")

[ad_1]

Klaus Vedfelt

Thesis

Apollo Tactical Earnings Fund, Inc. (NYSE:AIF) is a hard and fast revenue closed-end fund (“CEF”). The automobile accommodates a mixture of leveraged loans and excessive yield bonds with a basic 70% / 30% allocation between the asset lessons. As per the fund literature:

Apollo seeks to generate present revenue and preservation of capital primarily by allocating the Fund’s belongings amongst several types of credit score devices primarily based on absolute and relative worth concerns and its evaluation of the credit score markets. Underneath regular market situations the Fund invests not less than 80%of its managed belongings (which incorporates leverage) in credit score devices and investments with comparable financial traits.

Supply: Fund Reality Sheet

The fund is on the smaller aspect with a $180mm AUM and sports activities a 9.4% yield. The fund is a typical “CLO mild” fund, with a 70/30 allocation to leveraged loans and excessive yield bonds and a excessive 37% leverage ratio. The leverage ratio is on the excessive aspect for the CEF area as a result of low volatility that traditionally has been uncovered by the senior secured mortgage asset class.

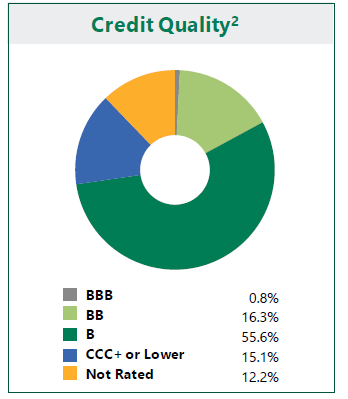

Regardless of its collateral being on the backside of the credit score spectrum (excessive focus of “B” and “CCC” credit, which account for over 70% of the underlying portfolio), the fund has carried out properly in 2022, being down solely -16% on a complete return foundation this yr. This efficiency exceeds the one uncovered by a lot better identified names, such because the Eaton Vance Floating-Fee Earnings Belief (EFT) or Ares Dynamic Credit score Allocation Fund Inc (ARDC).

The primary driver for fund efficiency consists of credit score spreads. Since many of the collateral is floating fee, length is a secondary issue. Credit score spreads are significantly necessary as a result of collateral composition (low score) and excessive leverage within the fund. Credit score spreads have widened and have breached the “normalized setting” vary:

Credit score Sprads (the Fed)

Whereas we don’t suppose they may revisit the 2015/2016 or Covid-19 disaster highs, there could be one other 100 bps in widening to slowly happen. We really feel shopper and institutional stability sheets are in a lot better form that in different recessionary situations and precise default charges should not going to tick up that top throughout this cycle.

AIF is an efficient, low commonplace deviation automobile to play a credit score restoration. Nonetheless we really feel the market is just not completely carried out with wider credit score spreads, regardless of the current panic we noticed in June. We’ve AIF at Maintain for now and are eager to see an finish to the rate of interest hikes earlier than shifting ahead with a distinct sign for this extremely leveraged automobile.

Analytics

AUM: $0.18 billion.

Sharpe Ratio: 0.19 (5Y).

St Deviation: 11.2 (5Y).

Yield: 9.4%.

Expense Ratio: 2.92%.

Premium/Low cost to NAV: -12.8%.

Z-Stat: -1.2.

Leverage Ratio: 37%.

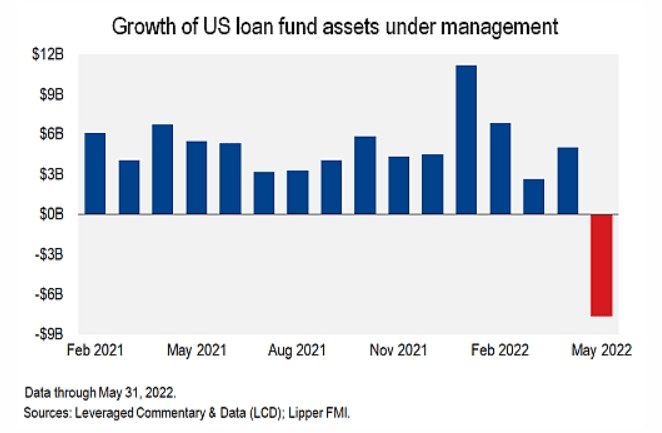

Present State of the Leveraged Mortgage Market

Leveraged loans have began to see vital outflows this yr as properly, following excessive yield fastened bonds:

US excessive yield fund outflows have reached over $33 billion this yr, or almost 10% of HY belongings beneath administration on the finish of 2021. Leveraged loans, which had inflows for a lot of the early a part of the yr, have just lately skilled two consecutive weeks of outflows together with the biggest weekly outflow since March 2020. The Credit score Suisse Leveraged Mortgage Index is down 3.3% and the Bloomberg US Excessive Yield 2% Issuer Capped Index is down 1.8% for the month of Might (as of Might 25). 12 months so far (as of Might 25), the benchmarks are down 3.2% and 9.8%, respectively.

Supply: GS

A visible illustration of inflows / outflows under, courtesy of LCD:

Outflows (liquid crystal display)

Nonetheless, the rise in danger free charges coupled with wider credit score spreads have introduced all-in yields within the area above 8%. This alerts sturdy returns forward, as per GS:

On the heels of the current sell-off, LL yields incorporating the ahead curve are actually above 8% for less than the fifth time for the reason that 2008-2009 monetary disaster. Traditionally, shopping for each LL and HY when yields are above 8% has generated sturdy ahead returns.

Supply: GS

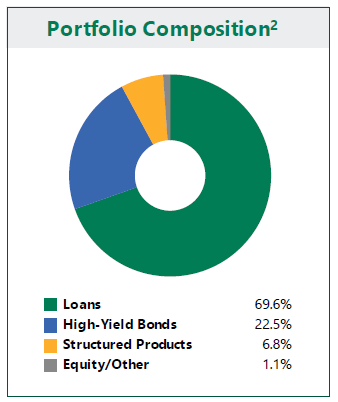

Holdings

The fund holds a mixture of leveraged loans, excessive yield bonds, and a really small allocation to CLOs:

Portfolio Composition (Fund Reality Sheet)

The fund tends to be targeted on the decrease rungs of the credit score spectrum:

Credit score High quality (Fund Reality Sheet)

We will see from the above desk that many of the exposures sit within the single “B” bucket, whereas “CCC”s even have a excessive allocation. With a possible recession upcoming it’s not ultimate to run such excessive credit score danger.

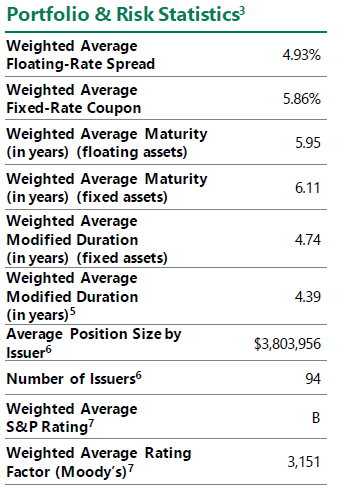

The fund runs a length shut to five years and has a mean fastened fee coupon profile:

Portfolio Statistics (Fund Reality Sheet)

Efficiency

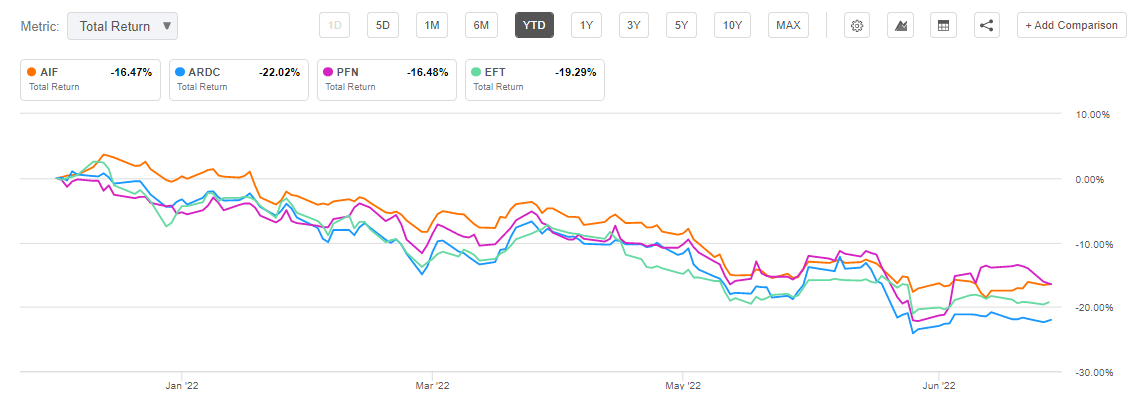

The fund is down greater than -16% on a complete return foundation year-to-date, beating a few of its extra well-known friends within the trade:

YTD Efficiency (Searching for Alpha)

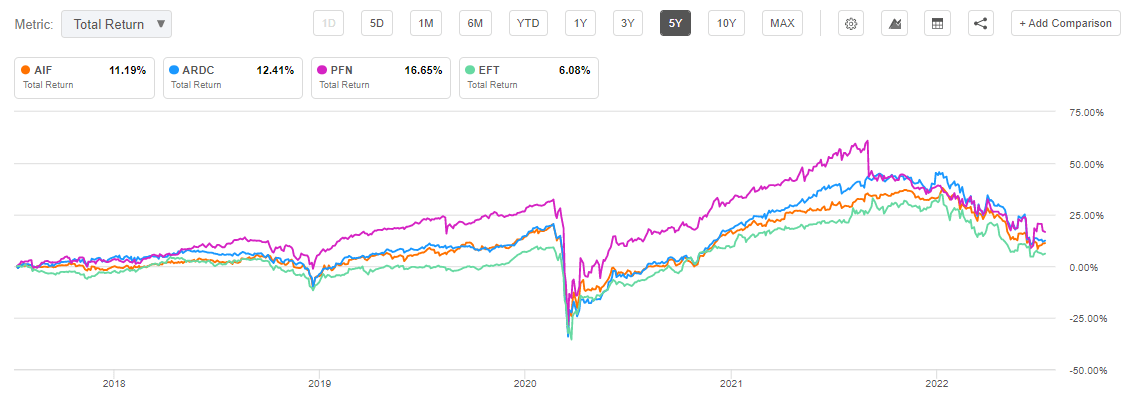

On a 5-year foundation the image is pretty comparable with AIF displaying a sturdy efficiency:

5-12 months Efficiency (Searching for Alpha)

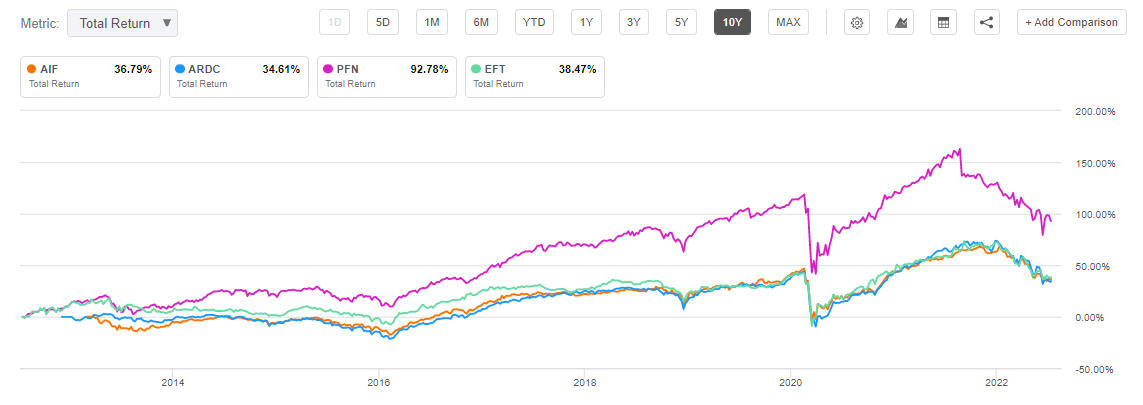

A decade lengthy graph paints a two-cohort image, with AIF being consistent with two different floating fee funds, however underperforming a well-known PIMCO fund, Pimco Earnings Technique Fund II (PFN) (to be honest, PFN solely has a 30% allocation to leveraged loans, therefore different danger elements come into play):

10-Y Efficiency (in search of alpha)

Premium/Low cost to NAV

The fund is presently buying and selling at a -12.5% low cost to NAV, which is on the vast aspect from a historic standpoint:

Premium/Low cost to NAV (Morningstar)

We will see from the above desk sourced from Morningstar that the widest low cost to NAV for the fund was recorded in 2020, when the market moved the value to an -18% low cost to web asset worth.

Conclusion

AIF is a leveraged mortgage/excessive yield bond CEF from Apollo. The fund has a excessive focus of low rated credit (“B” and “CCC”) and a excessive leverage ratio of 37%. AIF has carried out pretty robustly this yr being down solely -16% and its low cost is near historic highs at a -12.5% stage. We count on the fund to represent an excellent play for a restoration in credit score, however have it at Maintain for now, ready for the rate of interest image to normalize which must also mark a prime in credit score spreads, the principle danger issue for the fund.

[ad_2]

Supply hyperlink