[ad_1]

Prospects of sustaining funding restoration are more likely to get tougher with a depreciating rupee and rising inflation

Prospects of sustaining funding restoration are more likely to get tougher with a depreciating rupee and rising inflation

The Finance Minister, Nirmala Sitaraman, mentioned lately that India’s long-term progress prospects are embedded in public capital expenditure programmes. She added that a rise in public funding would crowd in (or pull in) non-public funding, thus reviving the financial system. The Minister was talking on the third G20 Finance Ministers and Central Financial institution Governors (FMCBG) assembly hosted by Indonesia in Bali.

Lag in funding

Public investment-led financial progress has a decent educational pedigree, and varieties a reputable strand of clarification for India’s post-Independence financial progress. Right here is an illustration. When it was confronted with a slow-down after the Asian monetary disaster of 1997, the Atal Bihari Vajpayee led-Nationwide Democratic Alliance authorities initiated public highway constructing tasks. Within the type of the Golden Quadrilateral (to hyperlink metro cities utilizing a high-quality highway community) and the Pradhan Mantri Gram Sadak Yojana (to ‘present good all-weather highway connectivity to unconnected habitations’), these initiatives sowed the seeds of financial revival, culminating in an funding and export-led increase within the 2000s; GDP grew at 8%-9% yearly.

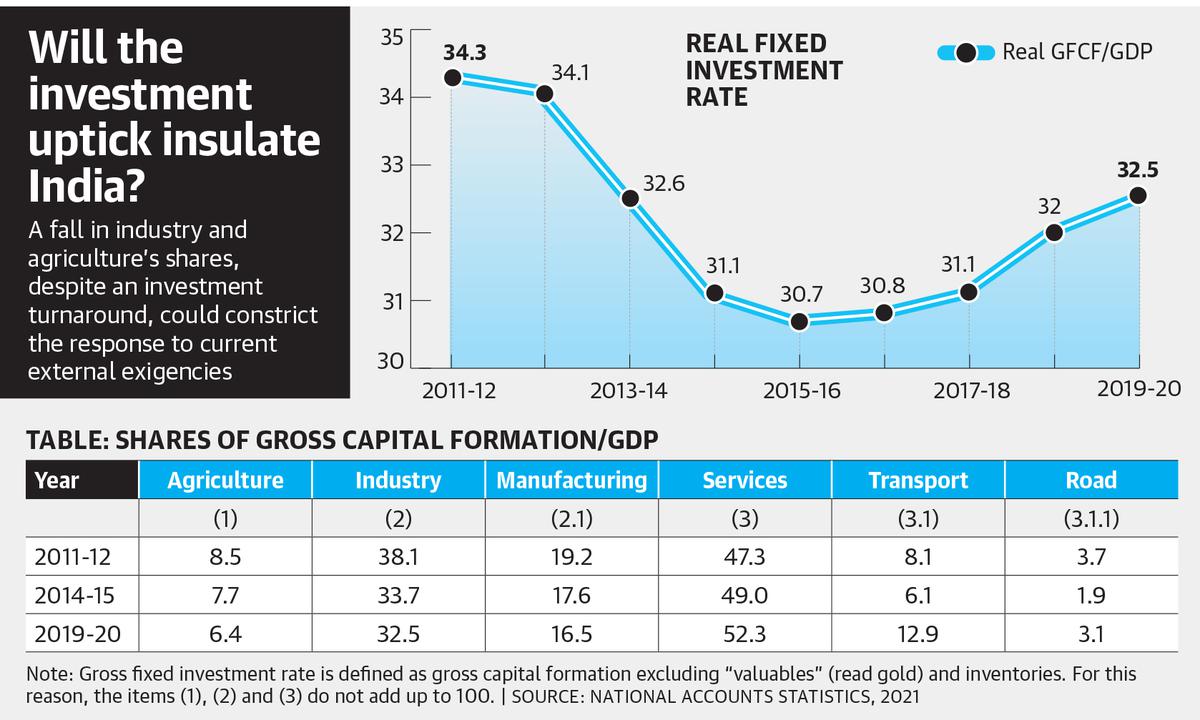

As compared, the funding report throughout the 2010s has been dismal. Nevertheless, a current uptick is clear in the actual gross fastened capital formation (GFCF) price — the fastened funding to GDP ratio (internet of inflation). The ratio recovered to 32.5% in 2019-20 from a low of 30.7% in 2015-16 (determine).

Ms. Sitaraman has claimed that the Authorities sustained the funding tempo even throughout the novel coronavirus pandemic (2020-21 and 2021-22). As within the June version of the Ministry of Finance’s Month-to-month Financial Evaluate, the fastened funding to GDP ratio was 32% in 2021-22. Nevertheless, there may be want for warning in studying the latest information, as they’re topic to revision. Furthermore, the budgetary definition of funding refers to monetary investments (which embrace buy of current monetary property, or loans provided to States) and never simply capital formation representing an enlargement of the productive potential.

On gross capital formation

The Nationwide Accounts Statistics offers disaggregation of gross capital formation (GCF) by sectors, kind of property and modes of financing; over 90% of GCF consists of fastened investments. The upturn within the funding price is welcome, although its productive potential is dependent upon its composition. Opposite to Ms. Sitaraman’s rivalry, the funding distribution has hardly modified during the last decade, with the general public sector’s share remaining 20%.

The desk exhibits the distribution of GCF by agriculture, trade and providers (columns 1 to three); inside providers transport (column 3.1) and inside transport, roads (the only largest expenditure merchandise; column 3.1.1).

Between 2014-15 and 2019-20, the shares of agriculture and trade in fastened capital formation/GDP fell from 7.7% and 33.7% to six.4% and 32.5%, respectively. Providers’ share rose to 52.3% in 2019-20 in comparison with 49% in 2014-15. The rise within the providers sector is sort of completely on transport and communications. The share of transport has doubled from 6.1% to 12.9% throughout the identical interval. Inside transportation, it’s principally roads.

As roads and communications are basic public items, funding in them is welcome. However over-emphasising it might be lop-sided. For wholesome home output progress, there’s a want for stability between “instantly productive investments” (in farms and factories) and infrastructure investments. And this stability was missed. Furthermore, the share of agriculture and trade shrank even because the financial system’s gross capital formation price trended downwards (see determine).

Import dependence grew

The case of producing is distressing. Its share within the funding ratio (column 2.1) fell from 19.2% in 2011-12 to 16.5% in 2019-20. It isn’t stunning that ‘Make in India’ didn’t take off, import dependence went up, and India turned deindustrialised. Import dependence on China is alarming for essential supplies reminiscent of fertilizers, bulk medication (lively pharmaceutical components or APIs) and capital items. This turned acute throughout the COVID-19 pandemic, as China imposed export restrictions — prompting the Prime Minister to announce the ‘Atmanirbhar Bharat’ marketing campaign.

As a substitute of boosting funding and home technological capabilities, the ‘Make in India’ marketing campaign frittered away time and assets to boost India’s rank within the World Financial institution’s (questionable and contested) Ease of Doing Enterprise Index. India’s place did go up, from 142 in 2014 to 63 in 2019, but it surely failed to spice up industrial funding, not to mention international funding.

The contribution of international capital to financing GCF fell to 2.5% in 2019-20 from 3.8% in 2014-15 (or 11.1% in 2011-12). With declining funding share, industrial output progress price fell from 13.1% in 2015-16 to a destructive 2.4% in 2019-20, as per the Nationwide Accounts Statistics.

Public funding

The Finance Minister has claimed that public funding is the pivot of the continued investment-led financial revival. The current upturn within the combination fastened capital formation to GDP ratio is optimistic, although the speed remains to be decrease than its mark within the early 2010s. The declare that the funding revival is public sector pushed shouldn’t be borne out by info. The jury should still be out on the urged rise in public funding throughout the COVID-19 pandemic. The budgetary figures consult with monetary funding, not estimates of capital formation, indicating enlargement of the financial system’s productive capability.

Through the 2010s, the funding shares of agriculture and trade fell however rose sharply in providers. The share share for roads has doubled. The enlargement of roads and communications is unquestionably welcome. Contemplating such a skewed funding precedence, the ‘Make in India’ technique didn’t take off, accentuating India’s import dependence, particularly on China, resulting in deindustrialisation.

The dearth of home capability for important uncooked industrial supplies and capital items may show expensive. It should probably check India’s potential to resist exterior financial challenges. With a depreciating forex and rising (imported) inflation, prospects of sustaining funding restoration are more likely to get tougher. The deficit on stability of fee is already properly above coverage makers’ consolation stage of two.5% of GDP.

R. Nagaraj is with the Centre for Improvement Research, Thiruvananthapuram. The views expressed are private

[ad_2]

Supply hyperlink