[ad_1]

Panuwat Dangsungnoen/iStock by way of Getty Pictures

That is an replace to our sequence of articles began in 2012 assessing market valuation and estimating ahead inventory market returns. The latest earlier replace was June 2022 with finish of Might 2022 values.

The December 2021 replace concluded that the then prevailing situation of overvaluation recommended zero returns from shares to the top of 2028 and the hazard of an imminent main downturn for equities.

By finish of Might 2022 the S&P 500 was 14% down from the December 2021 common, and since then the index has declined 4% to finish of June 2022. For the S&P 500 to achieve the long-trend would entail an extra 33% decline, presumably over a brief interval.

The projections listed here are partly based mostly on “Estimating Ahead 10-Yr Inventory Market Returns utilizing the Shiller CAPE Ratio and its 35-Yr Transferring Common”, which is known as the “referenced article” additional down.

What Brief-Time period Inventory Market Returns Can Be Anticipated?

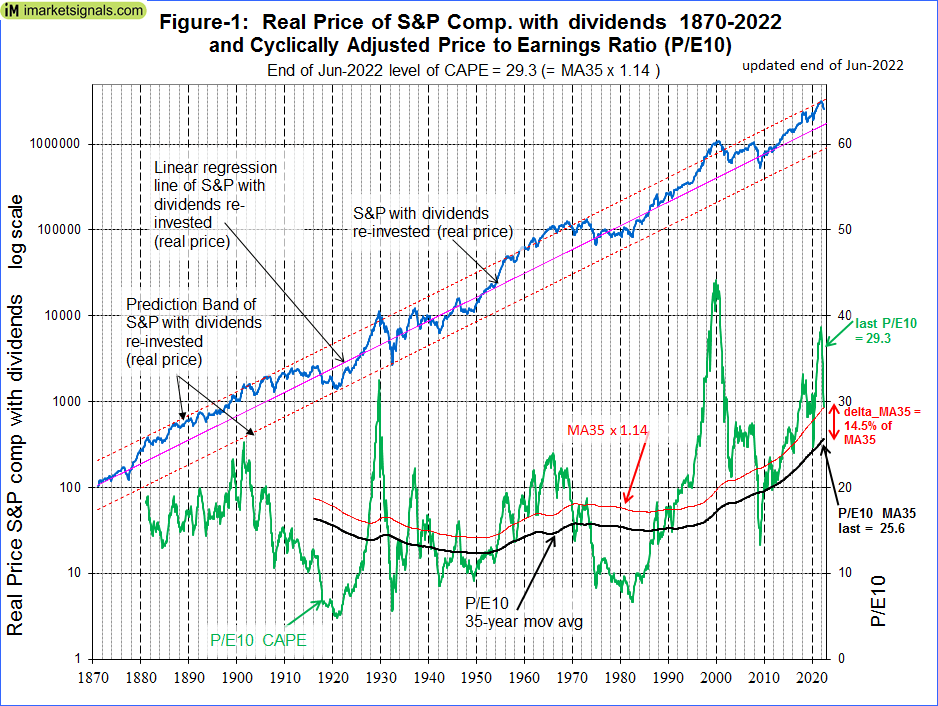

No one is aware of, and the most effective one can do is to make use of the historic information (which is from Shiller’s S&P sequence) to information us to make estimates for the long run. From the actual value of the S&P-Composite with dividends re-invested (S&P-real) one finds that the best-fit line from 1871 onward is a straight line when plotted to a semi-log scale. There isn’t a motive to consider that this long-term development of S&P-real will probably be interrupted. S&P-real, up to date to finish of June 2022 and the most effective match line along with its 95% prediction band are proven in Determine-1. (See appendix for the equation.)

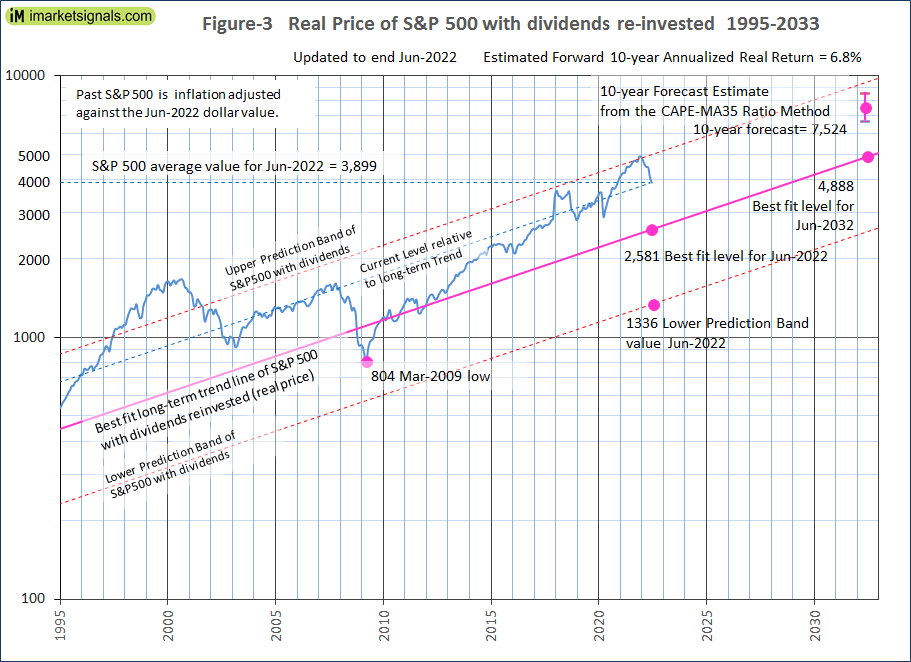

The typical June degree of three,899 is 51% above the long-term development line (Determine-3). Reverting to the imply development would entail a 33% decline.

iMarketSignals

Forecasting Inventory Market Returns With The CAPE-MA35 Ratio

Additionally proven in Determine-1 are the CAPE (which is the S&P-real divided by the common of the actual earnings over the previous 10 years) and its 35-year transferring common (MA35), having finish of June 2022 values of 29.Three and 25.6, respectively. Thus, the falling CAPE is now solely about 15% above the MA35 and the S&P-real has now sharply declined from the higher prediction band line the place it was finish of December 2021.

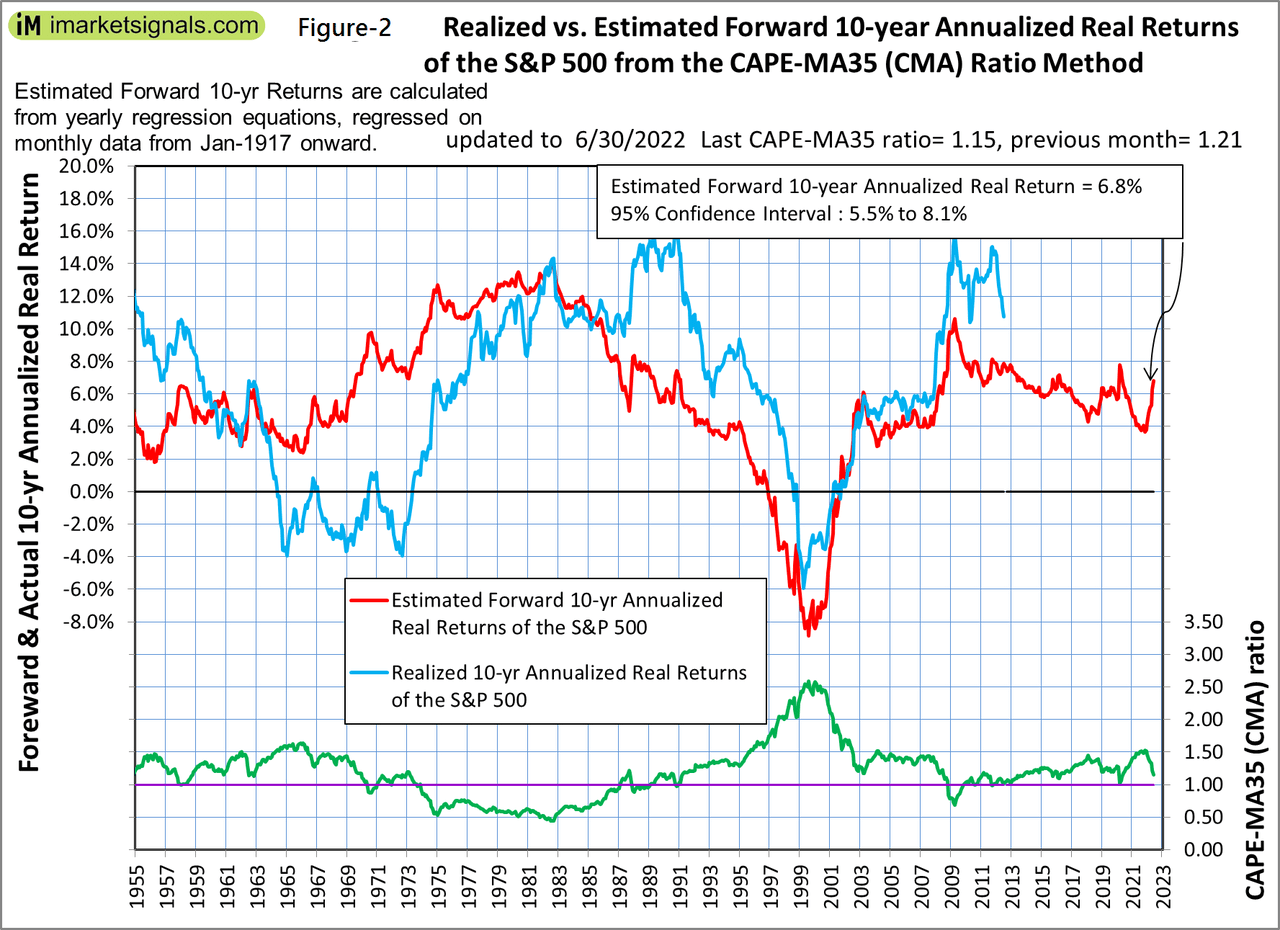

As proven within the referenced article, a superior technique to the usual use of the Shiller CAPE-ratio is to foretell 10-year actual returns utilizing the CAPE-MA35 ratio as a valuation measure. It’s merely the worth of the Shiller CAPE-ratio divided by the corresponding worth of its 35-year transferring common (29.3 / 25.6 = 1.145).

Presently, the CAPE-MA35 ratio of 1.15 forecasts a possible 10-year annualized actual return of about 6.8% to June 2032 (Determine-2). Based mostly on the present S&P 500 worth this is able to point out an finish of June 2032 worth of seven,524 for S&P-real, with higher and decrease confidence values of 8,500 and 6,640, respectively (Determine-3).

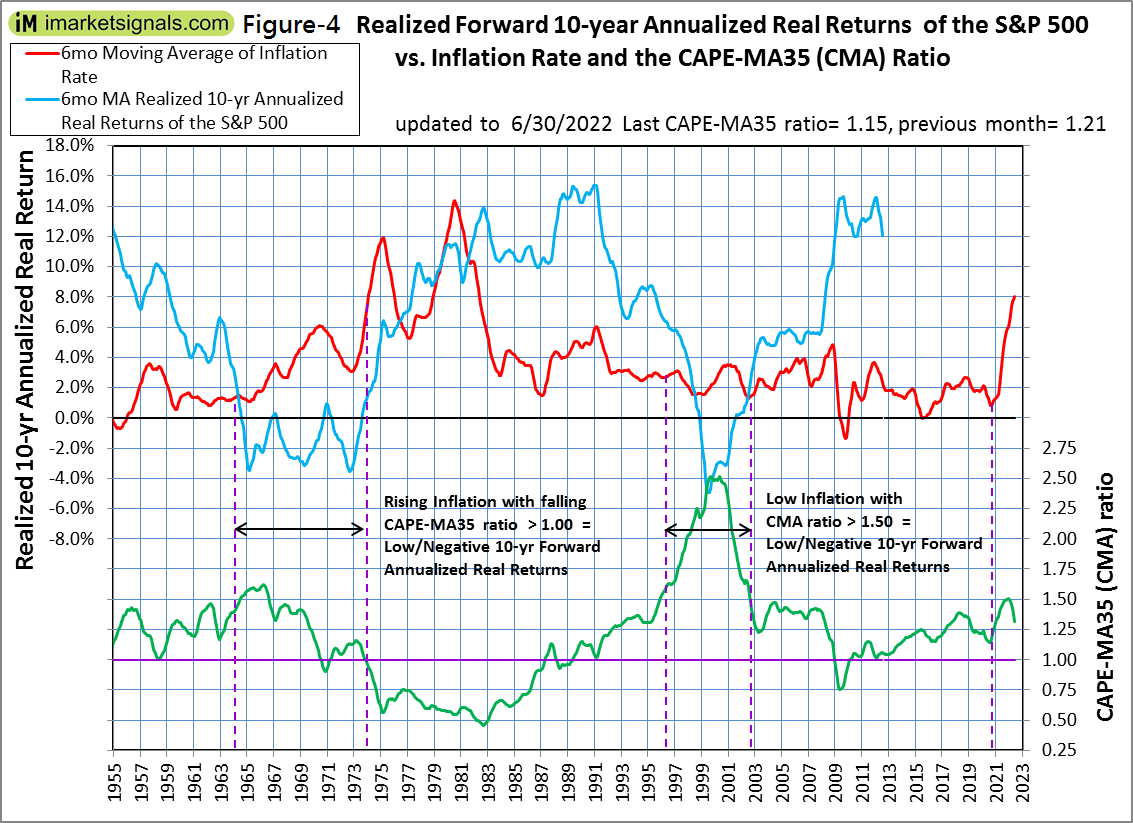

The forecast 10-year annualized actual return of about 6.8% relies on regression evaluation and could also be optimistically excessive during times of rising inflation. Determine-Four exhibits inflation, the CAPE-MA35 ratio and realized 10-year annualized actual returns from 1955 onwards. One observes that very low or unfavorable 10-year ahead annualized actual returns adopted the interval with rising inflation and a falling CAPE-MA35 ratio, 1964-1973. Present situations look like much like that point interval.

Additionally in Determine-Three the present degree of the S&P 500 relative to the long-term development is indicated by the road parallel to the long-term development line. Be aware that this relative degree is now about the identical because it was on the finish of 2007 previous to the 55% decline to the March 2009 low.

iMarketSignals iMarketSignals iMarketSignals

Forecasting Returns To 2032 With The Lengthy-Time period Pattern

When extending the most effective match line and the prediction band traces (Determine-3), then the S&P-real finish of June 2032 worth can be 4,888.

Thus, the historic development forecasts a possible complete achieve of solely about 25% (or an annualized return of two.3%) for S&P-real from its June 2022 degree of three,899 to the top of June 2032 greatest match degree of 4,888.

Conclusion

- The present elevated degree of the S&P 500 relative to the present long-term development degree warns that shares are nonetheless overvalued; and

- The present CAPE-MA35 ratio of 1.15 forecasts a comparatively excessive 6.8% actual 10-year ahead return for the S&P 500, whereas the long-term development signifies an actual 10-year ahead return of solely 2.3%.

- Nevertheless, present excessive/rising inflation and a falling CAPE-MA35 ratio might point out very low, or unfavorable 10-year ahead returns for equities, much like what adopted the interval 1964-1973.

- The present situation of overvaluation and excessive inflation suggests the potential for a serious downturn for equities. An additional decline of about 60% is feasible, ought to the S&P-real attain the decrease prediction band degree.

Updates of the estimated 10-year ahead returns of the S&P 500 (Determine-2) are posted month-to-month at imarketsignals.com.

Appendix

The perfect match line and prediction band

The perfect match line and prediction band had been calculated from month-to-month information from Jan-1871 to July-2012. The S&P-real values for the interval after July-2012 are “out of pattern” and weren’t included within the regression evaluation.

The equation of the most effective match line is y = 10(ax+b)

y = is the dependent variable of the most effective match line. x = is the variety of months from January 1871 onwards. a = 0.0023112648 b = 2.02423522

[ad_2]

Supply hyperlink