[ad_1]

utah778

Transcript

We expect the Nice Moderation, an period of regular progress and inflation, is over.

We see ourselves in a brand new regime of elevated macro volatility and better danger premia.

Three key themes information us on this new setting.

1) Bracing for volatility

Macro volatility drives market volatility, so the tip of the Nice Moderation is now inflicting fierce market gyrations. In a extra risky setting, buyers will demand greater compensation for holding each shares and bonds.

2) Residing with inflation

Proper now, we predict the Fed has boxed itself into responding to political pressures or relatively the politics of inflation. This means recession dangers.

Finally, the harm to progress and jobs from combating inflation will change into apparent and central banks will reside with greater inflation.

3) Positioning for net-zero

The bumpy transition to net-zero emissions additionally fuels the brand new regime’s volatility. We like “already inexperienced” corporations and carbon-intensive ones with credible transition plans or people who provide vital supplies for the transition.

We expect buyers should be nimble on all funding horizons.

Within the brief time period, we’ve reduce most Developed Market equities, as central banks seem set to overtighten coverage. In the meantime, we improve credit score given their leap in yields.

Strategically, we nonetheless favor equities over bonds in the long term as yields rise and inflation traits greater.

____________

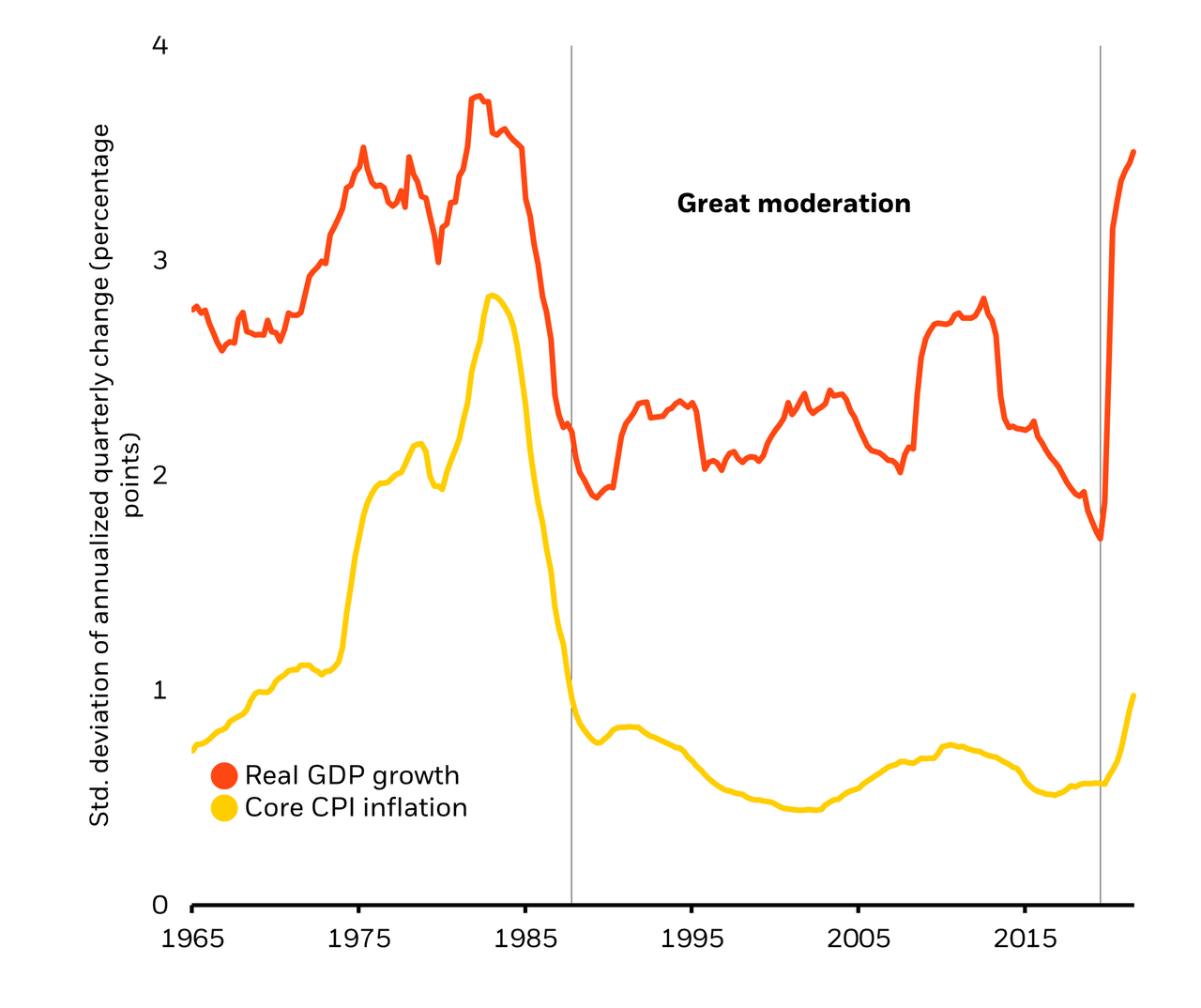

The tip of the Nice Moderation

Volatility Of US GDP Progress And Core Inflation (BlackRock Funding Institute, U.S. Bureau of Financial Evaluation and Labor Division, with information from Haver Analytics, March 2022)

Notes: The chart exhibits the usual deviation of the annualized quarterly change of U.S. actual GDP and the core Shopper Worth Index.

What occurred to the Nice Moderation anyway? It acquired flipped the wrong way up. Key options of the period had been steadily increasing manufacturing capability and demand shocks. Central banks might simply nudge spending by reducing or mountain climbing charges. However now that’s flipped (see chart above). Why? Manufacturing constraints. The pandemic triggered an enormous sectoral shift in spending from companies to items in addition to labor shortages. The restart and struggle in Ukraine added an power crunch. These are powerful issues to resolve. A pile-up of world debt to buffer the Covid shock limits the wiggle room of central banks – and makes it extra tempting to reside with inflation. And the politicization of every little thing means coverage debates are oversimplified when nuanced options are wanted. All this makes trade-offs between progress and inflation tougher, we imagine, and results in worse outcomes.

Three funding themes information us in new period

Three funding themes information us within the new period. First – Bracing for volatility. Macro volatility drives market volatility. The tip of the Nice Moderation is now inflicting fierce market gyrations. On this structurally extra risky setting, buyers will demand greater danger premia, or compensation for holding each shares and bonds. What do we predict this implies? Each tactical and strategic allocations need to adapt extra rapidly. Portfolios need to get extra granular on the sector degree. Conventional 60/40 stock-bond portfolios and fashions received’t work as effectively anymore. And “shopping for the dip” is unlikely to be as efficient because it was earlier than. The inertia behind these form of behavioral biases should be overcome, we imagine.

Our second theme is as related as ever – Residing with inflation. Proper now, we predict the Fed has boxed itself in by responding to political pressures to rein in inflation. In different phrases, the politics of inflation rule. This means draw back dangers to progress and firm earnings. Finally, the harm to progress and jobs from combating inflation will change into apparent, in our view, and central banks will reside with greater inflation. Manufacturing constraints rooted within the pandemic and exacerbated by the struggle in Ukraine have led to 40-year highs in inflation. The spike in commodities is a main instance of how these elements have collided into an inflation explosion. And we see an period of structurally greater commodities costs forward.

The bumpy transition to net-zero emissions additionally fuels the brand new regime’s volatility. This makes for our third theme – Positioning for net-zero. We imagine markets haven’t absolutely priced in fast-changing societal preferences for sustainability and technological innovation. We like “already inexperienced” corporations and carbon-intensive ones with credible transition plans.

What this implies for investments

Extra frequent tactical adjustments – like recognizing a turning level for shares when markets eye a dovish pivot by central banks. Within the brief time period, we’ve reduce DM equities besides Japanese shares as central banks seem set to overtighten coverage. We improve credit score to obese as a part of an up-in-quality adjustment to portfolios. We nonetheless like inflation-linked bonds, and now favor the euro space. And we like UK gilts as we see the Financial institution of England turning dovish.

Strategically, we imagine our stance is positioned for the brand new regime. We favor equities over bonds in the long term as yields rise and inflation traits greater. We expect central banks will reside with greater inflation, pause after which change course on their fee rises – a boon for shares. Personal markets should not immune on this new regime of upper volatility, however alternatives exist for selective buyers, particularly in non-public credit score. See our full Midyear outlook for the granular adjustments to our asset views.

Market backdrop

Final week’s U.S. jobs replace underscores the continuing provide shock that can trigger greater inflation to be extra persistent. Non-farm payrolls had been a little bit greater than anticipated, permitting for downward revisions in earlier months. However the participation fee – capturing these in or searching for work – fell on the month. Bond yields resumed their rise as markets priced in greater possibilities that the Fed will increase charges by 75 foundation factors at its coverage assembly later this month.

U.S. CPI can be key this week. A continuation of the sample of persistently excessive month-to-month inflation charges would probably cement the case for a 75-basis level Fed hike later this month. We see the Fed persevering with with hikes as much as restrictive ranges by the tip of the 12 months. In China, second-quarter GDP will assist gauge the financial influence of strict Covid lockdowns earlier this 12 months.

[ad_2]

Supply hyperlink