[ad_1]

Greater funding prices and elevated credit score losses are more likely to mood stronger lending revenues at European banks in 2023, based on analysts.

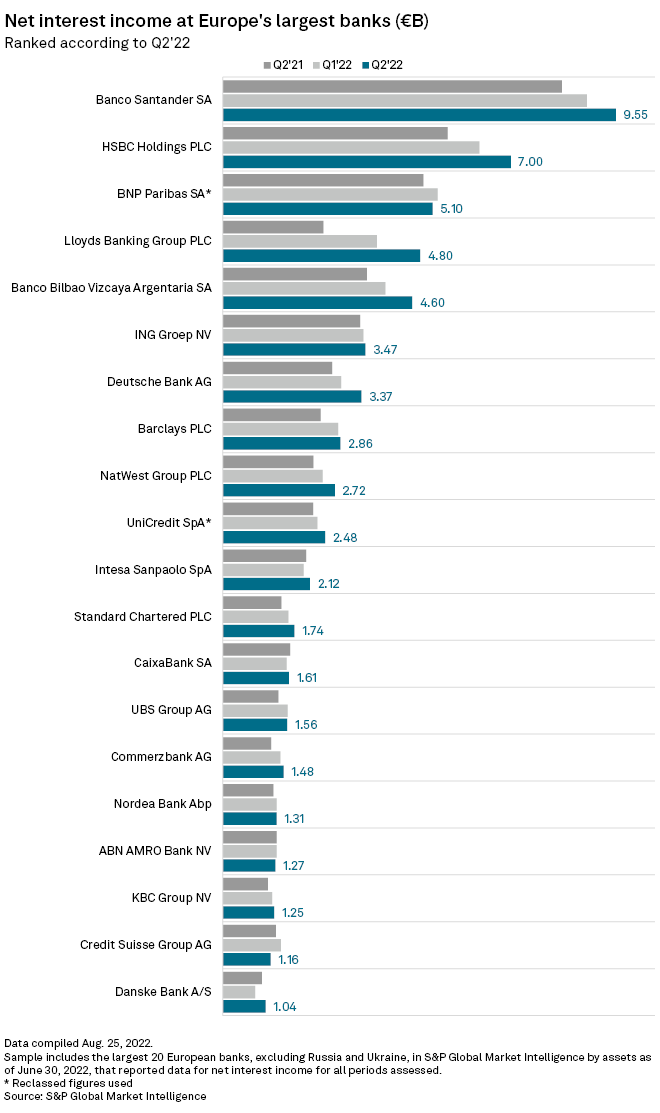

The continent’s largest lenders have loved stronger internet curiosity revenue — income from loans minus the curiosity paid on deposits — after central banks started elevating rates of interest to curb inflation. In a pattern of 20 banks, 17 reported year-over-year development within the second quarter, S&P International Market Intelligence knowledge confirmed. British lender Lloyds Banking Group PLC booked the sharpest enhance, with NII practically doubling yr over yr.

Internet curiosity incomes are more likely to proceed to rise versus prior years, with lending volumes recovering to pre-pandemic ranges, Martin Rauchenwald, a associate at London-based specialist non-public fairness investor Monetary Providers Capital, informed S&P International Market Intelligence.

Margins on lending are set to develop by between 20% and 35% on common over the subsequent three years, assuming expectations round GDP development and financial coverage are met, Emiliano Carchen, principal within the monetary providers apply at consultancy Oliver Wyman, informed S&P International Market Intelligence. There will probably be a small influence on 2022 margins and a much bigger influence in 2023, he mentioned.

Banco Santander SA recorded essentially the most internet curiosity revenue within the second quarter, with outgoing CEO José Antonio Álvarez beforehand saying higher charges would offer a “massive, important uplift.” Spanish and Italian banks are particularly well-positioned to learn from rising charges, Berenberg analyst Michael Christodoulou mentioned in an Aug. 15 analysis word. Berenberg sees a selected upside for banks geared to learn from rising charges, similar to Spain’s CaixaBank SA.

Moreover in areas the place central financial institution charges are rising, banks haven’t been passing on charges to depositors as rapidly as beforehand anticipated, Christodoulou wrote.

Double-edged sword

Financial coverage tightening may also result in greater wholesale funding prices for banks, nevertheless, pushed by a hike within the risk-free fee and widening credit score and authorities spreads, Oliver Wyman companions Elie Farah, Matthew Austen and Carchen wrote in a current dialogue paper. Banks may also count on decrease price revenue within the subsequent few years. Banks’ totally different enterprise fashions, and their various publicity to the opposing dynamics of mortgage repricing and wholesale or deposit funding, in addition to the construction of their stability sheets and geographic presence, will decide the upside on their internet curiosity margins, Carchen mentioned.

Greater charges additionally restrict mortgage demand and will result in greater mortgage losses, analysts at Deutsche Financial institution Analysis warned in a July 26 word.

The prices of threat are already starting to rise, and this can seemingly proceed, with many of the influence set to be seen in 2023, based on Monetary Providers Capital’s Rauchenwald.

“Though financial sentiment has turned damaging, it’s going to take time for the true financial influence to feed by way of to mortgage loss provisions,” Rauchenwald mentioned.

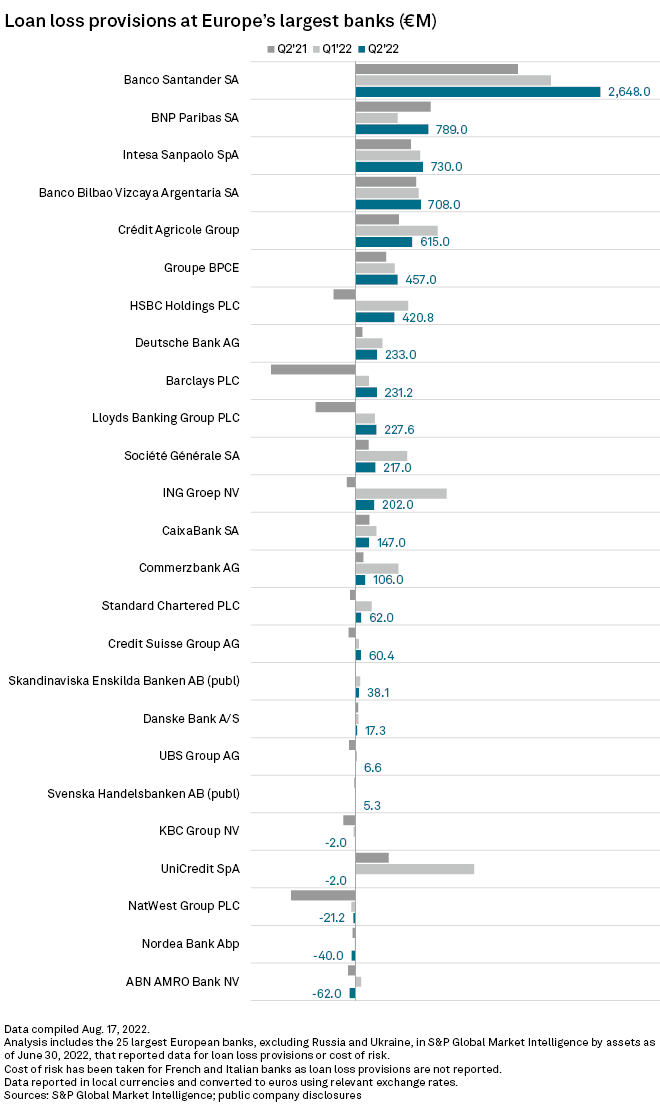

Twenty of the banks in S&P International Market Intelligence’s pattern reported greater mortgage loss provisions within the second quarter or incurred costs versus year-ago writebacks. Santander, together with recording the best NII, additionally acknowledged essentially the most provisions at €2.64 billion, up from €1.78 billion.

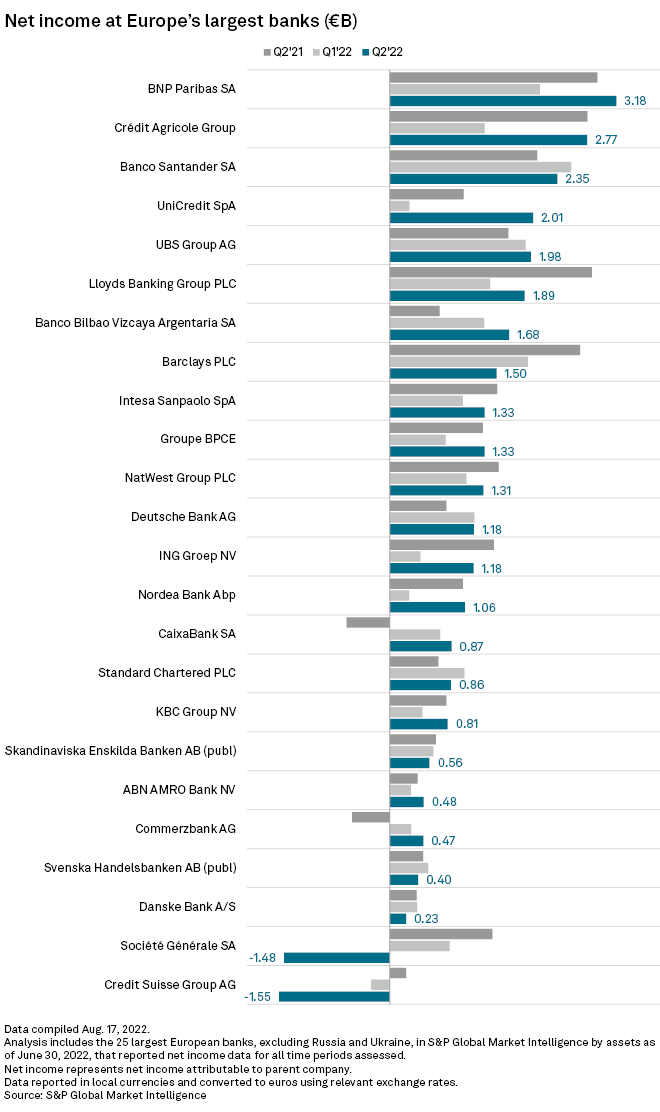

Nonetheless, banks largely gained a revenue enhance within the second quarter, with their NII offsetting elevated prices and mortgage losses, Berenberg’s Christodoulou mentioned. 13 of the 25 banks in Market Intelligence’s pattern reported both year-over-year internet revenue development or swung to income from year-ago losses within the second quarter.

Solely Credit score Suisse and Société Générale SA posted losses within the quarter, with the previous affected by its troubled funding financial institution and the latter taking in costs associated to its exit from Russia.

Report inflation

Inflation throughout Europe has risen because the starting of 2022, and banks are notably weak. Eurozone inflation is at a report excessive, hitting 8.9% in July. Within the U.Ok., inflation was 10.1% in the identical month, the highest in additional than 40 years.

In response, the European Central Financial institution in July raised charges, to zero, for the first time in over 11 years, with one other hike anticipated in September. The Financial institution of England additionally elevated its benchmark fee to 1.75% in early August.

European banks’ capital ranges are resilient and higher ready for a downturn, based on Rauchenwald.

“Future winners will probably be these that may optimize their asset technique across the rising financial setting, with a larger give attention to underwriting and phase choice,” he mentioned.

Banks in Russia and Ukraine, the place authorities possession means they’re topic to totally different market dynamics than these in Western Europe, had been excluded from this evaluation.

[ad_2]

Supply hyperlink