MoMo Productions

The Invesco Senior Mortgage ETF (NYSEARCA:BKLN) is an index ETF investing in senior secured variable price loans from non-investment grade firms. BKLN’s holdings are virtually all variable price loans, which see larger rate of interest funds and steady asset costs when charges rise. As such, BKLN tends to outperform different bond indexes when charges are rising, as has been the case YTD.

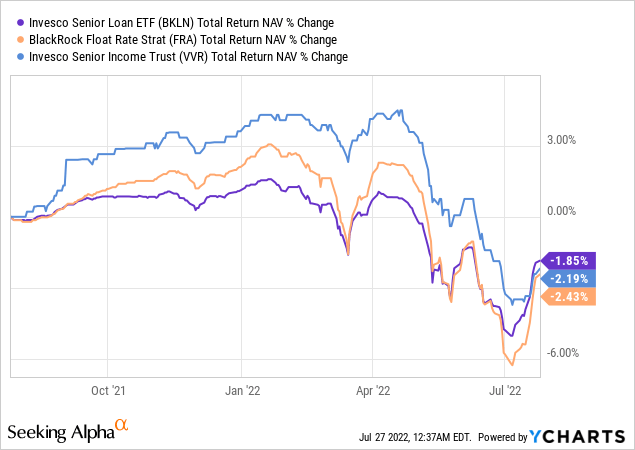

BKLN is an inexpensive funding alternative, particularly in a rising charges surroundings, however there are a number of comparable CEFs with larger yields, reductions, and general worth propositions. These embody the BlackRock Floating Charge Revenue Methods Fund (FRA) and the Invesco Senior Revenue Belief (VVR). For my part, and underneath present market circumstances, these CEFs are stronger funding alternatives in comparison with BKLN. As such, I’d not be investing in BKLN at the moment.

Variable Charge Bonds versus Mounted-Charge Bonds – Evaluation and Comparability

BKLN invests in variable price bonds, whereas most bond funds spend money on fixed-rate bonds. There are vital variations between these two sub-asset lessons, variations that are materials to the fund’s efficiency, traits, and funding thesis. As such, let’s begin with a fast comparability between these, earlier than looking on the fund itself.

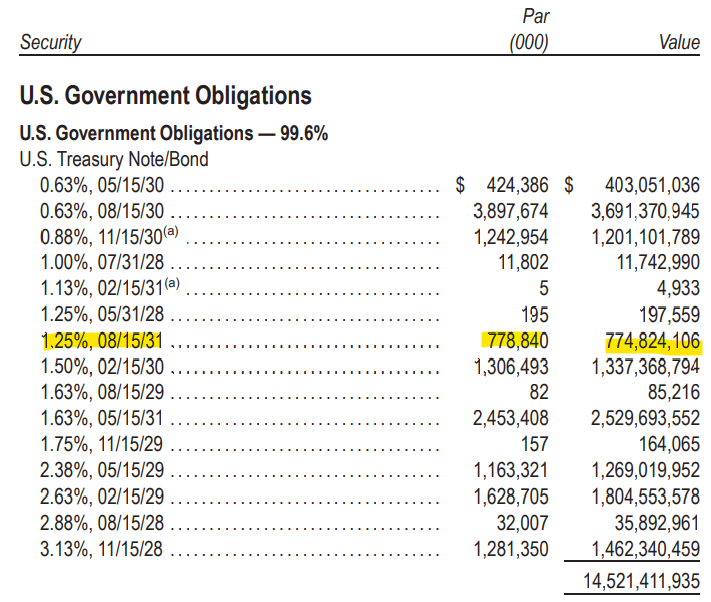

Mounted-rate bonds pay a hard and fast rate of interest fee all through their tenure. Market circumstances might change, however the rate of interest on the bonds stays the identical. Most bond funds give attention to fixed-rate bonds, as these are usually the commonest kind of bond. For instance, the iShares 7-10 12 months Treasury Bond ETF (IEF), the most important, most well-known treasury index ETF, completely invests in fixed-rate bonds / treasuries. Let’s have a fast have a look at one of many fund’s underlying bonds. The information beneath is for 3Q2021.

BKLN 2021 Annual Report

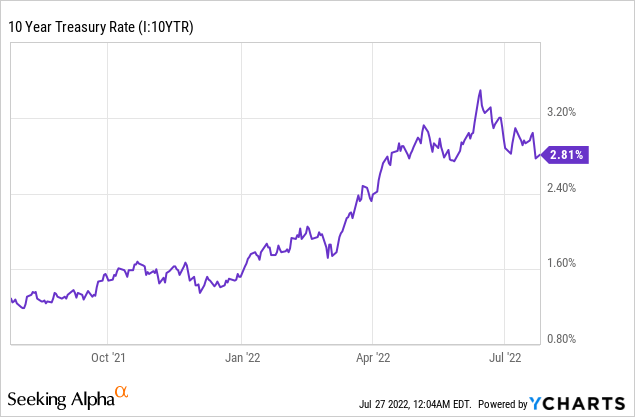

The marked bond above may be described as follows. IEF loaned $778,840,000 to the federal government at a 1.25% rate of interest with a maturity date of 8/15/31. IEF’s bond will likely be repaid in full at maturity however, if the necessity arises, the fund may promote stated bond within the open market every time it desires. The market worth of stated bond may materially differ from the unique funding, relying on financial and trade circumstances. Situations have materially modified since, as larger inflation charges and tighter financial coverage have led to elevated rates of interest throughout the boards. 10Y treasury charges, the benchmark treasury price, and the closest analogue to this particular bond, have jumped from 1.25% to 2.80% these previous few months.

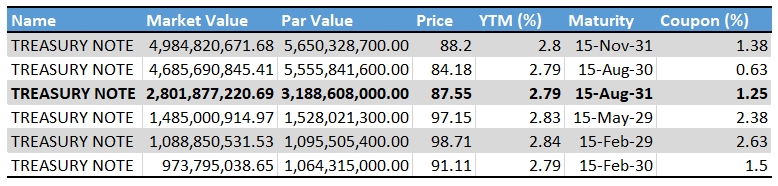

Importantly, the above is just for newly-issued treasuries. Older treasuries keep their decrease rates of interest, together with IEF’s 1.25% treasury bond. As ought to be apparent, investor demand for a 1.25% previous treasury bond goes to be fairly low when there are newer points yielding greater than twice as a lot. Low investor demand immediately results in decrease costs, with this particular bond’s worth declining by about 12%. The next desk is for 3Q2022, rates of interest have barely decreased since, however not materially so.

BKLN Company Web site – Chart by creator

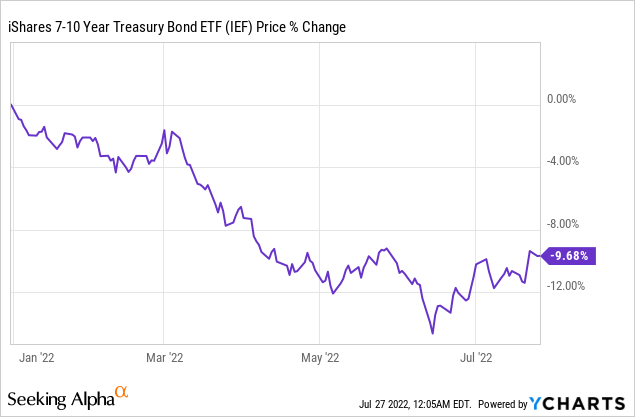

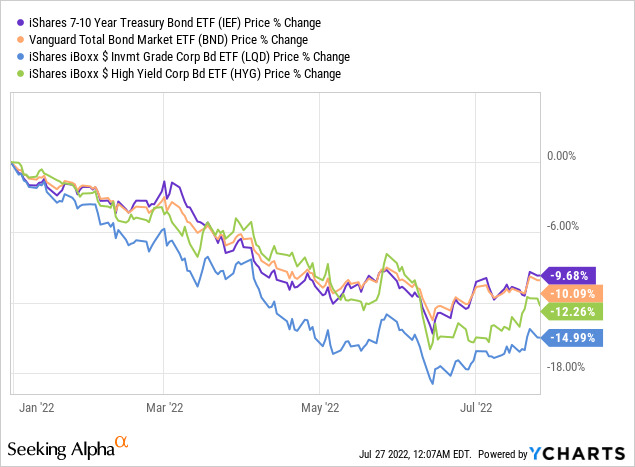

Decrease bond costs imply capital losses for IEF and its shareholders, with the fund’s worth declining by 9.7% YTD.

BKLN’s underlying holdings work considerably otherwise from the above. BKLN focuses on senior secured loans which, resulting from market conference, overwhelmingly have variable charges. When market circumstances change, the rate of interest of those bonds modifications too, which helps stabilize their worth when market circumstances are turbulent. For instance, let’s take a look at BKLN’s largest holding. Desk beneath is for 3Q2021.

BKLN Annual Report 2021

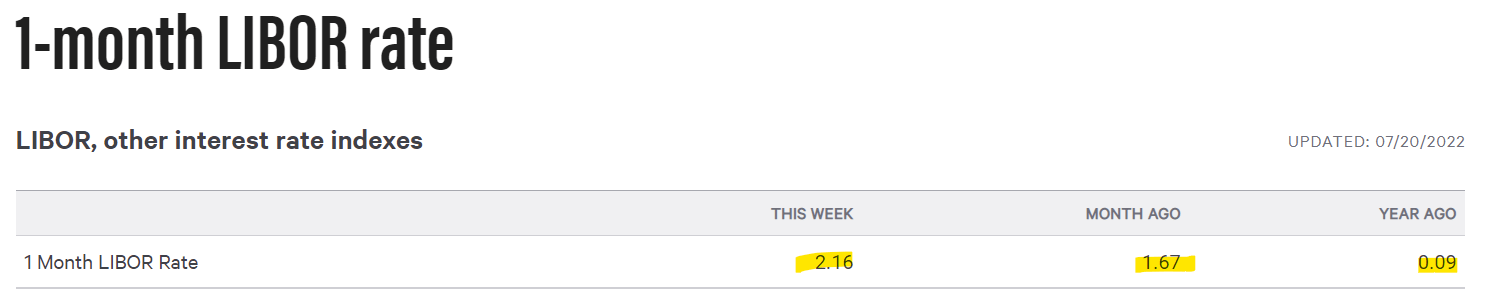

The marked bond above may be described as follows. BKLN loaned $96,712,000 to Constitution Communications (CHTR) at a price of 1.75% plus 1M Libor, with a maturity date of 02/01/2027. 1M Libor is a benchmark rate of interest which intently tracks the Federal Funds Charge, the rate of interest set by the Federal Reserve. Federal Funds Charges have been at near 0% final 12 months, 1M Libor was at 0.09%, so the bond yielded 1.84%.

With extraordinarily few exceptions, if the Federal Reserve hikes charges by X%, 1M Libor goes up by X%. 1M Libor has gone up these previous twelve months, intently monitoring Federal Reserve hikes, as anticipated.

Bankrate.com

BKLN’s bond is tied to Libor, which is tied to the Federal Reserve charges, in order charges improve so does the rate of interest paid by stated bond. As per administration knowledge, stated bond now pays an rate of interest of three.42%, a rise from one 12 months in the past, as anticipated. Greater rates of interest assist stabilize bond demand and costs. Costs for this particular bond have remained comparatively steady, as anticipated. There have been some losses, principally as a result of it takes time for Federal Reserve hikes to reverberate throughout bond markets, and since the Fed has been sluggish to hike this cycle.

BKLN is a broad-based, diversified, senior secured / variable price mortgage index ETF. The overwhelming majority of its holdings have comparable traits to the bond above, with all the advantages that entail.

As BKLN’s holdings have variable charges, these improve when rates of interest are rising, as they presently are. Greater rates of interest means larger revenue for the fund, and better dividends for shareholders, a major profit for a similar. As proven within the instance above, BKLN’s bonds have seen their rates of interest improve these previous few months, as anticipated.

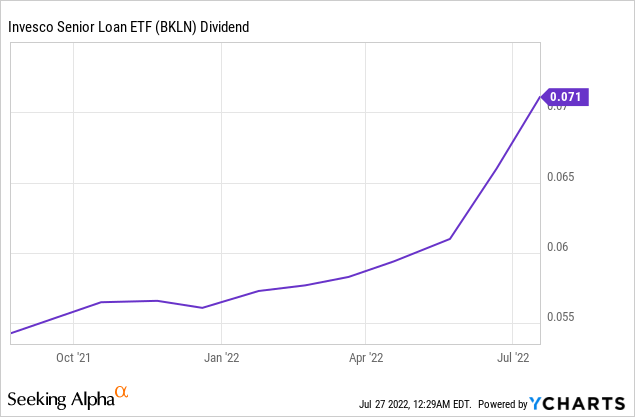

On a extra adverse observe, it takes some time for larger bond rate of interest funds to translate into larger dividend funds. BKLN’s dividends have elevated from $0.0541 to $0.0660 previously twelve months, for a 22% improve. Dividends have elevated, however rate of interest hikes have been considerably better than this. Attributable to this, the fund yields a comparatively low 3.3%. On a extra constructive observe, which means dividends ought to proceed to extend within the coming months, benefitting traders.

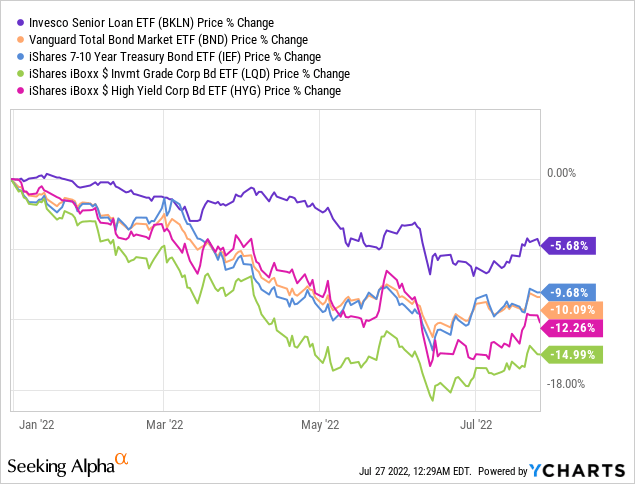

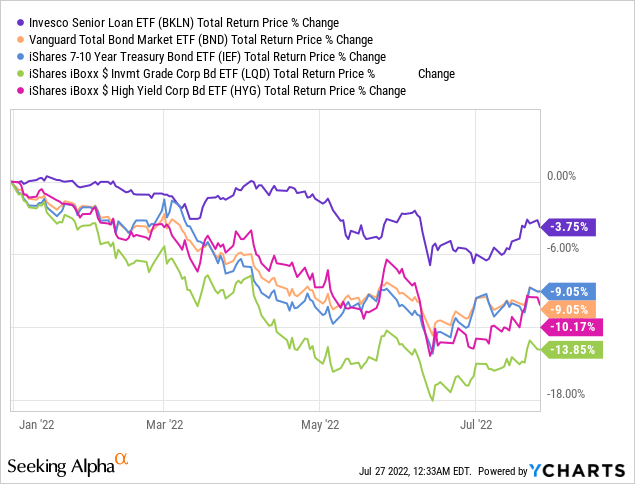

BKLN sees larger revenue and extra steady share costs when rates of interest rise, so the fund ought to outperform its friends when this occurs. This has been the case YTD, as anticipated.

BKLN outperforms when rates of interest are rising, as they presently are. The fund’s funding thesis is straightforward, clear, and powerful, for my part not less than. Though there’s nothing inherently mistaken with the fund, there are a number of stronger selections on the market. Let’s take a look.

Fast Peer Comparability

BKLN is the most important, hottest senior mortgage ETF available in the market at present, however it has many friends. There are a number of ETFs with comparable holdings and traits, together with the SPDR Blackstone Senior Mortgage ETF (SRLN) and the First Belief Senior Mortgage Fund (FTSL). There are additionally a number of senior mortgage CEFs, together with FRA and VVR.

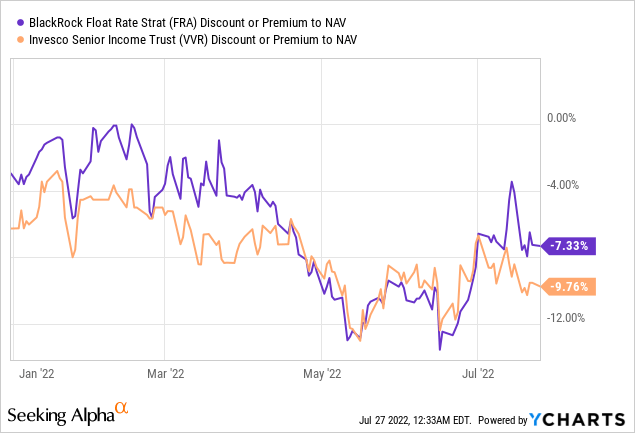

CEFs particularly are trying extraordinarily enticing underneath present market circumstances. Latest losses and weakening financial fundamentals have prompted CEF reductions to widen, with these three CEFs buying and selling with giant double-digit reductions to NAV.

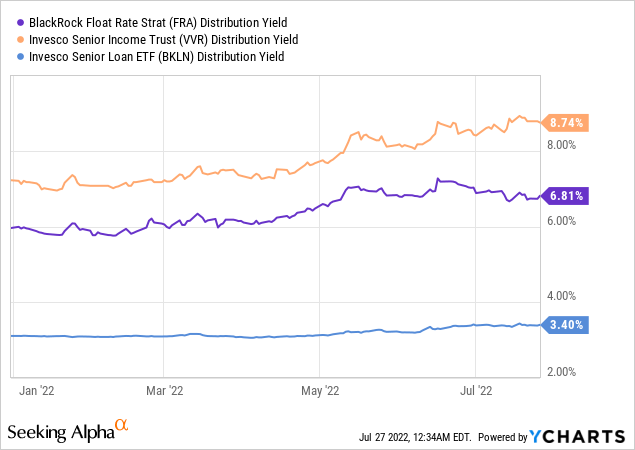

Greater distribution yields imply stronger long-term whole shareholder returns, on each a NAV and worth foundation.

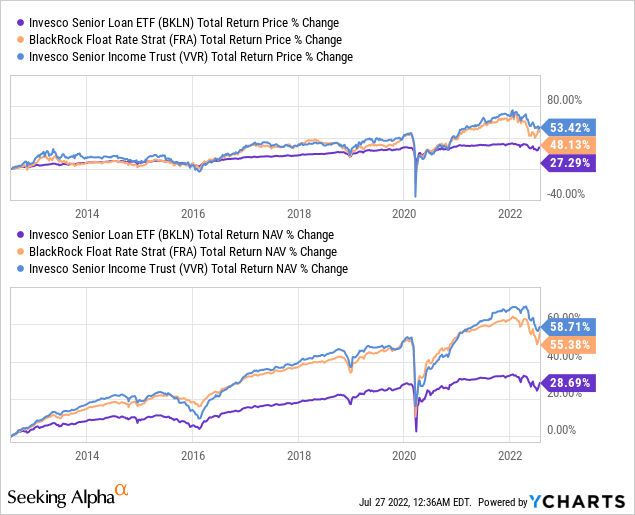

FRA and VVR have larger distribution yields, whole shareholder returns, and reductions to NAV, relative to BKLN. Beneath these circumstances, I see no cause to spend money on BKLN over these two CEFs.

Conclusion

BKLN is an index ETF investing in senior secured variable price loans from non-investment grade firms. BKLN outperforms throughout a rising charges surroundings, making the fund an inexpensive funding alternative underneath present market circumstances. Though there’s nothing inherently mistaken with the fund, there are a number of comparable CEFs with larger yields, reductions, and general worth propositions. As such, I’d not be investing in BKLN at the moment.

{kind=link}