andriano_cz/iStock by way of Getty Photographs

Introduction: Why is Kone Inventory Down?

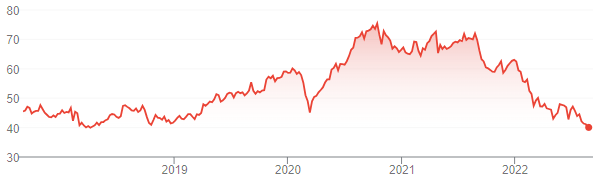

We overview our funding case on Kone Oyj (OTCPK:KNYJY) after shares fell under €40 in Helsinki to a brand new 5-year low:

|

Kone Share Worth (Final 5 Years)  Supply: Google Finance (26-Aug-22). |

We initiated our Purchase score on Kone in June 2020. Shares have now misplaced 28% (after dividends) since our initiation, falling one other 13% since Q2 2022 outcomes on July 20, and are down 47% from their all-time excessive in October 2020.

Kone has been battered by the slowdown in Chinese language development and rising enter prices. Q2 2022 outcomes have been poor, largely attributable to COVID lockdowns in China. The total-year 2022 outlook was minimize once more. Nonetheless, orders grew and there have been indicators of progress in pricing and margins exterior China. China stays the largest unknown for figuring out a backside for Kone’s P&L, and far will depend upon the development sector there.

We now assume EPS will decline by 15% in 2022, however return to rising at 7% yearly from 2023. With Kone shares now buying and selling at 20.4x 2021 EPS, our forecasts point out a complete return of 58% (15.7% annualized) by 2025 year-end. Purchase.

Kone Purchase Case Recap

Kone is a top-Three participant within the world elevator and escalator business. We consider Kone and its friends to be high-quality companies, due to the structural progress in demand from urbanization and taller buildings, recurring Upkeep and Modernization providers (which generate a lot of the earnings, besides in China), a extremely consolidated aggressive panorama, and a capital-light manufacturing mannequin that sources parts from a community of suppliers.

Kone is the #1 participant in China and a top-Three participant in each area besides North America (the place it’s #4). Its world market share is roughly 19% in New Gear and 10% in Providers; throughout the latter it’s a joint #2 in Upkeep.

China had traditionally been a serious supply of earnings and progress for Kone, the place its giant development sector generated high-margin New Gear gross sales. The nation represented as a lot as 35% of Kone’s gross sales in 2021. Nonetheless, the development growth in China has now ended, and Kone has set out new progress targets at its 2022 investor day that rely a lot much less on New Gear gross sales:

- New Gear gross sales to be “secure to low progress”

- Upkeep gross sales to develop at “mid to excessive single-digit”

- Modernization gross sales to develop at “excessive single-digit”

Kone additionally has a goal of elevating Adjusted EBIT margin to 16% (from 12.5% in 2021) As we described in our June 2022 overview, the income progress targets, along with modest margin enlargement (of, say, 35 bps yearly), suggest an roughly 7% annual progress in Adjusted EBIT.

As well as, Kone had traditionally not included computerized worth changes in its backlog of contracts, which implies COVID-related excessive inflation since 2021 has considerably impacted its earnings. Administration has been remedying this with worth will increase, new “dynamic” contract pricing phrases, and value financial savings.

Q2 2022 outcomes have been closely impacted by COVID lockdowns in China, however confirmed progress in Kone’s self-help efforts.

Kone Q2 Closely Hit by China Lockdowns

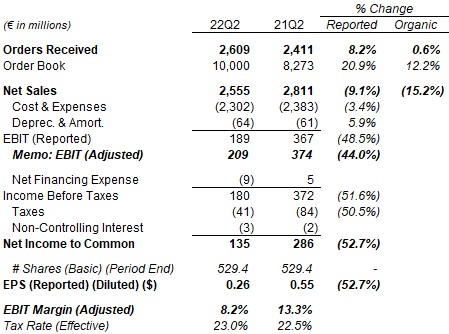

Q2 2022 was a poor quarter for Kone, with Internet Gross sales down 9.1% (15.2% excluding foreign money), Adjusted EBIT down 44.0% (Adjusted EBIT Margin fell to only 8.2%) and Reported EPS down 52.7% year-on-year:

|

Kone Orders and P&L (Q2 2022 vs. Prior 12 months)  Supply: Kone outcomes launch (Q2 2022). |

The culprits have been COVID lockdowns in China and better enter prices. China alone was described as diminished Adjusted EBIT by “over €100m”. Provide chain points and labour shortages in some markets additionally diminished gross sales.

Demand for Kone merchandise remained wholesome, with Orders Acquired up 0.6% and the Order E book up 12.2% year-on-year (excluding foreign money); administration said there was “robust progress” in Orders Acquired within the Americas, EMEA in addition to in Asia-Pacific excluding China.

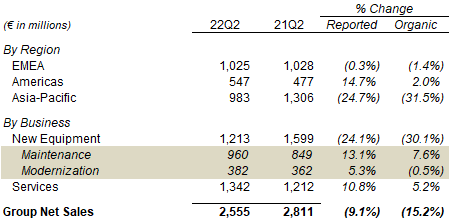

The explanations for Kone’s poor Q2 outcomes are clearer if we take a look at Internet Gross sales by area and by enterprise:

The explanations for Kone’s poor Q2 outcomes are clearer if we take a look at Internet Gross sales by area and by enterprise:

|

Kone Net Gross sales By Area & Enterprise (Q2 2022 vs. Prior 12 months)  Supply: Kone outcomes launch (Q2 2022). |

By area, excluding foreign money, Kone Internet Gross sales have been broadly secure within the Americas (up 2.0% excluding foreign money) and EMEA (down 1.4%), regardless of provide chain points and labor shortages that delayed some tasks and thus revenues. Asia-Pacific Internet Gross sales have been down 31.5% excluding foreign money, however this was totally attributable to China Internet Gross sales falling 40% year-on-year; Internet Gross sales for Asia-Pacific excluding China grew year-on-year in Q2.

By enterprise, excluding foreign money, Upkeep gross sales grew 7.6% year-on-year; Modernization gross sales have been down barely (0.5%), once more attributable to provide chain and labor points. New Gear gross sales have been down by 30.1% once more totally attributable to China; administration said that “New Gear markets exterior of China have truly been good” , with “clear progress” in most markets exterior Central and Northern Europe.

The Chinese language market was down greater than 20% year-on-year in Q2, with COVID lockdowns delaying development in lots of areas and in addition some property builders experiencing monetary difficulties. Kone now expects the Chinese language market to be down 15% for the complete yr. Lockdowns additionally closed down Kone’s manufacturing facility in Kunshan totally for a number of weeks in April and restricted its manufacturing in Might (June was again to regular). Kone’s 40% gross sales decline in China got here from a mixture of weaker quantity, weaker worth in addition to a “slight” unfavourable combine shift.

Kone EBIT Down 35% in H1

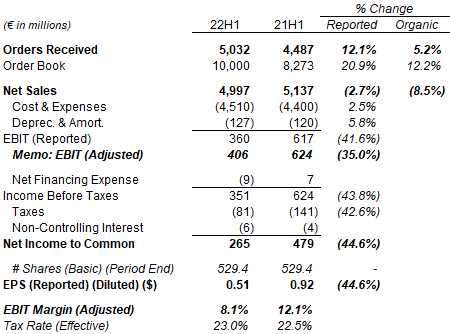

Throughout H1, Kone’s Internet Gross sales have been down 2.7% (8.5% excluding foreign money) and its Adjusted EBIT was down 35% year-on-year; Reported EPS was down 44.6%:

|

Kone Orders and P&L (H12022 vs. Prior 12 months)  Supply: Kone outcomes launch (Q2 2022). |

Nonetheless, Orders Acquired for H1 have been 5.2% increased, once more exhibiting the energy of demand for Kone merchandise.

Full 12 months 2022 Outlook Reduce Once more

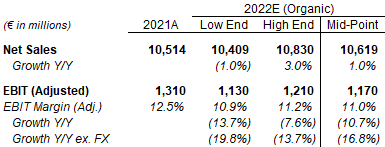

Kone diminished its full-year 2022 outlook. Administration now expects:

- Internet Gross sales progress to be -1% to +3% excluding foreign money (was +2% to +5%)

- Adjusted EBIT to be €1.13-1.21bn (was €1.18-1.28bn)

The Adjusted EBIT outlook consists of expectations that:

- Enter price headwind to be €200m (was €150-200m)

- Foreign money tailwind to be €80m (was €50m)

At mid-point, Kone’s new outlook implies a year-on-year Adjusted EBIT decline of 10.7% (16.8% excluding foreign money):

|

Kone 2022 Outlook  Supply: Kone outcomes presentation (Q2 2022). |

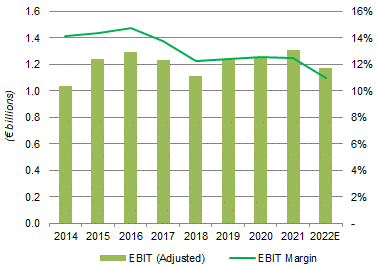

The outlook implies Kone’s Adjusted EBIT will fall for the primary time since 2018 whereas its Adjusted EBIT Margin might be greater than 3.5 ppt decrease than its earlier peak in 2016:

|

Kone Adjusted EBIT & Margin (2014-22E)  Supply: Kone firm filings. |

Whereas these P&L numbers are disappointing, there are some indicators of progress in Kone’s self-help efforts.

Progress in Self-Assist Efforts Outdoors China

Q2 2022 outcomes did comprise proof of progress in Kone’s self-help efforts, a minimum of exterior China.

Pricing progress was good in Upkeep and Modernization, the place Kone was in a position to “virtually absolutely switch to costs the elevated prices”. In New Gear, Kone was “clearly up in costs exterior of China to this point this yr”, having developed positively in Americas, Asia Pacific and Europe throughout Q2, although administration acknowledged that worth will increase don’t but absolutely offset the rise in price; New Gear pricing is “tougher” in China.

Value financial savings on merchandise continued to be recognized, and at charges that have been 2-Three occasions sooner than earlier than. As CEO Henrik Ehrnrooth said on the Q2 earnings name:

Usually after we take a look at product price actions that we take; we have seen possibly 2%, 3% lower on an annual foundation on product price. As I mentioned, now we have been in a position to see 2 occasions to three occasions that”

Margin on Orders Acquired elevated sequentially once more in Q2 2022, helped by the pricing and value enchancment described above. This marked the third consecutive quarter of such will increase (ranging from This fall 2021).

The upper anticipated enter price headwind of €200m might mark the ceiling of that quantity, as a result of administration now has extra visibility over full-year prices and provide chain disruption has began to ease. Once more as Ehrnrooth defined:

Whereas the headwind continues to be very important … we’re beginning to see the primary indicators, I would not say something concrete, however first indicators of enchancment in world provide chains, total logistics, and maybe, part availability …

From an enter price, logistics price perspective, we’ve got a fairly good visibility for the yr of 2022 already. So we’re dedicated and in addition begin to be have a fairly a transparent image on – on the combination which international locations and so forth. So there total the fee headwind now could be the €200 million and there is much less variability there.”

The results of all the above is that administration expects margin to begin to recuperate in Q3:

If you consider the character of the actions clearly we have seen now … margins for orders obtained beginning to enhance latter a part of final yr. A few of these begin to be in supply on the latter a part of the yr, so regularly contributing positively. Additionally, the product price actions that we have talked about, they’ll regularly begin to then affect additionally our manufacturing and be then impacting P&L. So regularly, I anticipate that the margins will then recuperate in direction of the latter a part of the yr, however we are going to begin to see a few of that slowly impacting then additionally Q3”

Ilkka Hara, Kone CFO (Q2 2022 earnings name)

China stays the largest unknown, each due to its dimension and since all the enhancements noticed at Kone to this point have been exterior China. The scenario in China can be macro-driven – if the development sector deteriorates additional, New Gear quantity will fall once more, and pricing will even seemingly worsen with producers competing for an excellent smaller market. Our base case is that the development sector in China will stabilize, because it is just too essential to the general economic system for the federal government to let it fail, and there have been current indicators of recent state help.

Kone Inventory Forecasts

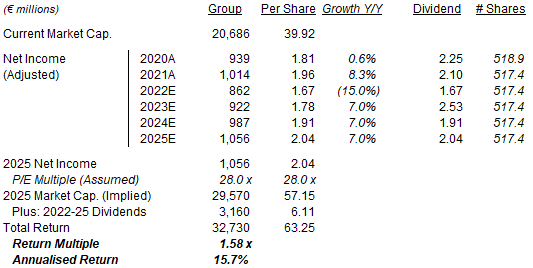

We minimize our forecasts additional to incorporate an excellent bigger EPS decline in 2022, however nonetheless assume the identical return to 7% EPS progress in 2023. We now assume:

- 2022 Internet Revenue decline of 15% (was 7.5%)

- From 2023, Internet Revenue progress of seven.0% annually (unchanged)

- Share rely to be flat (unchanged)

- Dividends to be on a Payout Ratio of 100% (unchanged)

- 2025 year-end P/E of 28.0x (unchanged)

Our new 2025 EPS forecast is 8% decrease than earlier than (€2.22):

|

Kone Illustrative Return Forecasts  Supply: Librarian Capital estimates. |

With shares at €39.92, we anticipate a complete return of 58% (15.7% annualized) by 2025 year-end.

Kone Inventory Valuation

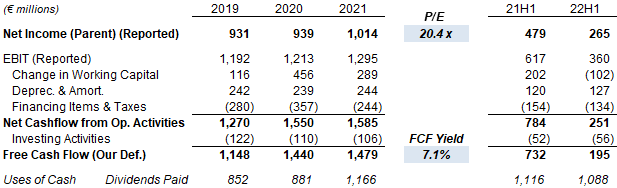

At €39.92, relative to 2021 financials, Kone inventory is buying and selling at a 20.4x P/E and a 7.1% Free Money Circulation Yield:

|

Kone Earnings, Cashflows & Valuation (Since 2019)  Supply: Kone firm filings. |

Relative to the median of our new 2022 EPS forecast of €1.67, Kone inventory is buying and selling at a 24.0x P/E.

Kone paid an everyday dividend of €1.75 per share and a particular dividend of €0.35 per share for Class B shares in March 2022 (in comparison with €1.75 and €0.50 respectively the yr earlier than). This represents a 4.4% Dividend Yield. Whereas the dividend has exceeded EPS lately, Kone’s FCF / Internet Revenue money conversion has usually exceeded 100%, attributable to capital expenditures being decrease than depreciation and dealing capital being a constructive money influx.

Kone has constantly operated with internet money on its steadiness sheet. At €1.26bn at Q2 2022, that is equal to roughly 6% of the present market capitalization.

Is Kone A Purchase? Conclusion

Kone has an excellent underlying enterprise, however the funding case has continued to be sophisticated by the massive publicity to development in China.

We consider the development sector in China will stabilize because it is just too giant for the federal government to let it fail.

On this base case, even assuming a 15% decline in EPS this yr (a number of factors worse than the most recent outlook), offered 7% EPS progress resumes in 2023, buyers can anticipate a complete return of 58% (15.7% annualized).

We reiterate our Purchase score on Kone inventory.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}