (outlined close to the start of this text), this negatively impacted practically all sub-sector BVs.

Utilizing Desk Four above as a reference, there are two secondary sub-accounts to debate when projecting a complete web valuation acquire (loss) relating to AGNC’s rate of interest swaps. The primary secondary sub-account is AGNC’s “web periodic curiosity earnings (prices/expense) of rate of interest swaps”. If one recollects, this determine was first mentioned in AGNC’s curiosity expense account. With regard to AGNC’s rate of interest swaps web (brief) place as of three/31/2022, the corporate had a weighted common fastened pay fee of 0.20% and a weighted common floating obtain fee of 0.26%. This weighted common fastened pay fee is notably extra engaging versus most sector friends who make the most of this particular spinoff instrument. As well as, AGNC’s weighted common floating obtain fee has not too long ago rapidly elevated (and can proceed to rapidly enhance over the foreseeable future).

When all elements and assumptions are considered, by means of an in depth evaluation that will likely be omitted from this specific article, I’m projecting AGNC will report a web periodic curiosity earnings (expense) of $40 million for the second quarter of 2022 versus ($18) million throughout the prior quarter. I’m anticipating AGNC didn’t add any new rate of interest payer swaps throughout the quarter whereas a really small proportion matured (this contains assuming no swaptions have been exercised). LIBOR rapidly moved larger all through the quarter and the Normal In a single day Financing Fee (“SOFR”) rapidly moved larger in direction of the tip of the quarter.

The second secondary sub-account to debate pertains to the online valuation acquire (loss) on AGNC’s rate of interest swaps. Throughout most tenors/maturities, there was a notable/large enhance within the fastened pay fee of rate of interest payer swap contracts throughout the second quarter of 2022. The fastened pay fee on rate of interest swap contracts throughout all tenors/maturities had a web fluctuation of 55 – 140 bps throughout the second quarter of 2022. As such, there may be going to be some larger-than-average valuation fluctuations amongst mREIT friends relating to this particular spinoff instrument for the second quarter of 2022.

By way of an in depth evaluation that will likely be omitted from this specific article, I’m projecting the corporate’s second secondary sub-account had a web valuation acquire of $1.18 billion for the second quarter of 2022. The contains the idea AGNC’s administration staff continued to mainly keep the weighted common tenor of the portfolio, mainly keep the notional worth of the online (brief) place, and solely barely elevated the weighted common fastened pay fee of this particular portfolio. When each secondary sub-accounts are mixed, I’m projecting AGNC’s rate of interest swaps had a complete web valuation acquire of $1.22billion for the second quarter of 2022.

c) Curiosity Fee Swaptions (Internet (Quick) Place as of three/31/2022):

- Estimate of $235 Million; Vary $85 – $385 Million

- Confidence Inside Vary = Reasonable to Excessive

- See Pink Highlighted, Blue Referenced Sub-Account “c)” in Desk Four Above Subsequent to the June 30, 2022 Column

Allow us to first briefly get accustomed with such a spinoff instrument. Rate of interest swaptions are choices to enter into underlying rate of interest swap contracts. Whereas rate of interest swap contracts haven’t any preliminary “up-front” prices (beneficial properties and losses are incurred as rates of interest fluctuate over the lifetime of the swaps), rate of interest swaptions have implicit up-front prices (just like an possibility contract; typically talking). Nevertheless, a realized acquire (loss) is just incurred (and is deferred over the remaining lifetime of the underlying swap) when the choice expires/terminates/is bought.

Allow us to focus on the current historical past of this spinoff sub-account which can result in a greater understanding of my projected whole web valuation acquire for the second quarter of 2022. AGNC had a web (brief) rate of interest swaptions place of ($10.3) billion as of three/31/2022 (primarily based on the notional steadiness of the underlying rate of interest swaps). AGNC decreased the corporate’s web (brief) rate of interest payer swaptions place by $2.Eight billion throughout the first quarter of 2022. As of three/31/2022, AGNC’s rate of interest payer swaptions had a weighted common of 18 months till expiration with an underlying rate of interest swaps weighted common tenor/maturity of 9.2 years and a weighted common fastened pay fee of two.16%.

Primarily since rate of interest payer swaps with an analogous weighted common tenor/maturity had a set pay fee of two.80%-3.10% as of three/31/2022 (a number of differing kinds), I’m projecting AGNC’s rate of interest payer swaptions had a complete web valuation acquire of $235 million for the second quarter of 2022. I imagine most of AGNC’s swaptions will finally be exercised (which derives “worth”; particularly contracts additional out on the choice time horizon). Would make sense if AGNC was trying to enhance the corporate’s company MBS portfolio sooner or later.

d) U.S. Treasury Securities (Internet (Quick) Place as of three/31/2022):

- Estimate of $395 Million; Vary $145 – $545 Million

- Confidence Inside Vary = Reasonable

- See Darkish Blue, Brown, and Teal Highlighted, Blue Referenced Secondary Sub-Accounts “d)” in Desk Four Above Subsequent to the June 30, 2022 Column

Allow us to first briefly get accustomed with such a spinoff instrument. AGNC purchases (or sells brief) U.S. Treasury securities and U.S. Treasury safety futures to assist mitigate the potential affect of adjustments in MBS costs (therefore the valuation of a majority of the corporate’s funding portfolio). AGNC borrows securities to cowl U.S. Treasury (brief gross sales) below reverse repurchase agreements. AGNC accounts for these spinoff devices as “safety borrowing transactions” and acknowledges an obligation to return the borrowed securities at FMV primarily based on the present worth of the underlying borrowed securities.

Allow us to focus on the current historical past of this spinoff sub-account which can result in a greater understanding of my projected whole web valuation acquire for the second quarter of 2022. AGNC had the next three spinoff secondary sub-account positions as of three/31/2022: 1) lengthy U.S. Treasury securities of $0.7 billion; 2) (brief) U.S. Treasury securities of ($10.9) billion; and 3) U.S. Treasury safety futures bought (brief) of ($5.4) billion. That is primarily based on every secondary sub-account’s face quantity (“par”). When combining all three secondary sub-accounts collectively, AGNC elevated the corporate’s web (brief) U.S. Treasury securities place by ($4.9) billion throughout the first quarter of 2022.

Yields on 5-, 7-, and 10-year U.S. Treasury securities elevated 55-70 bps throughout the second quarter of 2022. U.S. Treasury and U.S. Treasury futures pricing skilled an analogous fluctuations. Since U.S. Treasury securities are one of the liquid investments within the market, AGNC trades these spinoff devices all through the quarter which must be considered.

By way of an in depth evaluation that will likely be omitted from this specific article, I’m projecting AGNC’s U.S. Treasury securities and U.S. Treasury safety futures had a complete web valuation acquire of $395 million for the second quarter of 2022. If AGNC slightly-modestly elevated the corporate’s web (brief) U.S. Treasury securities place, then its web valuation acquire can be extra enhanced (and vice versa).

All remaining spinoff sub-accounts inside Desk Four that haven’t been particularly talked about above are deemed immaterial for dialogue functions. This contains valuation projections relating to the next spinoff sub-accounts: 1) interest-only (“IO”) and principle-only (“PO”) strips; 2) debt on consolidated variable-interest-entities (“VIE”); 3) REIT fairness securities (no place as of three/31/2022); and 4) put choices (when relevant).

When combining all of the spinoff sub-accounts collectively (each materials and immaterial), I’m projecting AGNC’s spinoff devices and different securities, web account had a complete web valuation acquire of $1.21 billion for the second quarter of 2022. Now, I wish to focus on my quarterly projection for AGNC’s web unfold + NDR earnings for the and examine it to a number of prior quarters.

Dialogue of AGNC’s Internet Unfold + NDR Earnings:

The REIT Discussion board Function

A) Internet Earnings (Loss):

- Estimate of ($292) Million; Vary ($492) – ($92) Million

- Internet Earnings (Loss) Obtainable to Widespread Shareholders of ($0.61) Per Share (Excluding OCI/(OCL)); Vary ($0.99) – ($0.22) Per Share

- Confidence Inside Vary = Reasonable

- See Crimson Reference “A” in Desk 6 Beneath Subsequent to the June 30, 2022 Column

Three remaining accounts inside AGNC’s consolidated assertion of complete earnings (loss) that affect the corporate’s web earnings (loss) quantity are the next: 1) unrealized acquire (loss) on investments measured at FMV by means of web earnings (loss), web; 2) compensation expense; and 3) common/administrative bills. Regarding the first listed account, this projection will likely be mentioned in PART 2 of the article; though it’s a part of AGNC’s web acquire (loss) quantity and proven inside Desk 1. Whereas the remaining two accounts have been projected inside Desk 1, they’re deemed immaterial for dialogue functions and will likely be excluded from any evaluation inside this text.

When the accounts from Desk 1 above are mixed, I’m projecting AGNC had a web lack of ($292) million for the second quarter of 2022. After accounting for AGNC’s quarterly most popular inventory dividends, this may be earnings (loss) out there to widespread shareholders of ($0.61) per share.

Conclusions Drawn (PART 1):

To sum up the evaluation above, I’m projecting AGNC will report the next account figures for the second quarter of 2022 (refer again to Desk 1 close to the start of the article):

1) Quarterly Curiosity Earnings of $410 Million

2) Quarterly Curiosity Expense of $85 Million

3) Quarterly Internet Loss on the Sale of Funding Securities of ($700) Million

4) Quarterly Internet Achieve on By-product Devices and Different Securities of $1.21 Billion

I’m additionally projecting AGNC will report the next web loss, EPS, and web unfold + NDR earnings quantities for the second quarter of 2022 (refer again to Tables 1 and 5):

A) Quarterly Internet Lack of ($292) Million; Earnings (Loss) Obtainable to Widespread Shareholders of ($0.61) Per Share

– Quarterly Internet Unfold + NDR Earnings (1 Dividend Sustainability Metric) of $0.690 Per Widespread Share

AGNC’s projected web lack of ($292) million for the second quarter of 2022 is a modest enhance when in comparison with a web lack of ($651) million for the primary quarter of 2022. That is primarily as a result of a projected much less extreme web realized and unrealized loss on funding securities when in comparison with the prior quarter, partially offset by a notably much less enhanced derivatives web valuation acquire.

As acknowledged earlier, AGNC’s OCI/(OCL) quantity is a part of the corporate’s consolidated assertion of complete earnings (loss) however is excluded from the corporate’s web earnings (loss) and EPS quantities.

As such, I STRONGLY recommend holding off on a “ultimate verdict” relating to AGNC’s projected outcomes for the second quarter of 2022 till PART 2 of this text is supplied.

In my skilled opinion, I imagine AGNC’s “complete acquire (loss)” quantity is extra essential than the corporate’s web earnings (loss) and EPS quantities.

My BUY, SELL, or HOLD Advice:

I made a decision to supply my AGNC suggestion to readers after PART 1 of this text so there’s a higher sense on my ideas relating to the corporate’s present valuation (so readers wouldn’t have to attend till PART 2). I might stress beforehand this suggestion is predicated on all of my AGNC account projections, together with accounts that will likely be mentioned in PART 2.

From the evaluation supplied above, together with extra catalysts/elements not mentioned inside this specific article, I presently fee AGNC as a SELL once I imagine the corporate’s inventory value is buying and selling at or larger than my projected non-tangible CURRENT BV (BV as of seven/15/2022), a HOLD when buying and selling at lower than my projected non-tangible CURRENT BV by means of lower than a (10%) low cost to my projected non-tangible CURRENT BV, and a BUY when buying and selling at or larger than a (10%) low cost to my projected non-tangible CURRENT BV. These ranges are unchanged when in comparison with my final AGNC article (roughly 2.5 months in the past).

AGNC’s inventory value closed at $12.00 on 7/19/2022.

Subsequently, I presently fee AGNC as a HOLD.

As such, I presently imagine AGNC is appropriately valued from a inventory value perspective. My present value goal for AGNC is roughly $12.65 per share. That is presently the worth the place my suggestion would change to a SELL. The present value the place my suggestion would change to a BUY is roughly $11.40 per share. Put one other means, the next are my CURRENT BUY, SELL, or HOLD per share suggestion ranges (the REIT Discussion board subscribers get such a knowledge on all 20 mREIT shares I presently cowl on a weekly foundation):

$12.65 per share or above = SELL

$11.41 – $12.64 per share = HOLD

$10.11 – $11.40 per share = BUY

$10.10 per share or beneath = STRONG BUY

Together with the info offered inside this text, this suggestion considers the next mREIT catalysts/elements: 1) projected future MBS/funding value actions; 2) projected future spinoff valuations; and 3) projected near-term (as much as 1-year) dividend per share charges. These suggestions additionally take into account the Eight Federal (“Fed”) Funds Fee will increase by the FOMC throughout December 2016-2018 (a extra hawkish tone/rhetoric when in comparison with 2014-2016), the three Fed Funds Fee decreases throughout 2019 as a result of extra dovish tone/rhetoric relating to general financial coverage because of current macroeconomic traits/occasions, and the very fast “plunge” within the Fed Funds Fee to close 0% in March 2020. This additionally considers the earlier wind-down/lower of the Fed Reserve’s steadiness sheet by means of gradual runoff/partial non-reinvestment (which started in October 2017 which elevated unfold/foundation danger) and the prior “easing” of this wind-down that began in Might 2019 relating to U.S. Treasuries and August 2019 relating to company MBS (which partially diminished unfold/foundation danger when volatility remained subdued). This additionally considers the early Spring 2020 announcement of the beginning of one other spherical of quantitative easing (“QE”) that features the Fed particularly buying company MBS (and “rolling over” all principal and curiosity funds into new company MBS) which bolstered costs whereas holding long-term/mortgage rates of interest close to historic lows (which lowered unfold/foundation danger for fairly a while when volatility remained subdued). This additionally contains the current “taper” of the Fed’s most up-to-date QE program relating to its month-to-month purchases of $80 billion of U.S. Treasury securities and $40 billion of company MBS. This taper started in November 2021 and market hypothesis round this future occasion has already induced an increase in unfold/foundation danger throughout the summer season of 2021 and throughout the second half of the fourth quarter of 2021-June 2022 (as accurately beforehand anticipated). This contains the FOMC’s current accelerated taper timeline (which completed in March 2022 versus the prior anticipated timeline of June 2022) and the continued very doubtless fast rise within the Fed Funds Fee to 2.50%-3.25% by the tip of 2022 which started again in March 2022. I imagine unfold/foundation danger ought to start to abate by the tip of summer season 2022.

Present Sector/Latest NLY/AGNC Inventory Disclosures:

On 3/18/2020, I initiated a place in NLY at a weighted common buy value of $5.05 per share (giant buy). This weighted common per share value excluded all dividends acquired/reinvested. On 6/9/2021, I bought my complete NLY place at a weighted common gross sales value of $9.574 per share as my value goal, on the time, of $9.55 per share was surpassed. This calculates to a weighted common realized acquire and whole return of 89.6% and 112.0%, respectively. I held this place for roughly 15 months.

On 3/18/2020, I as soon as once more initiated a place in AGNC at a weighted common buy value of $7.115 per share (giant buy). This weighted common per share value excludes all dividends acquired/reinvested. On 6/2/2021, I bought my complete AGNC place at a weighted common gross sales value of $18.692 per share as my value goal, on the time, of $18.65 per share was surpassed. This calculates to a weighted common realized acquire and whole return of 162.7% and 188.6%, respectively. I held this place for roughly 14.5 months.

On 1/31/2017, I initiated a place in New Residential Funding Corp. (NRZ) at a weighted common buy value of $15.10 per share. On 6/29/2017, 7/7/2017, and 12/21/2018, I elevated my place in NRZ at a weighted common buy value of $15.775, $15.18, and $14.475 per share, respectively. When mixed, my NRZ place had a weighted common buy value of $14.912 per share. This weighted common per share value excluded all dividends acquired/reinvested. On 2/6/2020, I bought my complete NRZ place at a weighted common gross sales value of $17.555 per share as my value goal, on the time, of $17.50 per share was surpassed. This calculates to a weighted common realized acquire and whole return of 17.7% and 41.2%, respectively. I held this place, on a weighted common foundation, for roughly 20 months.

On 9/22/2020, I as soon as once more initiated a place in NRZ at a weighted common buy value of $7.645 per share. On 1/28/2021, 7/16/2021, 8/20/2021, 4/7/2022, 6/13/2022, 6/14/2022, and 6/17/2022, I elevated my place in NRZ at a weighted common buy value of $9.415, $9.525, $9.485, $10.11, $9.345, $9.055, and $8.421 per share, respectively. When mixed, my NRZ place has a weighted common buy value of $8.977 per share. This weighted common per share value excludes all dividends acquired/reinvested.

On 1/2/2020, I initiated a place in Arlington Asset Funding Corp. (AAIC) at a weighted common buy value of $5.57 per share. On 1/9/2020, 3/16/2020, 9/24/2020, 5/6/2021, 9/2/2021, 9/10/2021, 11/10/2021, 11/24/2021, and three/3/2022, I elevated my place in AI at a weighted common buy value of $5.59, $3.25, $2.53, $3.875, $3.748, $3.75, $3.752, $3.70, and $3.395 per share, respectively. When mixed, my AAIC place has a weighted common buy value of $3.456 per share. This weighted common per share value excludes all dividends acquired/reinvested.

On 10/19/2020, I initiated a place in PennyMac Mortgage Funding Belief (PMT) at a weighted common buy value of $16.275 per share. On 10/29/2020, 8/12/2021, 8/20/2021, 11/18/2021, 2/4/2022, and 4/19/2022, I elevated my place in PMT at a weighted common buy value of $14.90, $18.693, $18.407, $18.180, $16.024, and $14.721 per widespread share, respectively. When mixed, my PMT place has a weighted common buy value of $15.857 per share. This weighted common per share value excludes all dividends acquired/reinvested.

On 12/1/2020, I initiated a place in DX at a weighted common buy value of $16.59 per share. On 12/20/2021, I elevated my place in DX at a weighted common buy value of $15.35 per share. When mixed, my DX place has a weighted common buy value of $15.66 per share. This weighted common per share value excludes all dividends acquired/reinvested.

On 10/12/2018, I initiated a place in Granite Level Mortgage Belief, Inc. (GPMT)at a weighted common buy value of $18.155 per share. On 5/12/2020, 5/27/2020, 5/28/2020, 8/26/2020, 9/10/2020, and 9/11/2020, I elevated my place in GPMT at a weighted common buy value of $4.745, $5.144, $5.086, $6.70, $6.19, and $6.045 per share, respectively. My final two purchases made up roughly 50% of my whole place (to place issues in higher perspective). When mixed, my GPMT place had a weighted common buy value of $6.234 per share. This weighted common per share value excluded all dividends acquired/reinvested. On 6/8/2021, I bought my complete GPMT place at a weighted common gross sales value of $15.783 per share as my value goal, on the time, of $15.75 per share was surpassed. This calculates to a weighted common realized acquire and whole return of 153.2% and 168.7%, respectively. I held this place, on a weighted common foundation, for roughly 11 months.

On 12/10/2021, I as soon as once more initiated a place in GPMT at a weighted common buy value of $11.817 per share. On 12/15/2021, 4/19/2022, and 4/29/2022, I elevated my place in GPMT at a weighted common buy value of $11.318, $9.998, and $9.69 per share, respectively. When mixed, my GPMT place has a weighted common buy value of $10.613 per share. This weighted common per share value excludes all dividends acquired/reinvested.

On 1/24/2022, I initiated a place in Prepared Capital Corp. (RC) at a weighted common buy value of $13.39 per share. On 6/29/2022, I elevated my place in RC at a weighted common buy value of $11.69 per share. When mixed, my RC place has a weighted common buy value of $12.257 per share. This weighted common per share value excludes all dividends acquired/reinvested.

Remaining Notice: All trades/investments I’ve carried out over the previous a number of years have been disclosed to readers in “actual time” (that day on the newest) through both the StockTalks function of Searching for Alpha or, extra not too long ago, the “reside chat” function of the Market Service the REIT Discussion board (which can’t be modified/altered). By way of these assets, readers can lookup all my prior disclosures (buys/sells) relating to all firms I cowl right here at Searching for Alpha (see my profile web page for a listing of all shares lined). By way of StockTalk disclosures and/or the reside chat function of the REIT Discussion board, on the finish of June 2022 I had an unrealized/realized acquire “success fee” of 83.9% and a complete return (contains dividends acquired) success fee of 90.3% out of 62 whole previous and current mREIT and enterprise improvement firm (“BDC”) positions (up to date month-to-month; a number of purchases/gross sales in a single inventory depend as one general place till totally closed out). I encourage different Searching for Alpha contributors to supply actual time purchase and promote updates for his or her readers/subscribers which might in the end result in larger transparency/credibility. Beginning in January 2020, I’ve transitioned all my real-time buy and sale disclosures solely to members of the REIT Discussion board. All relevant public articles will nonetheless have my buy and sale disclosures (simply not in actual time). Please disregard any minor “beauty” typos if/when relevant.

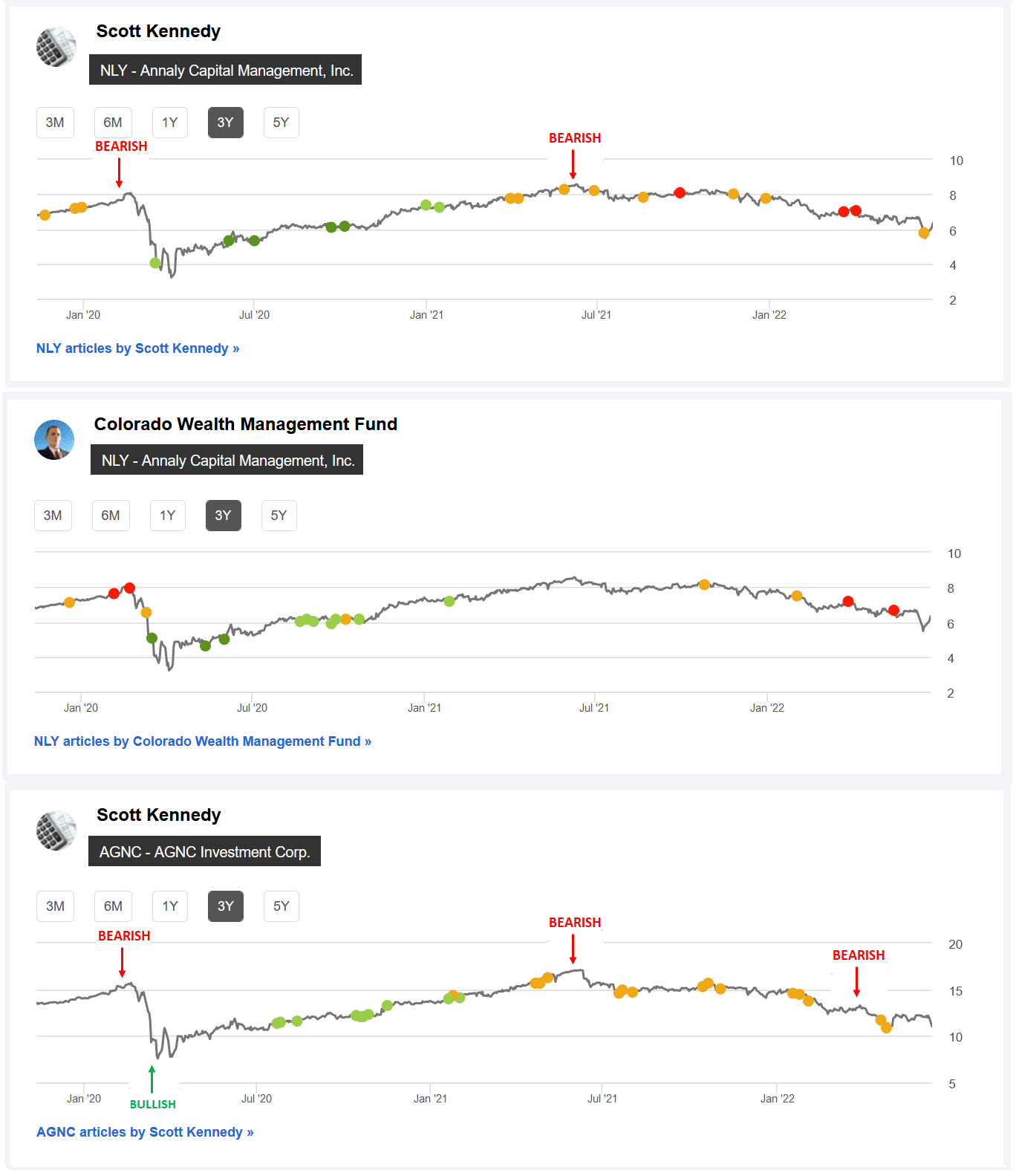

Desk 6 – The REIT Discussion board NLY + AGNC Searching for Alpha Suggestions (November 2019 – June 2022 Timeframe)

The REIT Discussion board

(Supply: Desk immediately from Searching for Alpha; 1st AGNC “Bearish” indicator included by me immediately from the public AGNC article dated 2/5/2020 suggestion [which can’t be changed once public], AGNC “Bullish” indicator included by me immediately from the public AGNC article dated 4/17/2020 suggestion [which can’t be changed once public], 2nd AGNC and 1st NLY “Bearish” indicator included by me immediately from the REIT Discussion board’s weekly subscriber suggestion article collection [week of 6/4/2021 for AGNC and week of 6/11/2021 for NLY], and threerd AGNC “Bearish” indicator included by me immediately from the REIT Discussion board’s weekly subscriber suggestion article collection [week of 4/8/2022])

Lastly, I simply wish to rapidly spotlight my/our AGNC and NLY Searching for Alpha suggestion ranges over the previous a number of years. In my private opinion, a inventory with a BUY suggestion ought to enhance in value over time, a SELL suggestion ought to lower in value over time, and a HOLD suggestion ought to stay comparatively unchanged in value over time (fairly logical). Merely put, my/our “valuation methodology” has accurately timed when each AGNC and NLY have been undervalued (a BUY suggestion; bullish), overvalued (a SELL suggestion; bearish), and appropriately valued (a HOLD suggestion; impartial).

Utilizing Desk 6 above as a reference, I imagine we’ve got achieved a reasonably good job in my/our AGNC and NLY suggestion rankings. For NLY, each pricing charts ought to actually be seen as 1 mixed chart since CO and I are a part of the identical Market service staff. Not solely do I/we wish to present steerage/a suggestion that enhances whole returns for subscribers, I/we additionally wish to shield these generated returns by subsequently minimizing whole losses. I personally imagine this technique/technique is essential. In different phrases, accurately recognizing each constructive catalysts/traits and unfavourable elements/traits as financial and rate of interest cycles fluctuate.

This technique/technique was extraordinarily helpful/correct when going again to very late 2019 and early 2020 (each pre-COVID-19) the place I/we had a SELL suggestion on each AGNC and NLY. For some purpose, this S.A. pricing chart doesn’t present my AGNC SELL suggestion pre-COVID-19 however one can merely look again to previous public articles in early 2020 (simply an omission on S.A.’s finish on this specific case). Instead, merely have a look at the NLY SELL suggestion highlighted in CO’s pricing chart (AGNC and NLY usually have very comparable suggestion ranges when contemplating comparable time durations). Moreover, after the preliminary “pandemic panic”, I/we had a STRONG BUY suggestion on each AGNC and NLY later within the spring of 2020.

Merely put, a contributor’s/staff’s suggestion monitor report ought to “depend for one thing” and may at all times be thought of on the subject of credibility/profitable investing. You’ll not see most (if not all) different contributor groups use such a factual, recommendation-driven value chart as a result of the outcomes are usually not practically as “engaging” when in comparison with our personal.

Every investor’s BUY, SELL, or HOLD choice is predicated on one’s danger tolerance, time horizon, and dividend earnings objectives. My private suggestion won’t match every reader’s present investing technique. The factual info supplied inside this text is meant to assist help readers on the subject of investing methods/selections.

Understanding My/Our Valuation Methodology Relating to mREIT Widespread and BDC Shares:

The fundamental “premise” round my/our suggestions within the mREIT widespread and BDC sectors is worth. Relating to operational efficiency over the long-term, there are above common, common, and beneath common mREIT and BDC shares. That stated, better-performing mREIT and BDC friends may be costly to personal, in addition to being low-cost. Simply because a well-performing inventory outperforms the corporate’s sector friends over the long-term, this doesn’t imply this inventory must be owned at any value. As with every inventory, there’s a value vary the place the valuation is affordable, a value the place the valuation is dear, and a value the place the valuation is suitable. The identical holds true with all mREIT widespread and BDC friends. As such, relating to my/our investing methodology, every mREIT widespread and BDC peer has their very own distinctive BUY, SELL, or HOLD suggestion vary (relative to estimated CURRENT BV/NAV). The higher-performing mREITs and BDCs usually have a suggestion vary at a premium to BV/NAV (various percentages primarily based on general outperformance) and vice versa with the typical/underperforming mREITs and BDCs (usually at a reduction to estimated CURRENT BV/NAV).

Every firm’s suggestion vary is “pegged” to estimated CURRENT BV/NAV as a result of this manner subscribers/readers can monitor when every mREIT and BDC peer strikes throughout the assigned suggestion ranges (each day if desired). That stated, the underlying reasoning why I/we place every mREIT and BDC suggestion vary at a special premium or (low cost) to estimated CURRENT BV/NAV is predicated on roughly 15-20 catalysts which embrace each macroeconomic catalysts/elements and company-specific catalysts/elements (each constructive and unfavourable). This investing technique is not for all market contributors. For example, unlikely a “good match” for very passive traders. For instance, traders holding a place in a selected inventory, regardless of the worth, for say a interval of 5+ years. Nevertheless, as proven all through my articles written right here at Searching for Alpha since 2013, within the overwhelming majority of cases I’ve been in a position to improve my private whole returns and/or reduce my private whole losses from particularly implementing this specific investing valuation methodology. I hope this supplies some added readability/understanding for brand new subscribers/readers relating to my valuation methodology utilized within the mREIT widespread and BDC sectors. Please disregard any minor “beauty” typos if/when relevant.

[ad_2]

Supply hyperlink