[ad_1]

Even after the greater than 9% rally for U.S. shares in July, we proceed to view the broad U.S. fairness market as materially undervalued, albeit much less low cost than it was initially of the quarter. Based on a composite of the valuations of the just about 700 shares we cowl that commerce within the U.S., the market is now at an 11% low cost to honest worth.

Fairness markets bottomed out in mid-June after which remained in a buying and selling vary till mid-July as buyers awaited second quarter outcomes. Earnings had been combined as a number of high-profile misses despatched some particular person shares plunging. However quarterly outcomes had been usually not as unhealthy because the market had anticipated.

Much more importantly although, administration groups didn’t throw within the towel on the second half of 2022. Firm executives appeared to dampen expectations however largely didn’t make wholesale reductions to their earnings outlook for the rest of this yr. With valuations at already low ranges following the selloff in late spring and early summer time, this supplied the market with sufficient confidence to start out re-allocating capital again into equities.

Key Takeaways for the Inventory Market At present:

U.S. Inventory Market at 11% Low cost to Truthful Worth

In our Q3 outlook we famous that we thought U.S. fairness markets had been changing into oversold, and that since 2010, shares had not often traded at as nice of a reduction to their intrinsic worth. The truth is, in mid-June, shares had been buying and selling at their best low cost to our long-term, intrinsic valuations for the reason that emergence of the pandemic in March 2020, and the expansion scare that despatched shares decrease in December 2018.

On an extended historic time-frame, the one different occasion when our value/honest worth metric had dropped decrease was within the fall of 2011 amid fears the Greek debt disaster would unfold to different international locations.

Following the rally within the second half of final month, as of July 29, the broad U.S. fairness market is buying and selling at an 11% low cost to our honest worth.

Progress shares surged 14.2% in July, simply outperforming the broader market. Following this acquire, these shares at the moment are buying and selling at a reduction much like worth shares, whereas core shares stay nearer to honest worth. As such, we proceed to favor a barbell formed portfolio break up between overweighting worth and development shares and underweighting core shares.

The Morningstar US Small Cap Index barely outperformed in July, rising 10.1%, and small-cap shares stay essentially the most undervalued by market capitalization. Massive- and mid-cap shares carried out in-line with the broader market and each classes are equally undervalued.

Look to Cyclicals, Economically Delicate Sectors for Worth

Throughout our sector valuations, communication companies stays essentially the most undervalued a part of the market by far at 33%, adopted by a number of cyclical sectors which had suffered the brunt of the selloff over the previous few months. Defensive sectors, which held their worth higher to the draw back, are pretty to overvalued.

Of notice, over half of the market capitalization of the communications sector is concentrated in Alphabet (GOOGL) and Meta Platforms (META). Following earnings, we lowered our honest worth on Alphabet by 6.1% to $169 to account for near-term weak point. Nevertheless, we expect the market is extrapolating this short-term weak point too far into the long run. Even after chopping again our honest worth estimate, the inventory stays in 4-star territory and trades at a 32% low cost to our intrinsic valuation.

We additionally lowered our valuation on Meta by 9.9% to $346 following poor second quarter outcomes and weak steerage. Much like Alphabet, we expect the market is overly pessimistic relating to Meta’s long-term outlook. For instance, primarily based on Meta’s persevering with person development, we consider the corporate’s community impact stays intact, which is the idea of our broad moat score. We count on additional monetization of its Reels product together with an financial turnaround to return top-line development to the low- to mid-teens vary starting within the second half of 2023. Meta’s inventory trades at lower than half of our intrinsic valuation, putting it deep within the 5-star score class.

Additionally of notice within the communications sector, we lowered our valuation of Twitter (TWTR) to $44 per share. We had moved our honest worth to Elon Musk’s buyout supply of $54.20 after the corporate accepted his buyout supply. However following his submitting to terminate the deal we’ve revised our valuation, which is now primarily based upon the underlying fundamentals of Twitter as a public firm.

Client cyclical stays the second-most undervalued sector, buying and selling at a 16% low cost to honest worth. With the financial system weakening within the first half of the yr, this sector had been the worst performing a part of the market throughout that point. We expect one of the best alternatives are in these areas that stand to realize from a normalization of client conduct. We count on spending will proceed to shift again into companies in the direction of pre-pandemic ranges and away from items, which had outperformed in the course of the pandemic. For a extra in-depth dialogue of those alternatives, please see Spending Is Shifting Again to Companies; Right here’s The place to Make investments Now.

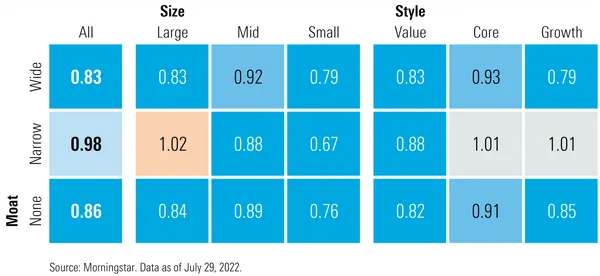

Indiscriminate Promoting Throughout Downturn Leaves Vast Moat Shares at a Low cost

In the course of the worst of the selloff we famous that with the intention to meet redemptions many portfolio managers resorted to promoting what they might versus what they needed. Shares of high-quality firms will sometimes have a deeper pool of liquidity to promote into than lower-quality names.

Because of this indiscriminate promoting, shares with Vast Financial Moats are buying and selling at a better low cost than shares of firms with both Slim or No Moat scores.

We proceed to see a big quantity of worth for long-term buyers in Vast Moat shares. Along with their decrease valuations, we additionally count on these firms usually to have better pricing energy. As such, they need to be capable to go by way of any value will increase to shoppers and be capable to higher preserve their margins, and thus maintain their valuations in an inflationary atmosphere.

Outlook

We proceed to view the broad U.S. fairness market as materially undervalued. Nevertheless, even on the present degree, long-term buyers ought to brace themselves and count on volatility to proceed over the following a number of months.

In our 2022 outlook we famous that there have been a number of headwinds the market was going to must cope with this yr. The 2 that the market will now most intently be anticipating are an financial restoration and moderating inflation. Over the following few months, markets might be searching for indicators that these challenges are starting to abate. Any metrics that point out the financial system is constant to weaken and/or that inflation will stay hotter for longer would probably put renewed downward strain on shares.

Based mostly on our forecasts, we expect each of those headwinds ought to start to shift into tailwinds. For instance, even after accounting for the unfavourable gross home product stories within the first and second quarter, we’re nonetheless projecting actual GDP development of two% this yr. We expect inflation has peaked and may start to reasonable from right here on out.

“The June [CPI] report will nearly definitely mark the height in inflation, as meals and power costs are set to fall sharply in subsequent month’s report,” says Morningstar’s chief U.S. economist Preston Caldwell.

We encourage market members to stay with plans that steadiness long-term funding objectives with their danger tolerances. These plans ought to permit for periodic rebalancing to extend fairness allocations when valuations decline, but in addition cut back publicity when valuations change into overextended. Based mostly on our view that the U.S. fairness market is undervalued, we expect now just isn’t the time to be lowering fairness exposures however to be including to them judiciously—particularly in firms with broad financial moats.

[ad_2]

Supply hyperlink