")

[ad_1]

imaginima

Writer’s Be aware: PART 2 of this text is a continuation from PART 1 which was mentioned in a earlier publication. Please see PART 1 of this text for an in depth projection of AGNC Funding Corp.’s (NASDAQ:AGNC) revenue assertion (technically talking, the corporate’s “consolidated assertion of complete revenue (loss)”) for the second quarter of 2022 relating to the next accounts: 1) curiosity revenue; 2) curiosity expense; 3) achieve (loss) on sale of funding securities, web; and 4) achieve (loss) on spinoff devices and different securities, web (together with 4 “sub-accounts”). PART 1 additionally mentioned AGNC’s projected web loss, earnings per share (“EPS”), and web unfold + web greenback roll (“NDR”) quantities. PART 1 assist results in a greater understanding of the matters and evaluation that might be mentioned in PART 2. The hyperlinks to PART 1 is offered under:

REIT Discussion board Model (Expanded Analytics):

Public Model:

Focus of Article:

The main focus of PART 2 of this text is to supply an in depth projection of AGNC’s consolidated assertion of complete revenue (loss) for the second quarter of 2022 relating to the next accounts: 5a) “unrealized achieve (loss) on funding securities measured at honest market worth (“FMV”) by means of web revenue, web”; and 5b) “unrealized achieve (loss) on available-for-sale (“AFS”) securities, web”. PART 2 additionally discusses AGNC’s projected different complete revenue (loss) (OCI/(OCL)) and complete revenue (loss) quantities. For readers who simply need the summarized account projections, I might counsel to scroll right down to the “Conclusions Drawn” part close to the underside of the article.

By understanding the developments that occurred inside AGNC’s operations through the second quarter of 2022, one can apply this data to sector friends as nicely. As such, the dialogue/evaluation under just isn’t solely relevant to AGNC however to the fixed-rate company mREIT sector as an entire. This consists of, however just isn’t restricted to, the next fixed-rate company mREIT friends: 1) ARMOUR Residential REIT, Inc. (ARR); 2) Cherry Hill Mortgage Funding Corp. (CHMI); 3) Dynex Capital, Inc. (DX); 4) Invesco Mortgage Capital Inc. (IVR); 5) Annaly Capital Administration, Inc. (NLY); 6) Orchid Island Capital, Inc. (ORC); and 7) Two Harbors Funding Corp. (TWO). It needs to be famous CHMI and TWO are additionally thought of fixed-rate company + mortgage servicing rights (“MSR”) mREIT friends and may very well be labeled as a separate sub-sector. Particularly, PART 2 gives a dialogue of fixed-rate company MBS worth actions which the entire sector friends listed above are at present closely invested in relating to honest market values (“FMV”).

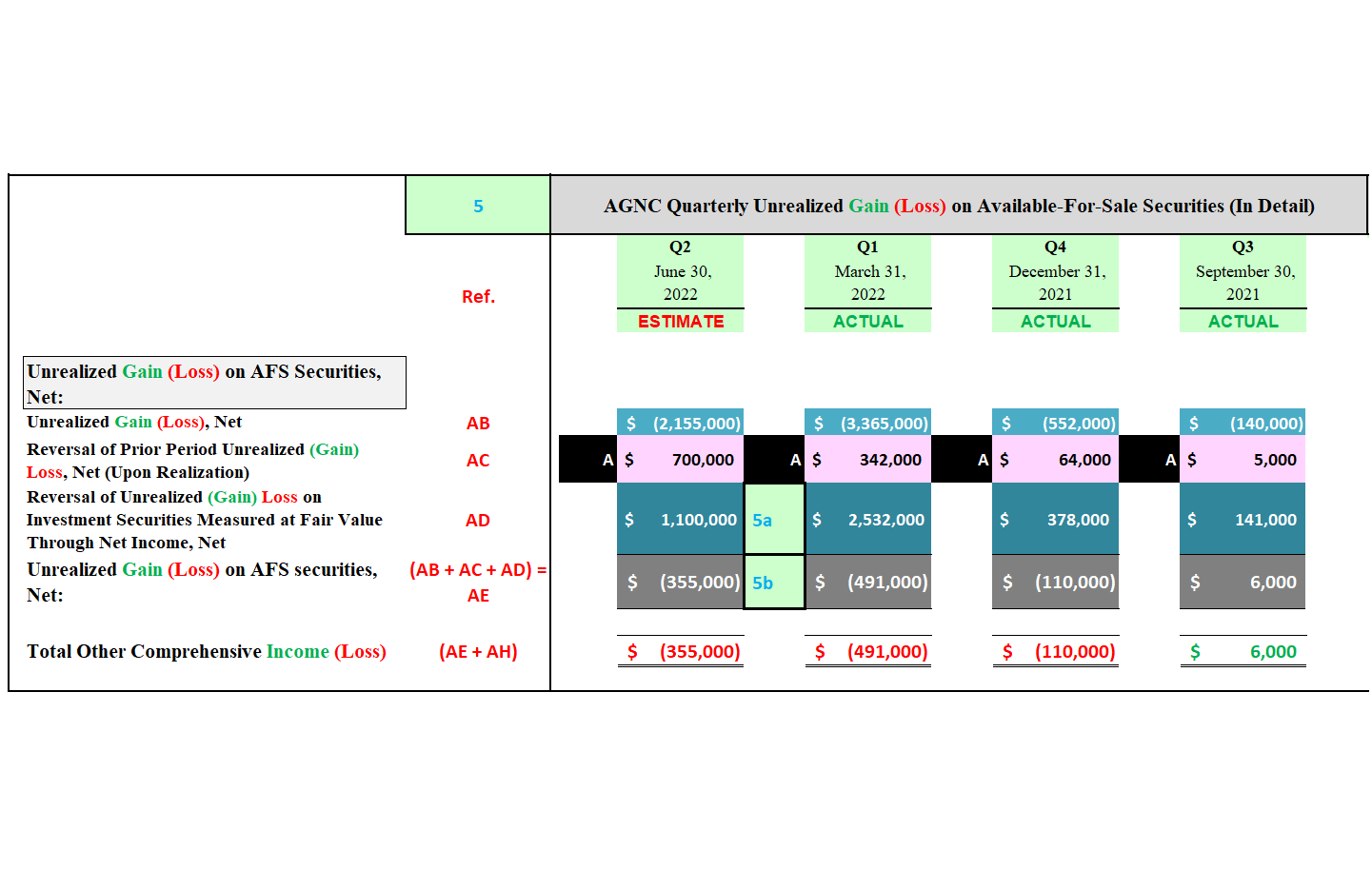

5a) Unrealized Acquire (Loss) on Funding Securities Measured at FMV Via Internet Earnings, Internet:

- Estimate of ($1.1) Billion; Vary ($1.35) Billion – ($850) Million

- Confidence Inside Vary = Average

- See Boxed Blue Reference “5a” in Desk 9 Beneath Subsequent to the June 30, 2022 Column

AGNC’s unrealized achieve (loss) on funding securities measured at FMV by means of web revenue, web account was created by the corporate a number of years in the past resulting from a change in accounting therapy of its MBS/funding portfolio. All unrealized FMV fluctuations on funding securities acquired on or after 1/1/2017 at the moment are acknowledged inside this account. All unrealized FMV fluctuations on funding securities acquired previous to 1/1/2017 proceed to be acknowledged within the account described subsequent. Since that is merely a monetary reporting/classification change, AGNC’s total MBS/funding portfolio is analyzed within the subsequent account (despite the fact that a rising portion of the portfolio is assessed within the account described right here).

5b) Unrealized Acquire (Loss) on AFS Securities, Internet:

- Estimate of ($355) Million; Vary ($555) – ($155) Million

- Confidence Inside Vary = Average to Excessive

- See Boxed Blue Reference “5a” in Desk 9 Beneath Subsequent to the June 30, 2022 Column

Projecting AGNC’s unrealized achieve (loss) unrealized achieve (loss) on AFS securities, web account is an evaluation that features a number of assumptions and variables that should be considered. Since this account is the summation of the quarterly unrealized valuation modifications inside AGNC’s MBS/funding portfolio (by far the most important asset class on the corporate’s stability sheet), a wider projection vary needs to be accompanied with this particular account. The identical assumptions used inside AGNC’s achieve (loss) on sale of funding securities, web account and achieve (loss) on spinoff devices and different securities, web account (relating to the corporate’s TBA MBS place; see PART 1 of article) apply when discussing this account.

Previous to performing an account projection evaluation, allow us to first analyze the fixed-rate “generic“ company MBS worth actions through the second quarter of 2022. Utilizing Desk 7 under as a reference, allow us to first analyze the 15-year fixed-rate company MBS worth actions. It will then be adopted by an analogous evaluation (through Desk 8) of the 30-year fixed-rate company MBS worth actions for a similar timeframe. By doing so, it will assist readers perceive how I start to provide you with my projected valuations mentioned later within the article.

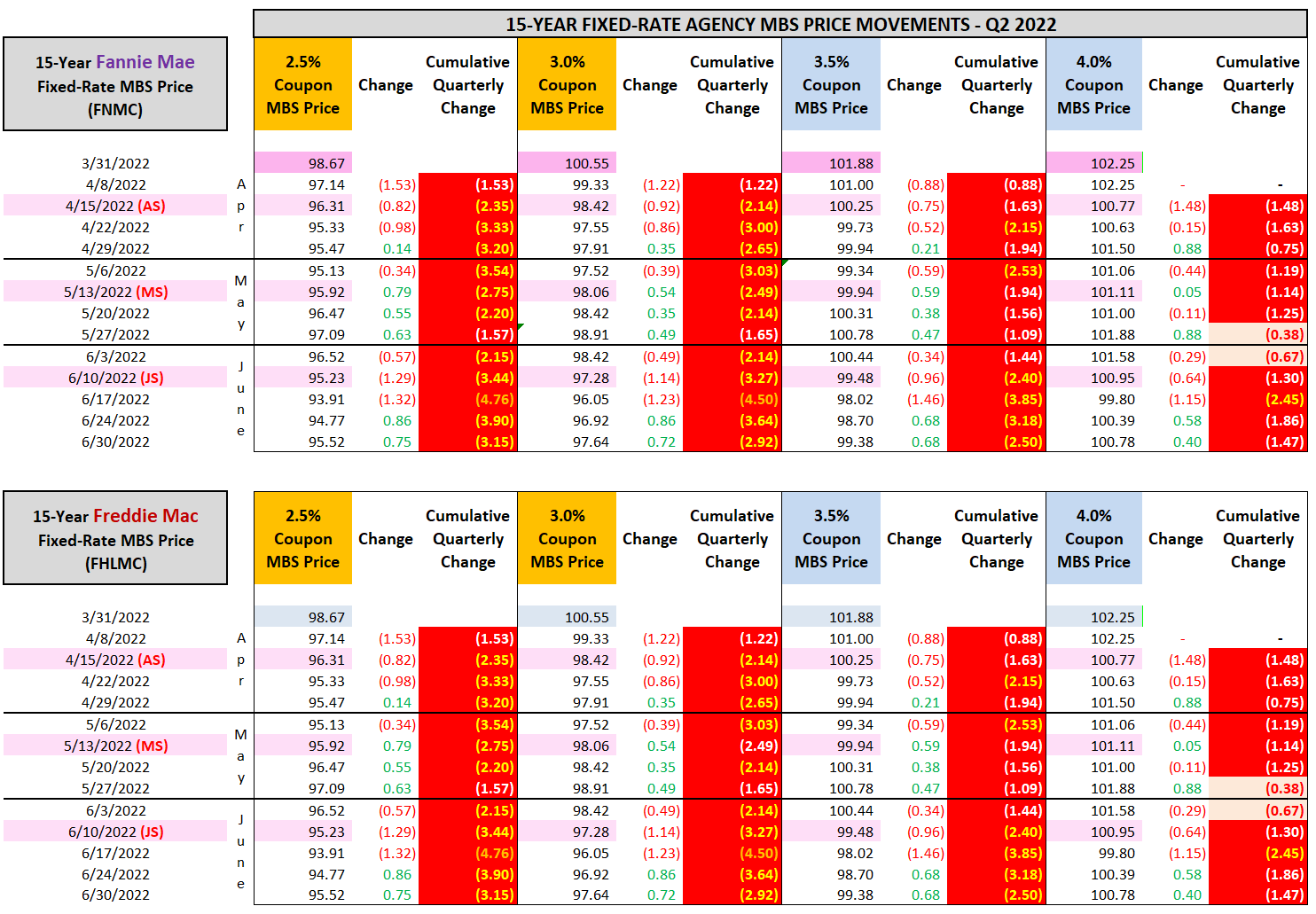

Desk 7 – 15-12 months Fastened-Fee Company MBS Value Actions (Q2 2022)

The REIT Discussion board

(Supply: Desk created by me, utilizing MBS pricing knowledge through non-public entry to knowledgeable useful resource [Thomson Reuters])

Desk 7 above exhibits the 15-year fixed-rate company MBS worth actions through the second quarter of 2022. It breaks out these company MBS holdings by “government-sponsored enterprise/entity” (“GSE”). This consists of each Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC) MBS. As of three/31/2022, AGNC’s Ginnie Mae holdings accounted for lower than 1% of the corporate’s MBS portfolio. As such, Ginnie Mae fixed-rate company MBS worth actions are deemed immaterial for dialogue functions and thus excluded from this desk. Desk 7 additional breaks out the 15-year fixed-rate company MBS worth actions into the varied coupons on AGNC’s books starting from 2.5% – 4.0%. AGNC at present holds an immaterial stability below the two.5% coupon and over the 4.0% coupon (no less than relating to generic MBS) and thus these particular coupons are excluded from Desk 7 above. From the data offered in Desk 7, a valuation achieve (loss) might be calculated which is damaged down by the varied coupons. It must also be famous AGNC regularly modifications the corporate’s MBS/funding portfolio in any given quarter. As such, I have to decide particular buy and sale assumptions in the direction of the top of my account projection evaluation (together with specified pool issues).

Utilizing Desk 7 above as a reference, allow us to have a look at the 15-year fixed-rate company MBS worth actions relating to coupon charges the place AGNC held a fabric stability as of three/31/2022. The cumulative quarterly web MBS worth actions for every coupon charge are proven inside Desk 7 below the “Cumulative Quarterly Change” column. For instance, through the second quarter of 2022, a Fannie 15-year fixed-rate company MBS with a 2.5%, 3.0%, 3.5%, and 4.0% coupon had a cumulative quarterly worth improve (lower) of (3.15), (2.92), (2.50), and (1.47) to settle its worth at 95.52, 97.64, 99.38, and 100.78, respectively. As such, a notable (at or larger than 0.75) worth lower occurred on the two.5%, 3.0%, 3.5%, and 4.0% coupons.

Merely put, as mortgage rates of interest/longer-term U.S. Treasury yields continued to shortly improve, extension threat continued to extend inside all coupon fixed-rate company MBS (which negatively impacted generic pricing). This common relationship was first mentioned in PART 1. It needs to be famous, firstly of 2020, there was a mix of Fannie and Freddie investments to create one “uniform/common” fixed-rate company MBS product. As such, in the case of this sort of funding, at present there may be one fixed-rate company Fannie/Freddie MBS product. Now that we’ve got an understanding of the 15-year fixed-rate company MBS worth actions through the second quarter of 2022, allow us to check out the 30-year fixed-rate company MBS worth actions.

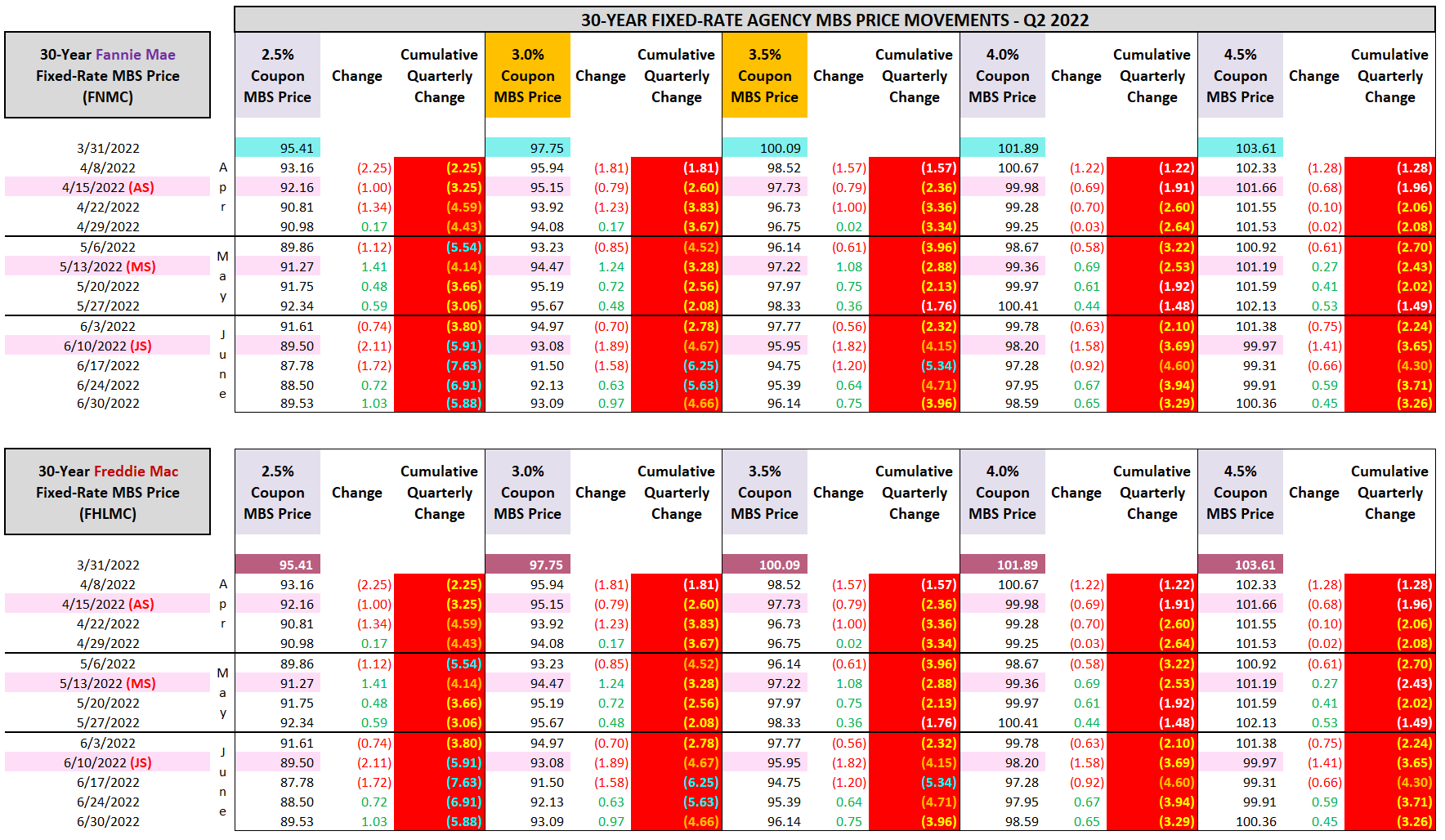

Desk 8 – 30-12 months Fastened-Fee Company MBS Value Actions (Q2 2022)

The REIT Discussion board

(Supply: Desk created by me, utilizing MBS pricing knowledge through non-public entry to knowledgeable useful resource [Thomson Reuters])

Desk Eight above exhibits the 30-year fixed-rate company MBS worth actions through the second quarter of 2022. It breaks out these MBS holdings by GSE as nicely. As said earlier, AGNC’s Ginnie Mae fixed-rate company MBS holdings are deemed immaterial for dialogue functions and are excluded from this desk. Desk Eight additional breaks out the 30-year fixed-rate company MBS worth actions into the varied coupons on AGNC’s books starting from 2.5% – 4.5%. AGNC at present holds an immaterial stability below the two.5% coupon (when contemplating the web (brief) TBA MBS place within the 2.0% coupon as of three/31/2022) and over the 4.5% coupon (no less than relating to generic MBS) and thus these particular coupons are excluded from Desk Eight above. From the data offered in Desk 8, a valuation achieve (loss) might be calculated which is damaged down by the varied coupons.

Utilizing Desk Eight above as a reference, allow us to have a look at the 30-year fixed-rate company MBS worth actions relating to coupon charges the place AGNC held a fabric stability as of three/31/2022. For instance, through the second quarter of 2022, a Fannie 30-year fixed-rate company MBS with a 2.5%, 3.0%, 3.5%, 4.0%, and 4.5% coupon had a cumulative quarterly worth improve (lower) of (5.88), (4.66), (3.96), (3.29), and (3.26) to settle its worth at 89.53, 93.09, 96.14, 98.59, and 100.36, respectively. As such, a notable worth lower occurred on the two.5%, 3.0%, 3.5%, 4.0%, and 4.5% coupons. Now that we’ve got an understanding of the 15- and 30-year fixed-rate company MBS worth actions through the second quarter of 2022, allow us to check out how I imagine these worth actions impacted AGNC’s MBS/funding portfolio from a valuation standpoint.

I’m projecting an “preliminary” web valuation lack of ($2.20) billion relating to AGNC’s on-balance sheet 15- and 30-year fixed-rate company MBS holdings for the second quarter of 2022. I might level out this projected determine considers the overwhelming majority of the corporate’s fixed-rate company MBS holdings had been inside varied varieties of “specified swimming pools” as of three/31/2022 and excludes its TBA MBS actions (that are thought of off-balance sheet spinoff devices per GAAP accounting). A lot of these investments are prepayment-protected holdings primarily by means of the Residence Inexpensive Refinance Program (“HARP”) and low-loan stability [LLB] securities. In a nutshell, the “pay-up”/premium related to these kinds of securitizations, when in comparison with “generic/TBA” MBS, continued to slim through the quarter (if not already at no premium). Merely put, market contributors turned way more open to the concept the rise in mortgage rates of interest/longer-term U.S. Treasury yields was “right here to remain”. As such, typically talking, specified pool pay-ups had been negatively impacted through the quarter; primarily inside increased, newer-production coupons.

After all, as is the case throughout any quarter, particular classifications, vintages, and underlying traits in the end impacted web valuation fluctuations. Detailed knowledge/evaluation in relation to AGNC’s specified swimming pools (over 25 totally different sub-classifications/vintages) is taken into account “proprietary knowledge” in the case of my tailor-made valuation fashions (which has taken quite a few man hours [and to be frank many quarters] to exactly “tweak”). If I had been to supply all of the “working elements” to my valuation fashions it’s analogous to Kentucky Fried Hen offering all of its rivals the “secret sauce” which makes their product style the very best. Merely put, then everybody can be utilizing the recipe and KFC suffers from a drop in gross sales (in my case it could probably be a drop in readership). That is why I’ve to set sure “boundaries” relating to sharing/exhibiting detailed quantitative knowledge/projections. With that stated, I nonetheless imagine myself (together with CO Wealth Administration Fund and his group) present, by far, probably the most particulars throughout the mREIT sector when contemplating each Market Providers and public readership. We’ve got a notable strategic benefit. Practically all different Looking for Alpha contributors primarily report earnings. As compared, I/we accurately-very precisely “challenge” earnings within the overwhelming majority of mREITs, every quarter (large distinction that gives super worth to readers/subscribers through recognizing worth dysfunctions by means of my/our valuation methodology).

As well as, by means of an in depth calculation that might be omitted from this explicit article, I’m projecting AGNC had a web valuation lack of ($25) million through the second quarter of 2022 regarding the following MBS holdings: 1) 20-year fixed-rate; 2) collateralized mortgage obligations (“CMO”); 3) adjustable-rate mortgages (“ARM”); 4) credit score threat transfers (“CRT”); and 5) AAA non-agency. Additionally, when contemplating the impacts of an assumed partial conversion of AGNC’s web lengthy TBA MBS place and the corporate’s realignment of its MBS/funding portfolio all through the quarter (change in leverage), I’m projecting a web valuation achieve of $70 million for the second quarter of 2022.

Due to this fact, when all of the figures said above are mixed, I’m projecting a complete web valuation lack of ($2.16) billion on AGNC’s on-balance sheet MBS/funding portfolio for the second quarter of 2022. This determine is prior to all bought MBS/investments being reversed out within the present quarter (mentioned in PART 1 of the article) and the reclassification of all MBS/investments bought after 1/1/2017. These two reversals are proven in Desk 9 under.

Desk 9 – AGNC Quarterly Unrealized Acquire (Loss) on AFS Securities, Internet Projection

The REIT Discussion board

(Supply: Desk created by me, partially utilizing AGNC knowledge obtained from the SEC’s EDGAR Database)

Desk 9 above exhibits AGNC’s projected complete web valuation lack of ($2.16) billion on the corporate’s MBS/funding portfolio (see crimson reference “AB”). This quantity is highlighted in teal. The second quantity proven is AGNC’s projected “reversal of prior interval unrealized (“achieve”) loss, web, (upon realization)” determine (see crimson reference “AC”). This quantity is highlighted in pink. The third quantity proven is AGNC’s projected “reversal of unrealized (“achieve”) loss on funding securities measured at FMV by means of web revenue, web” determine (see crimson reference “AD”). This quantity is highlighted in darkish teal.

After AGNC’s projected web realized loss on the sale of funding securities of $700 million and web unrealized loss on funding securities measured at FMV by means of web revenue of $1.10 billion are reversed out, the corporate’s complete web unrealized loss on AFS securities is projected to be ($355) million for the second quarter of 2022 (see crimson reference “(AB + AC + AD) = AE”). This quantity is highlighted in gray.

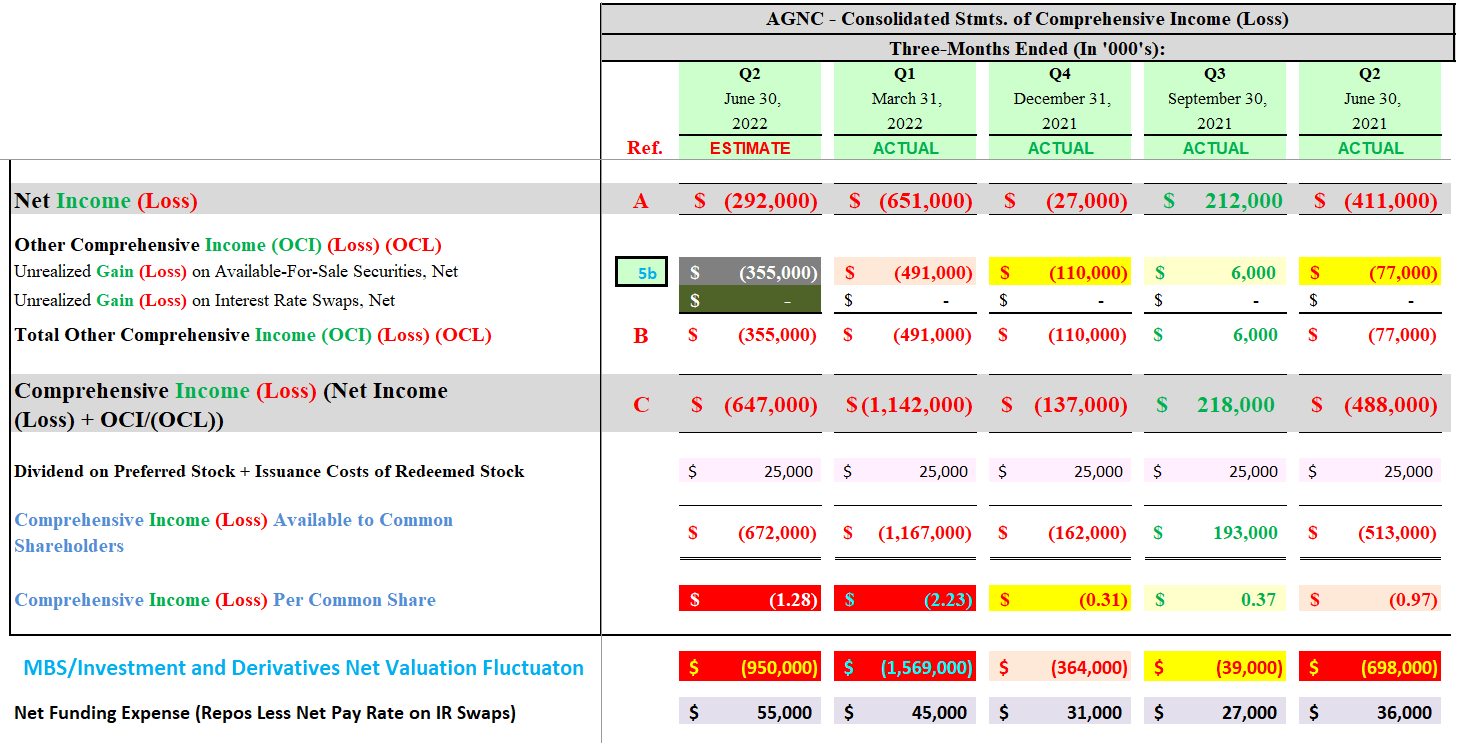

B) Different Complete Earnings (Loss) (OCI/(OCL)):

- Estimate of ($355) Million; Vary ($555) – ($155) Million

- Confidence Inside Vary = Average to Excessive

- See Purple Reference “B” in Desk 10 Beneath Subsequent to the June 30, 2022 Column

Allow us to now check out AGNC’s projected OCI/(OCL) and complete revenue (loss) quantities. This data is offered in Desk 10 under.

Desk 10 – AGNC Quarterly OCI/(OCL) and Complete Earnings (Loss) Projection

The REIT Discussion board

(Supply: Desk created by me, partially utilizing knowledge obtained from AGNC’s quarterly investor presentation slides)

After combining the corporate’s web unrealized loss on AFS securities of ($355) million and its web unrealized achieve on rate of interest swaps designated as money circulate hedges of $0 (AGNC now not classifies the corporate’s hedges this fashion), I’m projecting AGNC will report an OCL of ($355) million for the second quarter of 2022 (see crimson reference “B” in Desk 10 above).

C) Complete Earnings (Loss):

- Estimate of ($647) Million; Vary ($897) – ($397) Million

- Complete Loss Accessible to Widespread Shareholders of ($1.28) Per Share; Vary ($1.76) – ($0.81) Per Share

- Confidence Inside Vary = Average to Excessive

- See Purple Reference “C” in Desk 10 Above Subsequent to the June 30, 2022 Column

Conclusions Drawn From PART 1 and PART 2:

To sum up the evaluation from each elements of the article, I’m projecting AGNC will report the next quantities for the second quarter of 2022:

A) Quarterly Internet Lack of ($292) Million; Earnings Accessible to Widespread Shareholders of ($0.61) Per Share

B) Quarterly OCL of ($355) Million

C) Quarterly Complete Loss (A and B Mixed) of ($647) Billion; Complete Loss Accessible to Widespread Shareholders of ($1.28) Per Share

I imagine AGNC’s outcomes for the second quarter of 2022, with regard to valuation fluctuations, might be taken as neutral-slightly detrimental from “skilled” market contributors and really detrimental from “novice” market contributors. The important thing elements to research throughout the broader mREIT sector this quarter are the next: 1) every firm’s proportion of 15-year fixed-rate company MBS holdings versus 30-year fixed-rate company MBS holdings; 2) every firm’s hedging protection ratio; 3) every firm’s proportion of long-term spinoff devices versus short-term spinoff devices; 4) every firm’s “at-risk” leverage ratio; 5) every firm’s proportion of specified swimming pools (for example HARP and LLB securities); 6) every firm’s managerial experience; 7) every firm’s underlying asset composition relating to company versus non-agency/credit score investments; and 8) quantity of portfolio rotation into increased coupon investments. Dependent upon these elements, I imagine outcomes will modestly-notably range throughout the broader mREIT sector for the second quarter of 2022.

AGNC’s Projected BV as of 6/30/2022 and seven/15/2022:

When together with the figures derived from this two-part AGNC revenue assertion projection article, together with further figures/assumptions derived throughout the firm’s fairness part of its stability sheet, I’m projecting the next e book worth (“BV”) per widespread share figures as of 6/30/2022:

AGNC’s Projected Non-Tangible BV as of 6/30/2022 = $12.40 Per Widespread Share (Vary $11.95 – $12.85 Per Widespread Share)

AGNC’s Projected Tangible BV as of 6/30/2022 = $11.40 Per Widespread Share (Vary $10.95 – $11.85 Per Widespread Share)

When calculated, it is a projected quarterly non-tangible and tangible BV lower of ($1.73) and ($1.72) per widespread share, respectively. This calculates to a quarterly BV lower of (12.2%) and (13.1%), respectively. I’m additionally projecting AGNC generated a non-tangible and tangible “financial loss” (dividends accrued for/declared and web change in BV) of (9.7%) and (10.4%) for the second quarter of 2022, respectively.

Via an in depth evaluation that might be omitted from this explicit article, I’m projecting AGNC’s BV as of seven/15/2022 has fluctuated $0.00 – $0.50 per widespread share when in comparison with the corporate’s BV as of 6/30/2022. This projection excludes AGNC’s July 2022 month-to-month dividend of $0.12 per widespread share (ex-dividend is 7/28/2022).

My BUY, SELL, or HOLD Suggestion:

From the evaluation offered above, together with further catalysts/elements not mentioned inside this explicit article, I at present charge AGNC as a SELL after I imagine the corporate’s inventory worth is buying and selling at or larger than my projected non-tangible CURRENT BV (BV as of seven/15/2022), a HOLD when buying and selling at lower than my projected non-tangible CURRENT BV by means of lower than a (10%) low cost to my projected non-tangible CURRENT BV, and a BUY when buying and selling at or larger than a (10%) low cost to my projected non-tangible CURRENT BV. These ranges are unchanged when in comparison with my final AGNC article (PART 1 of this evaluation).

AGNC’s inventory worth closed at $12.22 on 7/21/2022.

Due to this fact, I at present charge AGNC as a HOLD.

As such, I at present imagine AGNC is appropriately valued from a inventory worth perspective. My present worth goal for AGNC is roughly $12.65 per share. That is at present the worth the place my advice would change to a SELL. The present worth the place my advice would change to a BUY is roughly $11.40 per share. Put one other means, the next are my CURRENT BUY, SELL, or HOLD per share advice ranges (the REIT Discussion board subscribers get this sort of knowledge on all 20 mREIT shares I at present cowl on a weekly foundation):

$12.65 per share or above = SELL

$11.41 – $12.64 per share = HOLD

$10.11 – $11.40 per share = BUY

$10.10 per share or under = STRONG BUY

Together with the info introduced inside this text, this advice considers the next mREIT catalysts/elements: 1) projected future MBS/funding worth actions; 2) projected future spinoff valuations; and 3) projected near-term (as much as 1-year) dividend per share charges. These suggestions additionally think about the Eight Federal (“Fed”) Funds Fee will increase by the FOMC throughout December 2016-2018 (a extra hawkish tone/rhetoric when in comparison with 2014-2016), the three Fed Funds Fee decreases throughout 2019 because of the extra dovish tone/rhetoric relating to general financial coverage because of current macroeconomic developments/occasions, and the very fast “plunge” within the Fed Funds Fee to close 0% in March 2020. This additionally considers the earlier wind-down/lower of the Fed Reserve’s stability sheet by means of gradual runoff/partial non-reinvestment (which started in October 2017 which elevated unfold/foundation threat) and the prior “easing” of this wind-down that began in Might 2019 relating to U.S. Treasuries and August 2019 relating to company MBS (which partially diminished unfold/foundation threat when volatility remained subdued). This additionally considers the early Spring 2020 announcement of the beginning of one other spherical of quantitative easing (“QE”) that features the Fed particularly buying company MBS (and “rolling over” all principal and curiosity funds into new company MBS) which bolstered costs whereas retaining long-term/mortgage rates of interest close to historic lows (which lowered unfold/foundation threat for fairly a while when volatility remained subdued). This additionally consists of the current “taper” of the Fed’s most up-to-date QE program relating to its month-to-month purchases of $80 billion of U.S. Treasury securities and $40 billion of company MBS. This taper started in November 2021 and market hypothesis round this future occasion has already brought on an increase in unfold/foundation threat through the summer time of 2021 and through the second half of the fourth quarter of 2021-June 2022 (as appropriately beforehand anticipated). This consists of the FOMC’s current accelerated taper timeline (which completed in March 2022 versus the prior anticipated timeline of June 2022) and the continued very probably fast rise within the Fed Funds Fee to 2.50%-3.25% by the top of 2022 which started again in March 2022. I imagine unfold/foundation threat ought to start to abate by the top of summer time 2022.

Present Sector/Latest NLY/AGNC Inventory Disclosures:

On 3/18/2020, I initiated a place in NLY at a weighted common buy worth of $5.05 per share (massive buy). This weighted common per share worth excluded all dividends acquired/reinvested. On 6/9/2021, I bought my total NLY place at a weighted common gross sales worth of $9.574 per share as my worth goal, on the time, of $9.55 per share was surpassed. This calculates to a weighted common realized achieve and complete return of 89.6% and 112.0%, respectively. I held this place for about 15 months.

On 3/18/2020, I as soon as once more initiated a place in AGNC at a weighted common buy worth of $7.115 per share (massive buy). This weighted common per share worth excludes all dividends acquired/reinvested. On 6/2/2021, I bought my total AGNC place at a weighted common gross sales worth of $18.692 per share as my worth goal, on the time, of $18.65 per share was surpassed. This calculates to a weighted common realized achieve and complete return of 162.7% and 188.6%, respectively. I held this place for about 14.5 months.

On 1/31/2017, I initiated a place in New Residential Funding Corp. (NRZ) at a weighted common buy worth of $15.10 per share. On 6/29/2017, 7/7/2017, and 12/21/2018, I elevated my place in NRZ at a weighted common buy worth of $15.775, $15.18, and $14.475 per share, respectively. When mixed, my NRZ place had a weighted common buy worth of $14.912 per share. This weighted common per share worth excluded all dividends acquired/reinvested. On 2/6/2020, I bought my total NRZ place at a weighted common gross sales worth of $17.555 per share as my worth goal, on the time, of $17.50 per share was surpassed. This calculates to a weighted common realized achieve and complete return of 17.7% and 41.2%, respectively. I held this place, on a weighted common foundation, for about 20 months.

On 9/22/2020, I as soon as once more initiated a place in NRZ at a weighted common buy worth of $7.645 per share. On 1/28/2021, 7/16/2021, 8/20/2021, 4/7/2022, 6/13/2022, 6/14/2022, and 6/17/2022, I elevated my place in NRZ at a weighted common buy worth of $9.415, $9.525, $9.485, $10.11, $9.345, $9.055, and $8.421 per share, respectively. When mixed, my NRZ place has a weighted common buy worth of $8.977 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

On half of/2020, I initiated a place in Arlington Asset Funding Corp. (AAIC) at a weighted common buy worth of $5.57 per share. On 1/9/2020, 3/16/2020, 9/24/2020, 5/6/2021, 9/2/2021, 9/10/2021, 11/10/2021, 11/24/2021, and three/3/2022, I elevated my place in AI at a weighted common buy worth of $5.59, $3.25, $2.53, $3.875, $3.748, $3.75, $3.752, $3.70, and $3.395 per share, respectively. When mixed, my AAIC place has a weighted common buy worth of $3.456 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

On 10/19/2020, I initiated a place in PennyMac Mortgage Funding Belief (PMT) at a weighted common buy worth of $16.275 per share. On 10/29/2020, 8/12/2021, 8/20/2021, 11/18/2021, 2/4/2022, and 4/19/2022, I elevated my place in PMT at a weighted common buy worth of $14.90, $18.693, $18.407, $18.180, $16.024, and $14.721 per widespread share, respectively. When mixed, my PMT place has a weighted common buy worth of $15.857 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

On 12/1/2020, I initiated a place in DX at a weighted common buy worth of $16.59 per share. On 12/20/2021, I elevated my place in DX at a weighted common buy worth of $15.35 per share. When mixed, my DX place has a weighted common buy worth of $15.66 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

On 10/12/2018, I initiated a place in Granite Level Mortgage Belief, Inc. (GPMT) at a weighted common buy worth of $18.155 per share. On 5/12/2020, 5/27/2020, 5/28/2020, 8/26/2020, 9/10/2020, and 9/11/2020, I elevated my place in GPMT at a weighted common buy worth of $4.745, $5.144, $5.086, $6.70, $6.19, and $6.045 per share, respectively. My final two purchases made up roughly 50% of my complete place (to place issues in higher perspective). When mixed, my GPMT place had a weighted common buy worth of $6.234 per share. This weighted common per share worth excluded all dividends acquired/reinvested. On 6/8/2021, I bought my total GPMT place at a weighted common gross sales worth of $15.783 per share as my worth goal, on the time, of $15.75 per share was surpassed. This calculates to a weighted common realized achieve and complete return of 153.2% and 168.7%, respectively. I held this place, on a weighted common foundation, for about 11 months.

On 12/10/2021, I as soon as once more initiated a place in GPMT at a weighted common buy worth of $11.817 per share. On 12/15/2021, 4/19/2022, and 4/29/2022, I elevated my place in GPMT at a weighted common buy worth of $11.318, $9.998, and $9.69 per share, respectively. When mixed, my GPMT place has a weighted common buy worth of $10.613 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

On 1/24/2022, I initiated a place in Prepared Capital Corp. (RC) at a weighted common buy worth of $13.39 per share. On 6/29/2022, I elevated my place in RC at a weighted common buy worth of $11.69 per share. When mixed, my RC place has a weighted common buy worth of $12.257 per share. This weighted common per share worth excludes all dividends acquired/reinvested.

Last Be aware: All trades/investments I’ve carried out over the previous a number of years have been disclosed to readers in “actual time” (that day on the newest) through both the StockTalks function of Looking for Alpha or, extra lately, the “stay chat” function of the Market Service the REIT Discussion board (which can’t be modified/altered). Via these sources, readers can lookup all my prior disclosures (buys/sells) relating to all firms I cowl right here at Looking for Alpha (see my profile web page for a listing of all shares coated). Via StockTalk disclosures and/or the stay chat function of the REIT Discussion board, on the finish of June 2022 I had an unrealized/realized achieve “success charge” of 83.9% and a complete return (consists of dividends acquired) success charge of 90.3% out of 62 complete previous and current mREIT and enterprise growth firm (“BDC”) positions (up to date month-to-month; a number of purchases/gross sales in a single inventory depend as one general place till totally closed out). I encourage different Looking for Alpha contributors to supply actual time purchase and promote updates for his or her readers/subscribers which might in the end result in larger transparency/credibility. Beginning in January 2020, I’ve transitioned all my real-time buy and sale disclosures solely to members of the REIT Discussion board. All relevant public articles will nonetheless have my buy and sale disclosures (simply not in actual time). Please disregard any minor “beauty” typos if/when relevant.

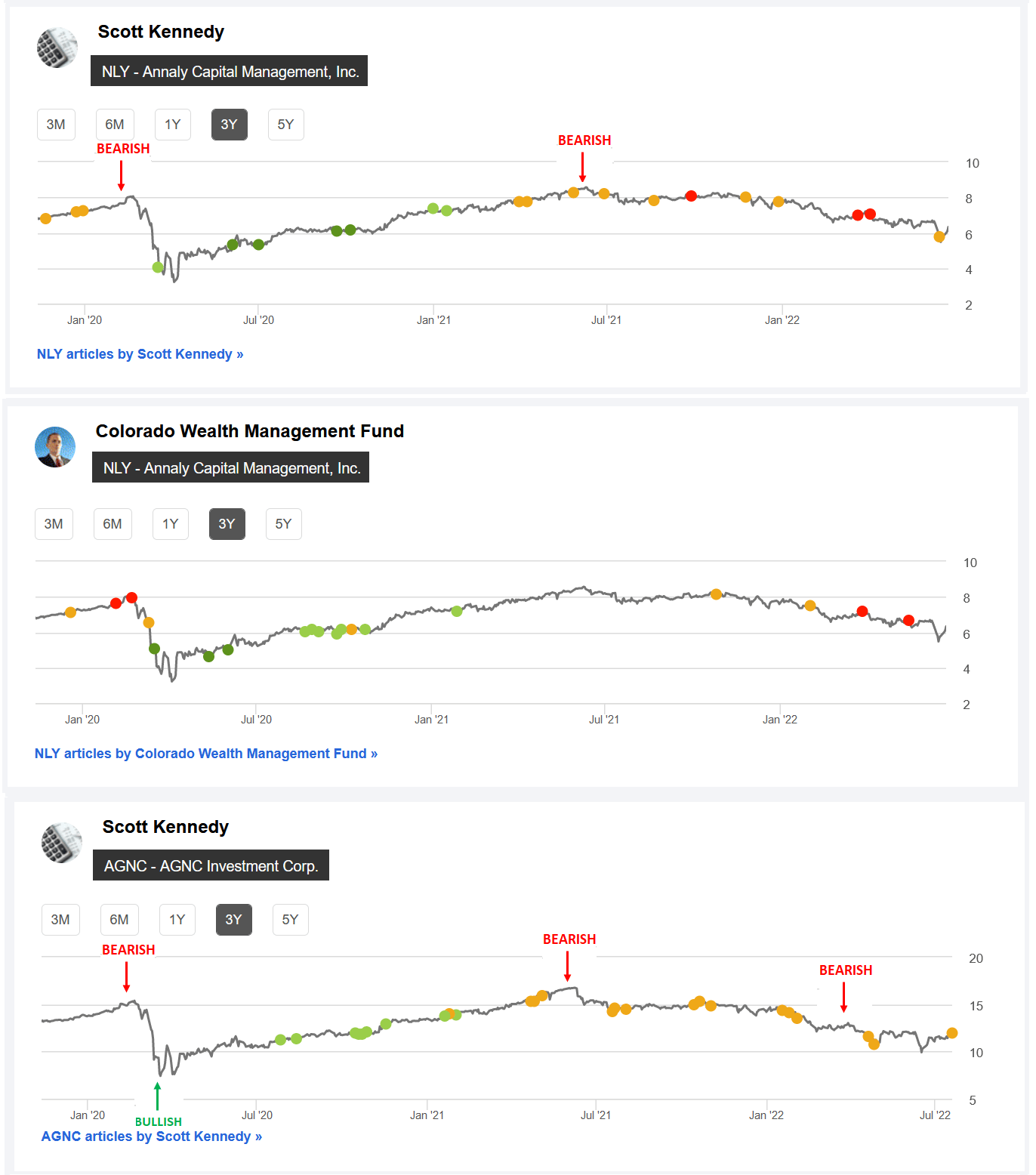

Desk 11 – The REIT Discussion board NLY + AGNC Looking for Alpha Suggestions (November 2019 – July 2022 Timeframe)

Looking for Alpha

(Supply: Desk immediately from Looking for Alpha; 1st AGNC “Bearish” indicator included by me immediately from the public AGNC article dated 2/5/2020 advice [which can’t be changed once public], AGNC “Bullish” indicator included by me immediately from the public AGNC article dated 4/17/2020 advice [which can’t be changed once public], 2nd AGNC and 1st NLY “Bearish” indicator included by me immediately from the REIT Discussion board’s weekly subscriber advice article collection [week of 6/4/2021 for AGNC and week of 6/11/2021 for NLY], and third AGNC “Bearish” indicator included by me immediately from the REIT Discussion board’s weekly subscriber advice article collection [week of 4/8/2022])

Lastly, I simply wish to shortly spotlight my/our AGNC and NLY Looking for Alpha advice ranges over the previous a number of years. In my private opinion, a inventory with a BUY advice ought to improve in worth over time, a SELL advice ought to lower in worth over time, and a HOLD advice ought to stay comparatively unchanged in worth over time (fairly logical). Merely put, my/our “valuation methodology” has appropriately timed when each AGNC and NLY have been undervalued (a BUY advice; bullish), overvalued (a SELL advice; bearish), and appropriately valued (a HOLD advice; impartial).

Utilizing Desk 11 above as a reference, I imagine we’ve got executed a reasonably good job in my/our AGNC and NLY advice rankings. For NLY, each pricing charts ought to actually be seen as 1 mixed chart since CO and I are a part of the identical Market service group. Not solely do I/we wish to present steering/a advice that enhances complete returns for subscribers, I/we additionally wish to shield these generated returns by subsequently minimizing complete losses. I personally imagine this system/technique is essential. In different phrases, appropriately recognizing each constructive catalysts/developments and detrimental elements/developments as financial and rate of interest cycles fluctuate.

This technique/technique was extraordinarily helpful/correct when going again to very late 2019 and early 2020 (each pre-COVID-19) the place I/we had a SELL advice on each AGNC and NLY. For some cause, this S.A. pricing chart doesn’t present my AGNC SELL advice pre-COVID-19 however one can merely look again to previous public articles in early 2020 (simply an omission on S.A.’s finish on this explicit case). Instead, merely have a look at the NLY SELL advice highlighted in CO’s pricing chart (AGNC and NLY sometimes have very comparable advice ranges when contemplating comparable time intervals). Moreover, after the preliminary “pandemic panic”, I/we had a STRONG BUY advice on each AGNC and NLY later within the spring of 2020.

Merely put, a contributor’s/group’s advice observe report ought to “depend for one thing” and may at all times be thought of in the case of credibility/profitable investing. You’ll not see most (if not all) different contributor groups use this sort of factual, recommendation-driven worth chart as a result of the outcomes usually are not practically as “enticing” when in comparison with our personal.

Every investor’s BUY, SELL, or HOLD resolution relies on one’s threat tolerance, time horizon, and dividend revenue objectives. My private advice is not going to match every reader’s present investing technique. The factual data offered inside this text is meant to assist help readers in the case of investing methods/choices.

Understanding My/Our Valuation Methodology Relating to mREIT Widespread and BDC Shares:

The essential “premise” round my/our suggestions within the mREIT widespread and BDC sectors is worth. Relating to operational efficiency over the long-term, there are above common, common, and under common mREIT and BDC shares. That stated, better-performing mREIT and BDC friends might be costly to personal, in addition to being low cost. Simply because a well-performing inventory outperforms the corporate’s sector friends over the long-term, this doesn’t imply this inventory needs to be owned at any worth. As with every inventory, there’s a worth vary the place the valuation is affordable, a worth the place the valuation is pricey, and a worth the place the valuation is suitable. The identical holds true with all mREIT widespread and BDC friends. As such, relating to my/our investing methodology, every mREIT widespread and BDC peer has their very own distinctive BUY, SELL, or HOLD advice vary (relative to estimated CURRENT BV/NAV). The higher-performing mREITs and BDCs sometimes have a advice vary at a premium to BV/NAV (various percentages based mostly on general outperformance) and vice versa with the typical/underperforming mREITs and BDCs (sometimes at a reduction to estimated CURRENT BV/NAV).

Every firm’s advice vary is “pegged” to estimated CURRENT BV/NAV as a result of this fashion subscribers/readers can observe when every mREIT and BDC peer strikes throughout the assigned advice ranges (each day if desired). That stated, the underlying reasoning why I/we place every mREIT and BDC advice vary at a special premium or (low cost) to estimated CURRENT BV/NAV relies on roughly 15-20 catalysts which embody each macroeconomic catalysts/elements and company-specific catalysts/elements (each constructive and detrimental). This investing technique is not for all market contributors. For example, unlikely a “good match” for terribly passive traders. For instance, traders holding a place in a specific inventory, regardless of the worth, for say a interval of 5+ years. Nonetheless, as proven all through my articles written right here at Looking for Alpha since 2013, within the overwhelming majority of situations I’ve been in a position to improve my private complete returns and/or decrease my private complete losses from particularly implementing this explicit investing valuation methodology. I hope this gives some added readability/understanding for brand new subscribers/readers relating to my valuation methodology utilized within the mREIT widespread and BDC sectors. Please disregard any minor “beauty” typos if/when relevant.

[ad_2]

Supply hyperlink