[ad_1]

By no means wager on the tip of the world as a result of it solely occurs as soon as. – Artwork Cashin

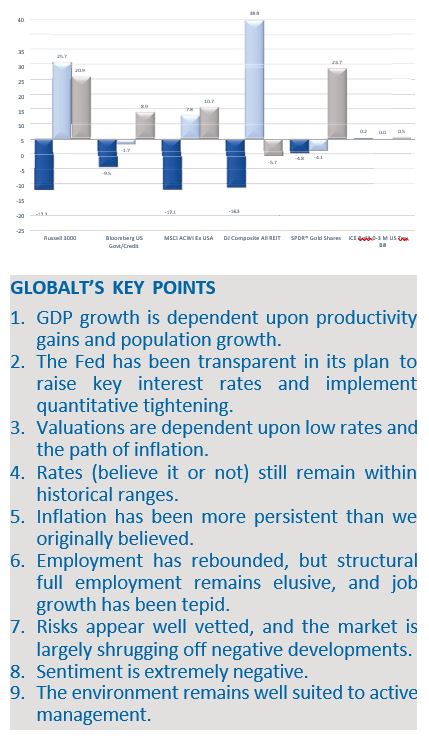

Markets have digested an excessive amount of unhealthy information to date in 2022. The efficiency of the corresponding indexes displays fairly a little bit of pessimism (see yr to this point returns by means of July 20th for a few of the main asset courses within the chart to the correct). We all know inflation has been much less transitory than consensus anticipated. The greenback has been sturdy, making use of strain to a world awash in dollar-denominated debt. Ten- yr yields have gone from close to zero in 2020 to ranges not seen since 2018, pressuring equities and progress shares particularly. The impacts of COVID are nonetheless disrupting provide chains and the employment setting worldwide. The battle in Ukraine has despatched costs for crude and pure fuel hovering. Lastly, oil spikes, inverted yield curves and Fed tightening have all preceded recessions, and in 2022, we’ve got all three concurrently. Sentiment displays the affect of an ostensibly dire setting, however we proceed to advocate wanting past the upcoming realities of the present setting to what might lie forward.

Markets have digested an excessive amount of unhealthy information to date in 2022. The efficiency of the corresponding indexes displays fairly a little bit of pessimism (see yr to this point returns by means of July 20th for a few of the main asset courses within the chart to the correct). We all know inflation has been much less transitory than consensus anticipated. The greenback has been sturdy, making use of strain to a world awash in dollar-denominated debt. Ten- yr yields have gone from close to zero in 2020 to ranges not seen since 2018, pressuring equities and progress shares particularly. The impacts of COVID are nonetheless disrupting provide chains and the employment setting worldwide. The battle in Ukraine has despatched costs for crude and pure fuel hovering. Lastly, oil spikes, inverted yield curves and Fed tightening have all preceded recessions, and in 2022, we’ve got all three concurrently. Sentiment displays the affect of an ostensibly dire setting, however we proceed to advocate wanting past the upcoming realities of the present setting to what might lie forward.

In our estimation, inflation remains to be transitory however clearly this is dependent upon your time-frame. The Fed has been making an attempt since 2009 to get GDP rising meaningfully and inflation to ≈2% however it was achieved as an alternative by unprecedented stimulus and a world pandemic. Sadly, this drove extra spending right into a provide constrained setting. The worldwide tightening (rising lengthy and quick charges and better oil costs) that has been occurring for the final couple of years is beginning to take a chunk out of the financial system on the identical time the Fed is aggressively defending in opposition to inflation. It’s a not-so-delicate waltz between stoking financial progress and protecting inflation at bay which has develop into more and more frenetic.

Measures of inflation, particularly the most well liked contributors to the Client Value Index (CPI), are lagging measurements. Simply as we “felt” inflation earlier than it really confirmed up in inflation information, we appear to be feeling an easing in sure prices. Of late a number of retailers have reported extra stock and have needed to unload items at decrease costs. We all know dwelling gross sales usually (varies by area) are reporting slower single household begins and mortgage purposes. Costs on the pump have moderated some and commodities are effectively off their highs from six months in the past. Shoppers have been buying and selling to extra non-public label merchandise, meat consumption is weaker, and fuel consumption is seasonally at its lowest in a decade. Lastly, we’ve seen a spike in revolving credit score suggesting customers could also be quick on their budgets. This have to be thought of in mild of the proliferation of pay-as-you-go plans from the likes of Klarna and Affirm. This “debt” doesn’t present up as a debit on the buyer’s steadiness sheet and is simply generally reported to the credit score companies within the occasion of delinquency. AT&T just lately reported elevated delinquencies from customers in what’s arguably their least inelastic fungible expense. Wage inflation is a strain level within the inflationary panorama, and we welcome any trace that the labor pool might be increasing. Merely put, extra People reentering the workforce ought to alleviate wage pressures in a constructive means. On the extra adverse aspect, nonetheless, we’ve got seen rising bulletins of removing of job openings, hiring freezes and layoffs.

Content material continues under commercial

What was most perplexing concerning the shopper is how they managed to transition from receiving direct authorities stimulus to receiving nothing in any respect with seemingly little change in conduct. What we found is that many had amassed appreciable money financial savings which appears to have allowed them to stay out of the out there workforce longer than anticipated. Because of this, unemployment stays fairly low, wage strain persists, and provide chains stay disjointed. Nonetheless, recently we’ve got seen an uptick in a number of measures which will point out the setting could also be altering. Jobless claims have been rising steadily since April. Actually, since 1980, jobless claims have by no means elevated as a lot as they’ve over the newest four-month interval with out the US financial system being already in recession or coming into one quickly thereafter. Markit US flash manufacturing PMI was down 0.Four factors to 52.3, the bottom print in two years. Output fell under 50 for first time since June ’20, with charge of value inflation at its softest degree since Apr ‘21, and promoting worth will increase had been the slowest since Feb ‘21. Flash Providers PMI dropped under the all-important 50 degree to 47.5, the bottom studying since Might ‘20. Employment nonetheless rose, although at its slowest tempo in 5 months. Whereas nothing is well confirmed by a sampling of financial collection, just lately reported information appears to be furthering each peak-inflation and peak-Fed narratives.

There’s an outdated saying we imagine rings true most of the time: “The bond market tells the reality and fairness markets lie.” This has extra to do with the bond market being extra ahead wanting whereas equities usually mirror present realities. The bond market seems to be reiterating these “peak” narratives. Measures of the unfold between actual yields and the yields on treasuries of comparable tenor suggest traders imagine inflation on a 5 yr or longer horizon is comparatively benign and consistent with the Feds objectives at ≈2%. An inverted yield curve alerts the Fed will at the least need to take its foot off the brakes in an effort to keep away from mountaineering the financial system into recession.

We posit that the Fed doesn’t affect the trail of charges however really follows it. The Fed has achieved a lot of the specified tightening simply by talking of it. The Fed might discover itself able to pause sooner or later this yr. As quickly as traders begin to assume the Fed could also be much less aggressive, charges are more likely to ease and relieve draw back strain considerably. An aggressive charge trajectory in a weakening financial system may be very damaging to nearly all the pieces. If they start to ease tightening expectations alongside inflation that’s increased however tolerable and quick lived (6-Eight months), they might obtain the “tender touchdown” all of us dream of.

The unhealthy information seems to be effectively understood. Final week each the CPI and PPI stories shocked traders anticipating, at a minimal, a pause in inflation’s advance. The fairness market as measured by the S&P 500 reacted negatively initially however recovered and surpassed starting ranges inside every week. Measurements of sentiment are on steadiness very bearish. In talking with shoppers and witnessing their conduct first-hand, we discover most traders are jittery at greatest. Even skilled cash managers are rattled. The BofA chart above depicts the Financial institution of America International Fund Supervisor Survey which included 259 individuals with $722 billion underneath administration within the week by means of July 15. They highlighted their largest issues as (within the following order) excessive inflation, adopted by a world recession, hawkish central banks, and systemic credit score occasions. At the very least in keeping with these measures, sentiment has by no means been this unhealthy.

Very like the overly bullish setting wherein we ended 2021, we really feel issues are so excessive that the dangers are doubtlessly to the upside. With sentiment so adverse, it might take little in the way in which of “much less unhealthy” information to offer some life to severely broken markets. The sell-off has been broad when it comes to asset class, sector, and business with scant alternative to cover. We sense that traders are wracked with worry. We’re coming into a seasonally sanguine interval, inflation and charges could also be peaking, the Fed might have achieved sufficient tightening to at the least pause, valuations have compressed meaningfully, particularly given the sturdiness of company earnings, and we’ve got but to see the type of blow off high or capitulation usually related to the tip to bull markets. All of that is to say, the setup by means of the tip of this yr might set off a broad-based rally in meaningfully depressed asset courses – which is nearly all the pieces.

Our outlook continues to be dominated by our weight of the proof strategy using basic, technical, and quantitative disciplines. The important thing components of this course of are pushed broadly by expectations for inflation, rates of interest and foreign money. We develop a story for the way issues might play out however look forward to the items to fall in to position earlier than appearing. We imagine timing is vital. Now we have been comparatively inactive as a result of markets, charges, and commodities appears directionless regardless of elevated volatility. We require affirmation earlier than dedication. Generally the toughest factor to do is to stay affected person.

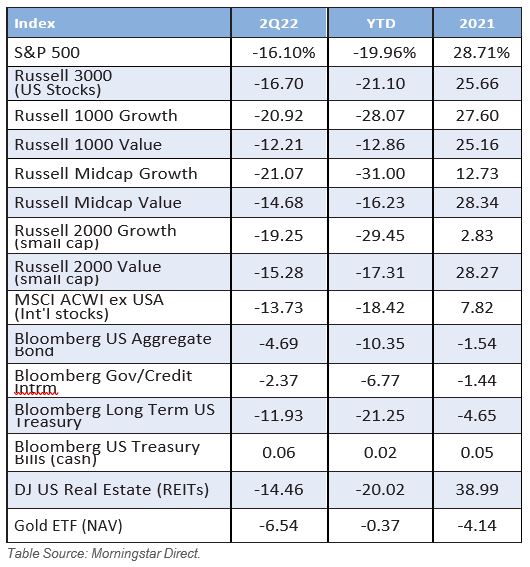

America fairness market, as broadly measured by the Russell 3000 Index, declined -16.70% within the second quarter of the yr. No sector posted constructive returns over the quarter. Rising oil and meals costs compelled customers to make tough choices, transferring away from elective gadgets to main family items. That is evident within the dispersion between greatest and worst performing sectors, Client Staples down solely (-4.04%) and Client Discretionary down (-25.51%) over the interval, as measured by the S&P Choose Providers Index household. At first of the yr, Russia/Ukraine tensions despatched oil costs skyrocketing resulting in overbought situations. In latest weeks we’ve seen a pullback in commodity costs leading to a decline within the vitality sector, the second top-performer over the quarter (-5.26%). Adverse financial surprises continued to weigh available on the market over the quarter and traders appeared to brace themselves for impending recession, rotating in direction of extra defensive sectors and away from progress themes with Well being Care and Utilities down solely (-5.91%) and (-5.09%) respectively and Communication Providers and Know-how down (-20.88%) and (-19.67%) respectively. As talked about beforehand, the remaining sectors additionally posted adverse returns over the interval, Actual Property (-14.72%), Industrials (-14.78%), Supplies (-15.90%) and Financials (-17.50%). Progress was the clear loser throughout all market caps, because it continued to underperform its worth counterparts as measured by the Russell indices. The best dispersion between model class was seen in Giant Cap, the place Russell 1000 Progress declined -20.92% and Russell 1000 Worth was down -12.21%. With that stated, Russell Giant Cap Worth was the most effective performer of the quarter, adopted by Russell Mid Cap Worth (-14.68%), Russell 2000 Worth (-15.28%), and Russell 2000 Progress (-19.25%). Russell Mid Cap Progress led to the draw back, declining (-21.07%) over the quarter. Worldwide markets outperformed in Q2, with the MSCI All Nation World Index ex USA down (-13.73%) in comparison with the S&P 500 which was down (-16.10%).

America fairness market, as broadly measured by the Russell 3000 Index, declined -16.70% within the second quarter of the yr. No sector posted constructive returns over the quarter. Rising oil and meals costs compelled customers to make tough choices, transferring away from elective gadgets to main family items. That is evident within the dispersion between greatest and worst performing sectors, Client Staples down solely (-4.04%) and Client Discretionary down (-25.51%) over the interval, as measured by the S&P Choose Providers Index household. At first of the yr, Russia/Ukraine tensions despatched oil costs skyrocketing resulting in overbought situations. In latest weeks we’ve seen a pullback in commodity costs leading to a decline within the vitality sector, the second top-performer over the quarter (-5.26%). Adverse financial surprises continued to weigh available on the market over the quarter and traders appeared to brace themselves for impending recession, rotating in direction of extra defensive sectors and away from progress themes with Well being Care and Utilities down solely (-5.91%) and (-5.09%) respectively and Communication Providers and Know-how down (-20.88%) and (-19.67%) respectively. As talked about beforehand, the remaining sectors additionally posted adverse returns over the interval, Actual Property (-14.72%), Industrials (-14.78%), Supplies (-15.90%) and Financials (-17.50%). Progress was the clear loser throughout all market caps, because it continued to underperform its worth counterparts as measured by the Russell indices. The best dispersion between model class was seen in Giant Cap, the place Russell 1000 Progress declined -20.92% and Russell 1000 Worth was down -12.21%. With that stated, Russell Giant Cap Worth was the most effective performer of the quarter, adopted by Russell Mid Cap Worth (-14.68%), Russell 2000 Worth (-15.28%), and Russell 2000 Progress (-19.25%). Russell Mid Cap Progress led to the draw back, declining (-21.07%) over the quarter. Worldwide markets outperformed in Q2, with the MSCI All Nation World Index ex USA down (-13.73%) in comparison with the S&P 500 which was down (-16.10%).

Analysts and corporations have develop into extra pessimistic of their earnings outlooks and revisions, consequently earnings estimates are decrease immediately than originally of the quarter. Moreover, 102 firms in S&P 500 have issued EPS steerage. Of those firms, 71 have issued adverse EPS steerage – the best quantity since This fall 2019. The second quarter earnings progress charge for the S&P 500 is estimated to be 4.3%. If that is the precise progress charge, it might mark the bottom earnings progress charge since This fall 2020. Nonetheless, as firms usually tend to report constructive surprises, the precise earnings progress charge has exceeded the estimated earnings progress charge in 39 of the previous 40 quarters for the S&P 500. To date, 21% of S&P 500 firms have reported earnings for the second quarter. Of those firms, 68% have beat on EPS and 26% have reported precise EPS under imply estimate. Out of the businesses to report thus far, labor value and shortages have been cited as main headwinds affecting earnings and revenues for Q2 and future quarters. We glance to firm commentary for perception into the affect of ongoing basic issues.

GLOBALT is an SEC Registered Funding Adviser since 1991 and, efficient July 10, 2013, stays a Registered Funding Adviser by means of a individually identifiable division of Synovus Belief N.A., a nationally chartered belief firm. GLOBALT supplies skilled cash administration to each institutional and particular person traders by means of Fairness, Mounted Revenue, and ETF Asset Allocation methods. Registration of an Funding Adviser doesn’t suggest any sure degree of ability or coaching.

Valuations on this report are based mostly on data offered by third celebration sources. Though the information gathered from third-party sources is believed to be dependable, GLOBALT Investments has not audited or verified the accuracy or completeness of the data. GLOBALT will not be accountable for any damages or losses arising from any use of third- celebration information. Any safety, allocation, or weightings described herein are topic to alter with out discover and no assurances are made that they may stay in a method or portfolio on the time you obtain this data. Illustrative methods or portfolios proven will not be consultant of methods or portfolios of current shoppers. Efficiency numbers proven are topic to alter with out discover. If there are any questions concerning this report, please contact your Advisor or GLOBALT for help.

The efficiency information introduced represents previous efficiency, which don’t assure future efficiency and future efficiency might end in a loss. No present or potential shopper ought to assume that the longer term efficiency of any particular funding, funding technique (together with the investments and/or funding methods beneficial/supplied by the Adviser or GLOBALT) or product referenced shall be worthwhile or equal to previous efficiency ranges. The funding return and principal worth of an funding will fluctuate, thus when offered or redeemed, could also be price kind of than the unique value. There are dangers, together with doable lack of principal, related to investing in securities, together with however not restricted to erratic or unstable market situations, monetary and debt market danger, geopolitical danger, administration danger, liquidity, non-diversification danger, credit score and counterparty danger. Diversification and/or strategic asset allocation don’t assure a revenue nor shield in opposition to a loss in declining markets. Buyers ought to rigorously think about funding targets, dangers, expenses and bills. Shoppers are suggested that their statements and particular person commerce confirmations, not this report, are the official data of their accounts and transactions. This and different vital data are contained in GLOBALT’s Type ADV Half 2 and Half 3, which is offered by your Advisor and ought to be learn rigorously previous to investing. Report calculations and figures shouldn’t be relied upon for tax functions. The data herein will not be an alternative choice to skilled tax recommendation. It’s best to seek the advice of your tax advisor for particular questions concerning your individual tax state of affairs.

Indexes are unmanaged and it’s not doable to take a position instantly in an index. Index returns proven don’t symbolize the outcomes of precise buying and selling of investor property. Index returns don’t mirror funds of any gross sales expenses, charges, or bills that an investor would pay or incur to buy or personal the securities that indices symbolize. The imposition of such charges, expenses or bills would trigger precise and back-tested efficiency to be decrease than the efficiency proven for that index. Publicity to an asset class represented by an index could also be out there by means of investable devices based mostly on that index. There is no such thing as a assurance such funding merchandise will precisely monitor index efficiency or present constructive funding returns.

GLOBALT claims compliance with the International Funding Efficiency Requirements (GIPS®).

GLOBALT has ready this materials for informational functions solely. It shouldn’t be construed as funding recommendation, a advice or solicitation to buy and / or promote any safety.

Content material will not be reproduced, distributed, or transmitted in entire or partially, by any means with out written permission from GLOBALT. To obtain permission or acquire a replica of GLOBALT’s Type ADV Half 2 and Half 3, contact GLOBALT’s Chief Compliance Officer, 3400 Overton Park Drive, Suite 200, Atlanta GA 30339. You possibly can acquire extra details about GLOBALT Investments and its Advisors by accessing IAPD (Funding Adviser Public Disclosure).

NOT A DEPOSIT. NOT FDIC INSURED. NOT GUARANTEED BY THE BANK. MAY LOSE VALUE. NOT INSURED BY ANY FEDERAL AGENCY

[ad_2]

Supply hyperlink