[ad_1]

Jose Luis Pelaez Inc

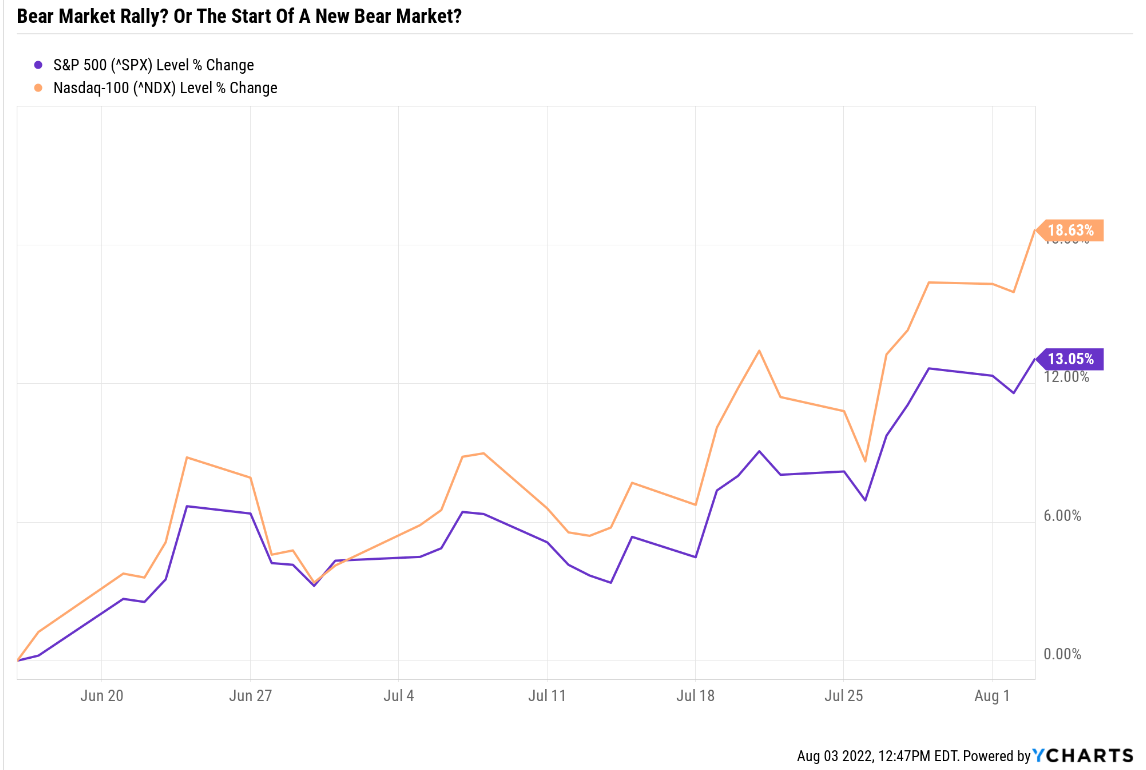

My oh, my, what a distinction a couple of weeks could make on Wall Avenue.

On June 16th, Financial institution of America’s funding sentiment indicator hit 0, a stage solely seen within the Nice Recession and the Pandemic.

Ycharts

The S&P is 13% off the June 16th lows (-24%), and the Nasdaq is up nearly 20%.

Yahoo Finance

Is that this the beginning of the subsequent nice bull market? Or simply one of many many bear market rallies that happen in recessionary bear markets?

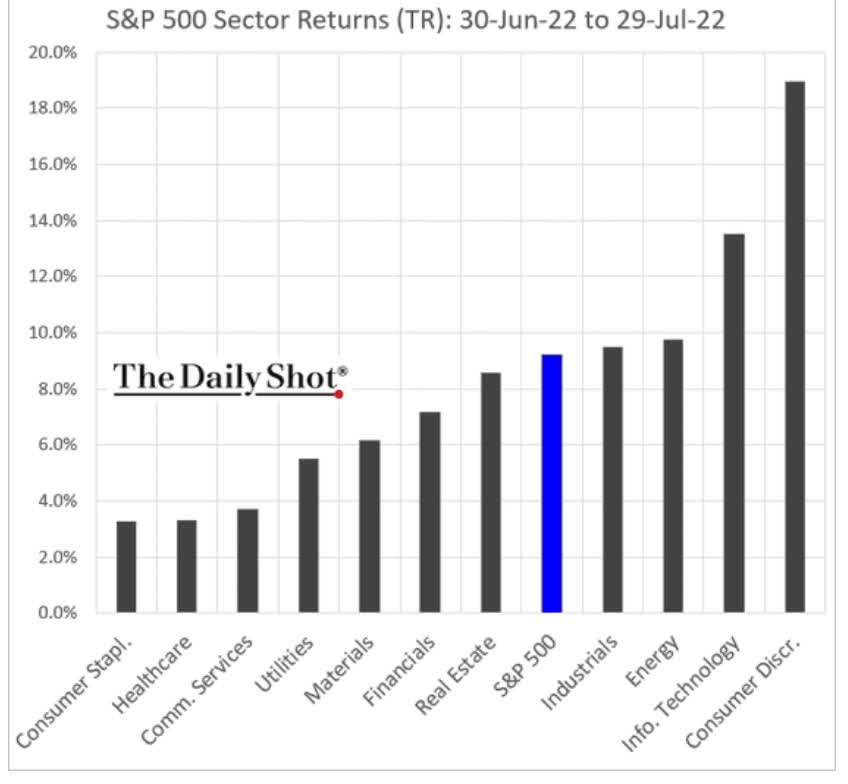

Every day Shot

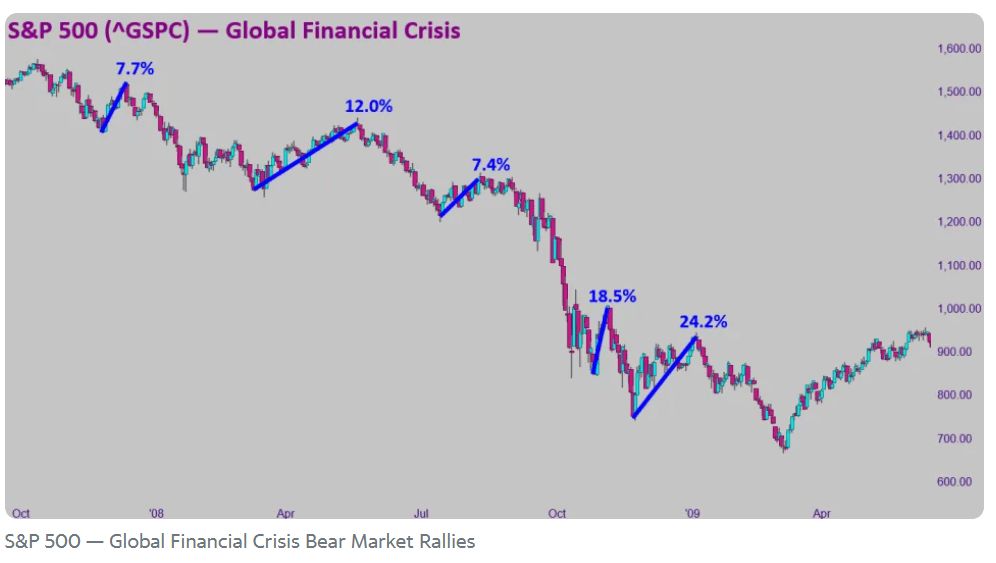

With no recession, the common historic bear market has three bear market rallies.

The typical recessionary bear market has 4, and that is the 4th rally the market has tried to date.

I personally agree with Mike Wilson, CIO of Morgan Stanley, who simply put out his weekly podcast replace.

- Morgan Stanley now expects a 22% EPS decline on this recession

- $195 for the S&P 500 in 2023 EPS

- and a 15.4X trough PE

- 3,003 base case backside for the market (-38% from all-time highs)

I am not saying that Morgan Stanley is 100% proper, and the S&P 500 will drop exactly 27% extra to precisely -38%, however that might be near the historic common bear market backside.

- 13 to 15 trough PE

- 13% to 18% EPS decline

So if I feel that shares are more likely to fall extra, why do not I promote all the pieces I personal and go 3X leveraged quick the Nasdaq or S&P 500 till we hit -38% within the coming months?

“The principle function of Wall Avenue is to make fools of as many males as potential.”

“Do not attempt to purchase on the backside and promote on the high. This cannot be executed – besides by liars.” – Bernard Baruch

Ask all 16 blue-chip economists whether or not they suppose that is the bear market backside, and so they’ll offer you 48 solutions.

- the bullish case, the bottom case, and the bearish case

Wall Avenue runs on possibilities, not certainties, besides for 2:

- diversification will increase long-term risk-adjusted returns (the one “free lunch” on Wall Avenue)

- over the long-term shares at all times go up (97% pushed by fundamentals over 30+ years)

And that is why I am what I wish to name a short-term, totally invested bear.

- I’ve let the market drag me to monster earnings within the final 6 weeks, kicking and screaming all the approach.

Charlie Bilello

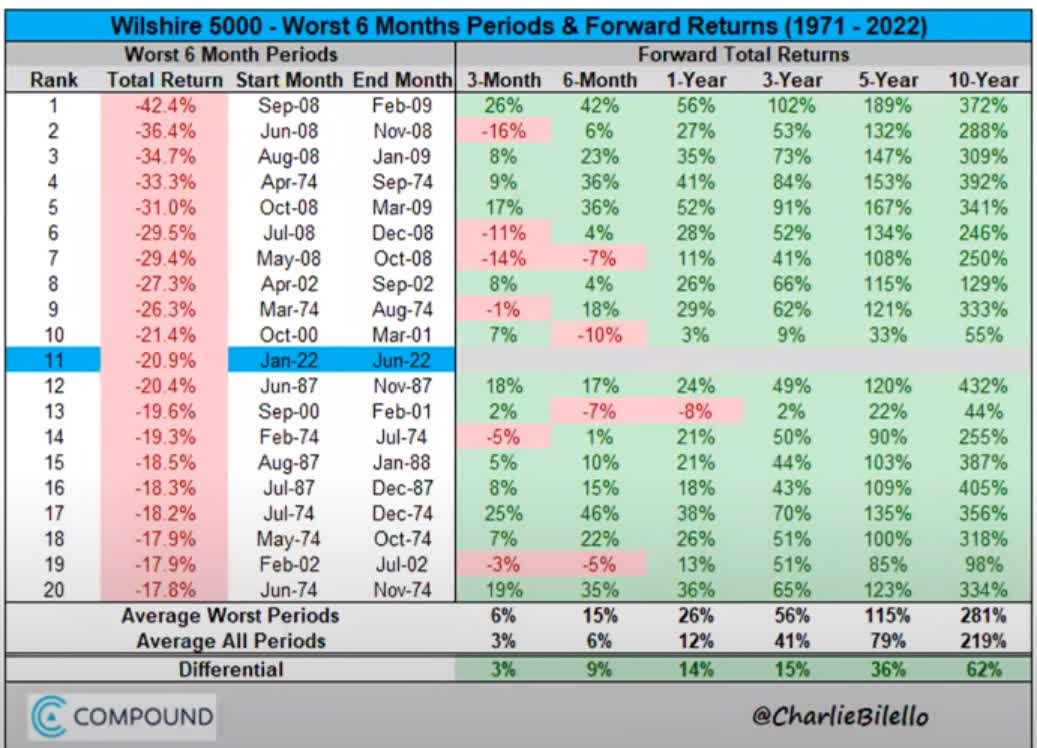

Guess how usually buyers shopping for after the 20 worst 6-month durations in US market historical past have misplaced cash over the subsequent three years? By no means.

How usually did they lose cash over the subsequent 12 months? Solely as soon as, through the tech crash.

What was the common 10-year return? 281%, nearly 4X your cash.

What does this historic return go to if we hit the worst-case state of affairs, a 52% peak decline (UBS stagflation hell recession with -30% EPS progress)?

- 6.9X over the subsequent 10 years

- 14X to 28X for particular person blue-chips

Over any given two to three-year interval, inventory returns are nearly all luck.

| Time Body (Years) |

Complete Returns Defined By Fundamentals/Valuations |

| 1 Day | 0.01% |

| 1 month | 0.25% |

| Three months | 0.75% |

| 6 months | 1.5% |

| 1 | 3% |

| 2 | 6% |

| 3 | 23% |

| 4 | 31% |

| 5 | 39% |

| 6 | 47% |

| 7 | 55% |

| 8 | 62% |

| 9 | 70% |

| 10 | 78% |

| 11+ | 90% to 91% |

| 30+ | 97% |

(Sources: Dividend Kings S&P 500 Valuation & Complete Return Instrument, JPMorgan, Financial institution of America, RIA, Princeton, Constancy)

However over 20 to 30 years? Inventory returns aren’t luck; they’re future. By which I imply fundamentals.

And that is why I am at all times a long-term bull on blue-chip shares, and even after I’m 80% assured shares will fall, I stay 100% invested and persist with my personally optimized threat administration and shopping for plan.

The maths is obvious, the historic file is incontrovertible, and there are three elementary truths that it is advisable bear in mind above all else.

“Fortunes are made in bear markets”. – Todd Sullivan

“Volatility is not threat, it is the supply of future returns.” – Joshua Brown, CEO of Ritholtz Wealth Administration

“Fortunes are made by shopping for proper and holding on.” – Tom Phelps

So let me share with you why there are three fast-growing dividend aristocrat bargains you need to contemplate shopping for earlier than everybody else does.

These aren’t defensive aristocrats. They’re cyclical and have been crushed down the toughest on this bear market. However they’re additionally those that may roar loudest and soar quickest when the subsequent bull market begins.

Every day Shot

So let’s check out why Stanley Black & Decker (SWK), and Caterpillar (CAT) are two dividend aristocrat bargains you need to contemplate shopping for earlier than this bear market ends and so they develop into Wall Avenue darlings as soon as extra.

Stanley Black & Decker: Catch This Falling Dividend King With Conviction And Confidence

In response to John Templeton and Howard Marks, two of the best buyers in historical past, you may solely ever be 80% assured about any firm.

- 80% is the Wall Avenue certainty restrict on blue-chips

- as a result of the info can change over time

- “die on this hill” confidence

I am 80% sure that SWK just isn’t a price entice.

Additional Analysis (Complete Look At The Funding Thesis, Development Outlook, Threat Profile, and Valuation And Complete Return Potential)

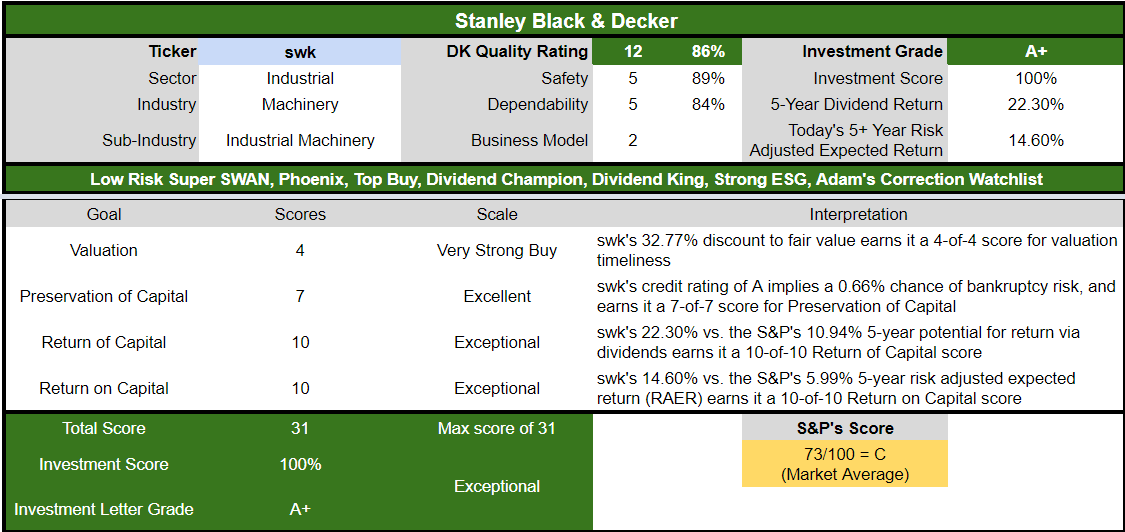

Causes To Doubtlessly Purchase SWK In the present day

- 86% high quality low-risk 12/13 Tremendous SWAN dividend king

- the 143rd highest high quality firm on the Grasp Checklist (71st percentile)

- 89% dividend security rating

- 55-year dividend progress streak

- 3.4% very protected yield

- 0.5% common recession dividend reduce threat

- 1.6% extreme recession dividend reduce threat

- 33% traditionally undervalued (potential very sturdy purchase)

- Honest Worth: $138.70

- 16.6X ahead earnings vs. 16.5X to 18.5X historic

- A- secure credit standing = 2.5% 30-year chapter threat

- 71st trade percentile threat administration consensus = good

- 6% to 12% CAGR margin-of-error progress consensus vary

- 9.4% CAGR median progress consensus

- 5-year consensus whole return potential: 18% to 22% CAGR

- base-case 5-year consensus return potential: 19% CAGR (4X greater than the S&P consensus)

- consensus 12-month whole return forecast: 41%

- Essentially Justified 12-Month Returns: 53% CAGR

Analysts count on SWK to ship 41% whole returns over the subsequent 12 months. If it grows as anticipated and returns to historic honest worth, a 53% whole return could be justified.

This low-risk Tremendous SWAN high quality dividend king hasn’t missed a dividend fee in 145 years, not even by way of eight DEPRESSIONS!

- Financial institution of America thinks US GDP contracts by 0.2% subsequent 12 months, the mildest recession in US historical past.

- Deutsche financial institution thinks it contracts 0.5%, the 2nd mildest recession in US historical past.

And guess who else agrees with me about SWK’s skill to climate this short-term downturn in its enterprise?

- score companies (Moody’s charges it Baa1, BBB+ equal with a adverse outlook, S&P A secure outlook)

- the bond market: 3.81% 30-year default threat in line with an A- credit standing

- 20 analysts who collectively know this firm higher than anybody aside from its wonderful administration group

75% Consensus EPS Development Coming Out Of This Recession

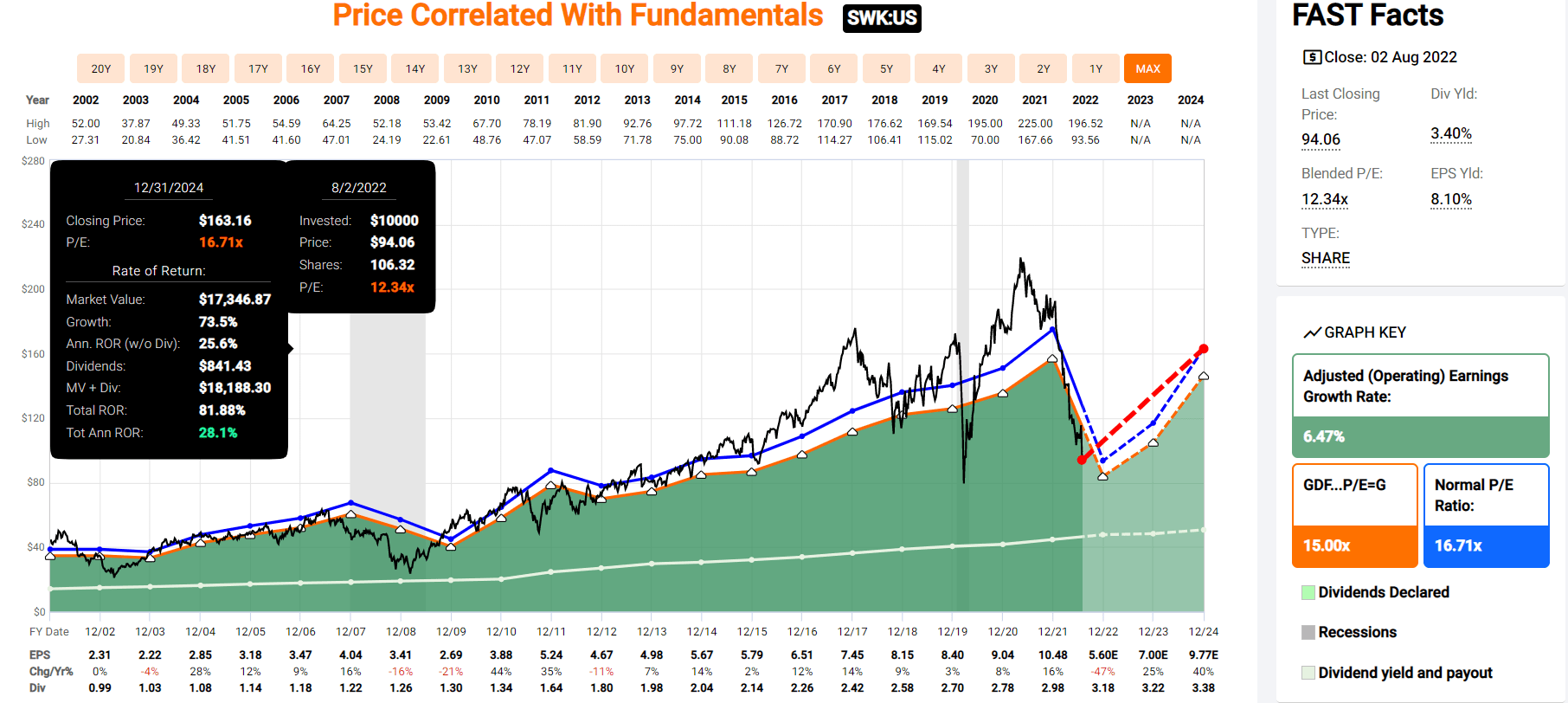

FAST Graphs, FactSet Analysis Terminal

Is that this a nasty downturn for SWK? It is an earnings collapse on par with the Nice Recession.

However analysts count on that SWK will develop its earnings 75% in 2023 and 2024.

Does this sound like a price entice to you? An organization headed to zero?

Administration progress steerage pre-earnings was 10% to 12% long-term progress.

- And probably ship 28% annual Buffett-like returns to anybody able to being “grasping when others are fearful”.

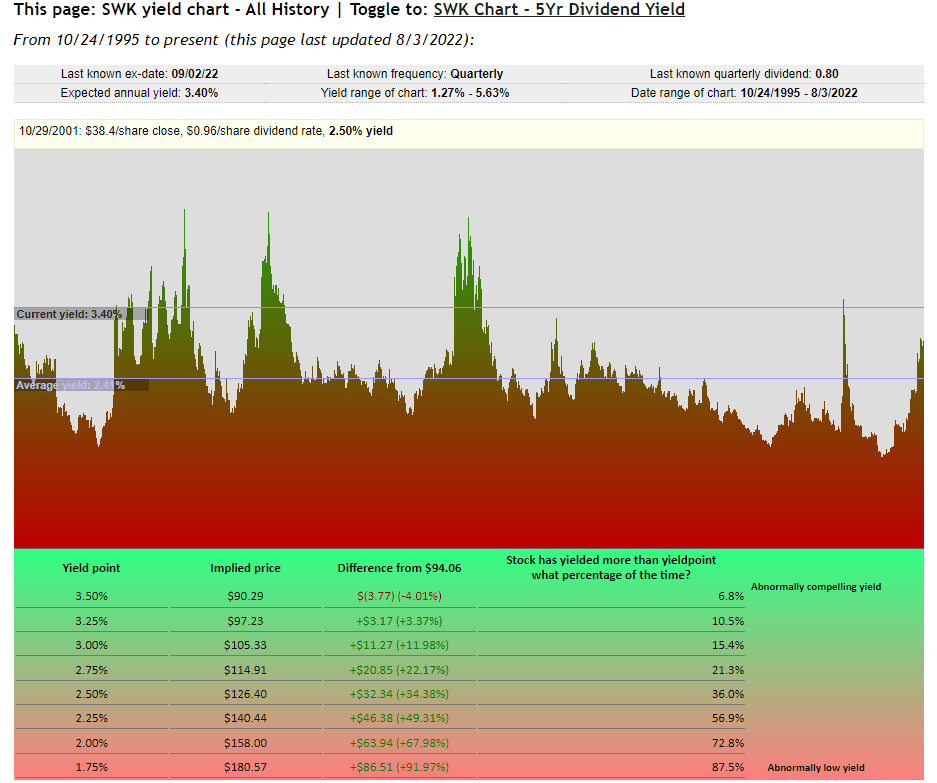

Yieldchart

How usually has SWK had a yield this beneficiant? About 7% of the time… over the past 25 years.

Have you learnt what the analyst consensus expects when you get past 2022’s earnings crash? 9.4% CAGR long-term progress.

| Funding Technique | Yield | LT Consensus Development | LT Consensus Complete Return Potential | Lengthy-Time period Threat-Adjusted Anticipated Return | Lengthy-Time period Inflation And Threat-Adjusted Anticipated Returns | Years To Double Your Inflation & Threat-Adjusted Wealth |

10-Yr Inflation And Threat-Adjusted Anticipated Return |

| Stanley Black & Decker | 3.4% | 9.4% | 12.8% | 9.0% | 6.5% | 11.1 | 1.88 |

| Dividend Aristocrats | 2.6% | 8.6% | 11.1% | 7.8% | 5.3% | 13.5 | 1.68 |

| S&P 500 | 1.7% | 8.5% | 10.2% | 7.1% | 4.7% | 15.4 | 1.58 |

(Sources: Morningstar, FactSet, Ycharts)

Is Stanley a hyper-growth inventory? No.

However with a yield this enticing and really protected, it would not need to be to ship near 13% long-term returns; that is greater than the aristocrats and S&P are providing.

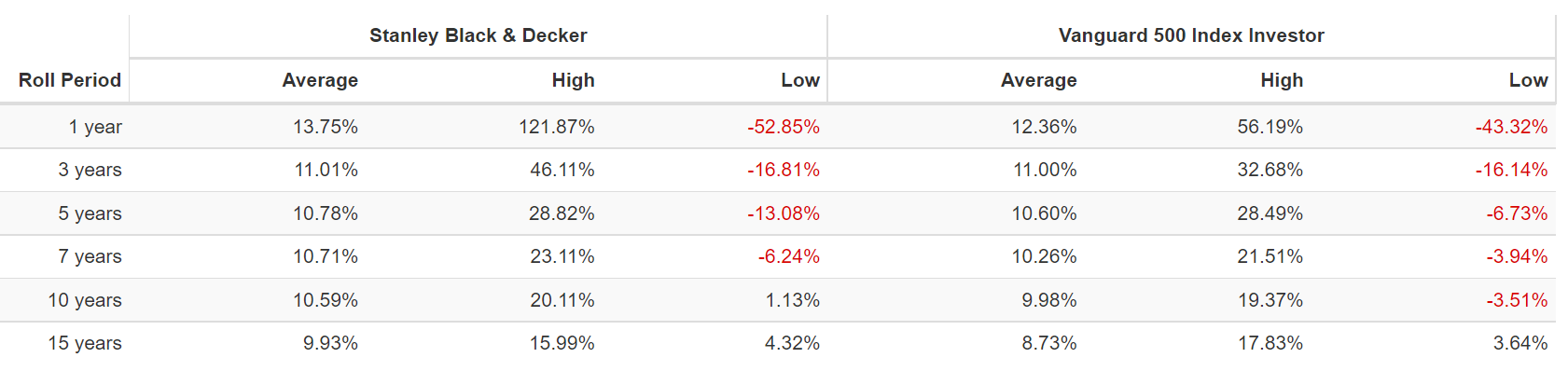

SWK Rolling Returns Since 1985

Portfolio Visualizer Premium

Since 1985 SWK has averaged 14% annular returns and long-term returns of 10% to 11%, barely higher than the S&P 500.

However from bear market lows? Returns as sturdy as 122% within the subsequent 12 months and 20% Buffett-like returns for the subsequent decade.

- 6X over 10 years

- returns as sturdy as 10X over the subsequent 15 years

Inflation-Adjusted Consensus Complete Return Potential: $1,000 Preliminary Funding

| Time Body (Years) | 7.7% CAGR Inflation-Adjusted S&P Consensus | 8.6% Inflation-Adjusted Aristocrat Consensus | 10.3% CAGR Inflation-Adjusted SWK Consensus | Distinction Between Inflation-Adjusted SWK Consensus And S&P Consensus |

| 5 | $1,451.05 | $1,512.69 | $1,634.81 | $183.76 |

| 10 | $2,105.56 | $2,288.22 | $2,672.61 | $567.06 |

| 15 | $3,055.27 | $3,461.36 | $4,369.22 | $1,313.95 |

| 20 | $4,433.36 | $5,235.95 | $7,142.86 | $2,709.50 |

| 25 | $6,433.04 | $7,920.35 | $11,677.25 | $5,244.20 |

| 30 | $9,334.69 | $11,981.01 | $19,090.12 | $9,755.43 |

(Supply: DK Analysis Terminal, FactSet)

Analysts suppose SWK has the potential to ship 19X inflation-adjusted returns over the subsequent 30 years, the usual retirement time-frame.

| Time Body (Years) | Ratio Aristocrats/S&P Consensus | Ratio Inflation-Adjusted SWK Consensus vs. S&P consensus |

| 5 | 1.04 | 1.13 |

| 10 | 1.09 | 1.27 |

| 15 | 1.13 | 1.43 |

| 20 | 1.18 | 1.61 |

| 25 | 1.23 | 1.82 |

| 30 | 1.28 | 2.05 |

(Supply: DK Analysis Terminal, FactSet)

That is probably 2X the S&P 500’s returns and 60% higher than the dividend aristocrats.

However you do not have to attend 30 years for probably superb returns from SWK.

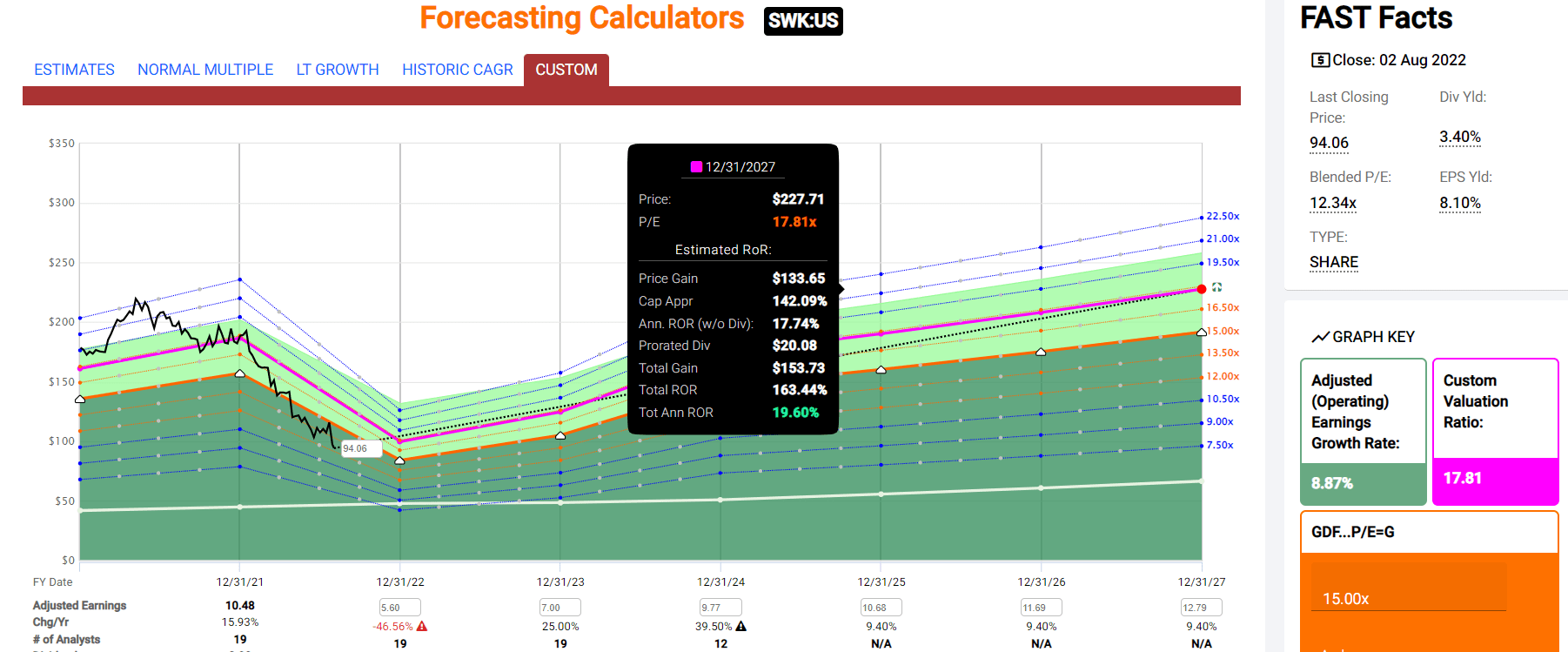

SWK 2027 Consensus Return Potential

(Supply: FAST Graphs, FactSet Analysis)

If SWK grows as anticipated and returns to honest worth by 2027, buyers may see 165% returns or nearly 20% yearly.

- 4X the S&P 500 consensus

- actually Buffett-like return potential from this dividend king discount

SWK Funding Choice Rating

DK Dividend Kings Automated Funding Choice Instrument

SWK is without doubt one of the most affordable and prudent dividend king bargains on Wall Avenue for anybody snug with its threat profile.

- 33% low cost vs. 4% market premium = 37% higher valuation

- 2X the a lot safer yield

- 30% higher consensus long-term return potential

- 3X higher risk-adjusted anticipated return over the subsequent 5 years

- 2X greater consensus earnings over the subsequent 5 years

Caterpillar: A $40 Trillion Megatrend Is Powering Its Future Development

Additional Analysis (Subsequent week, I will do a full deep dive on CAT, protecting its progress prospects, funding thesis, valuation profile, whole return potential, and threat profile)

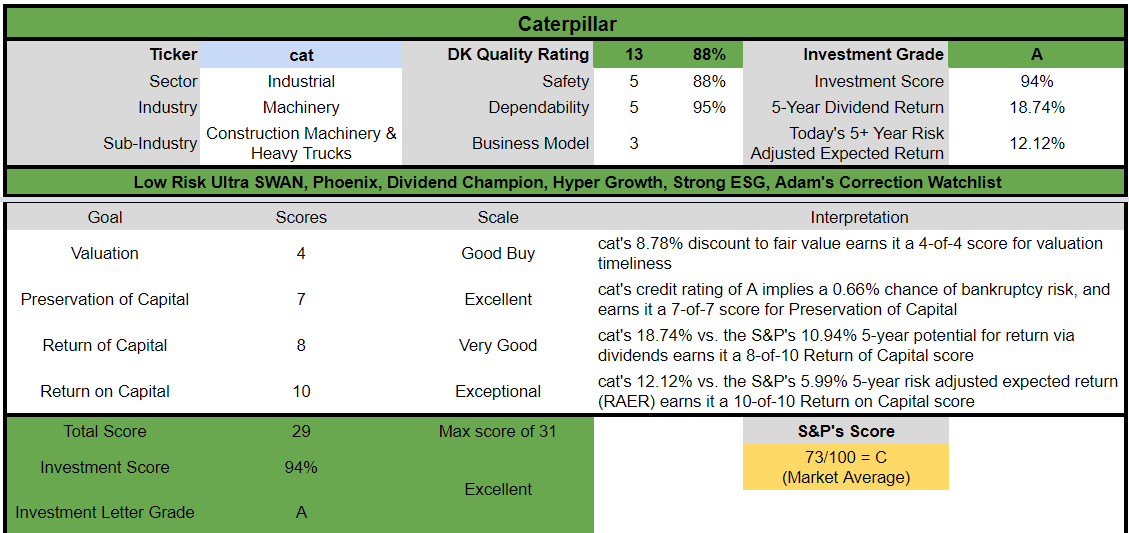

Causes To Doubtlessly Purchase CAT In the present day

- 88% high quality low-risk 13/13 Extremely SWAN dividend aristocrat

- the 104th highest high quality firm on the Grasp Checklist (79th percentile)

- 88% dividend security rating

- 28-year dividend progress streak

- 2.6% very protected yield

- 0.5% common recession dividend reduce threat

- 1.65% extreme recession dividend reduce threat

- 9% traditionally undervalued (potential very sturdy purchase)

- Honest Worth: $200.83

- 14.6X ahead earnings vs. 16.5X to 9X historic

- 12.3X cash-adjusted earnings: 1.04 PEG vs. 1.54 historic

- A secure credit standing = 0.66% 30-year chapter threat

- 72nd trade percentile threat administration consensus = good

- 9% to 19% CAGR margin-of-error progress consensus vary

- 11.8% CAGR median progress consensus

- 5-year consensus whole return potential: 11% to 22% CAGR

- base-case 5-year consensus return potential: 16% CAGR (2X greater than the S&P consensus)

- consensus 12-month whole return forecast: 23%

- Essentially Justified 12-Month Returns: 12% CAGR

Earnings Replace: Simply A Regular Recession

Provide Headwinds Persist in Caterpillar’s Second Quarter, however Demand Stays Robust:

We proceed to stay optimistic on the demand story for Caterpillar, regardless of provide headwinds. The corporate has been pressured by the chip scarcity and better manufacturing prices over the previous 12 months, difficult its skill to satisfy present demand. Nonetheless, we consider building exercise will proceed to enhance within the close to time period, giving us confidence that Caterpillar’s merchandise will see sturdy demand from prospects over our forecast. As well as, we expect the development trade will profit from elevated U.S. infrastructure spending beginning in 2023. Given this backdrop, we have raised our honest worth estimate to $193 per share from $189. – Morningstar

Caterpillar is not going through an absence of demand; it is simply provide constrained.

And given the $40 trillion in world infrastructure spending analyst agency KPMG expects by way of 2050, CAT may face such an exquisite downside for many years to come back.

Within the second quarter, equipment gross sales elevated 11% 12 months on 12 months to $13.5 billion, largely attributable to sturdy gross sales in North America, which grew 18% 12 months on 12 months. The corporate’s equipment working margins fell roughly 30 foundation factors from 2021 ranges, given persistent value inflation (supplies and freight prices). That mentioned, administration famous its skill to greater than offset rising prices with sturdy worth realization. We count on Caterpillar to additionally elevate costs within the again half of the 12 months at a high-single-digit clip to remain forward of inflation. For 2022, we undertaking over 15% gross sales progress for Caterpillar’s consolidated enterprise. – Morningstar

Morningstar expects 15% gross sales progress this 12 months and analysts, after the earnings miss, count on 15% as nicely.

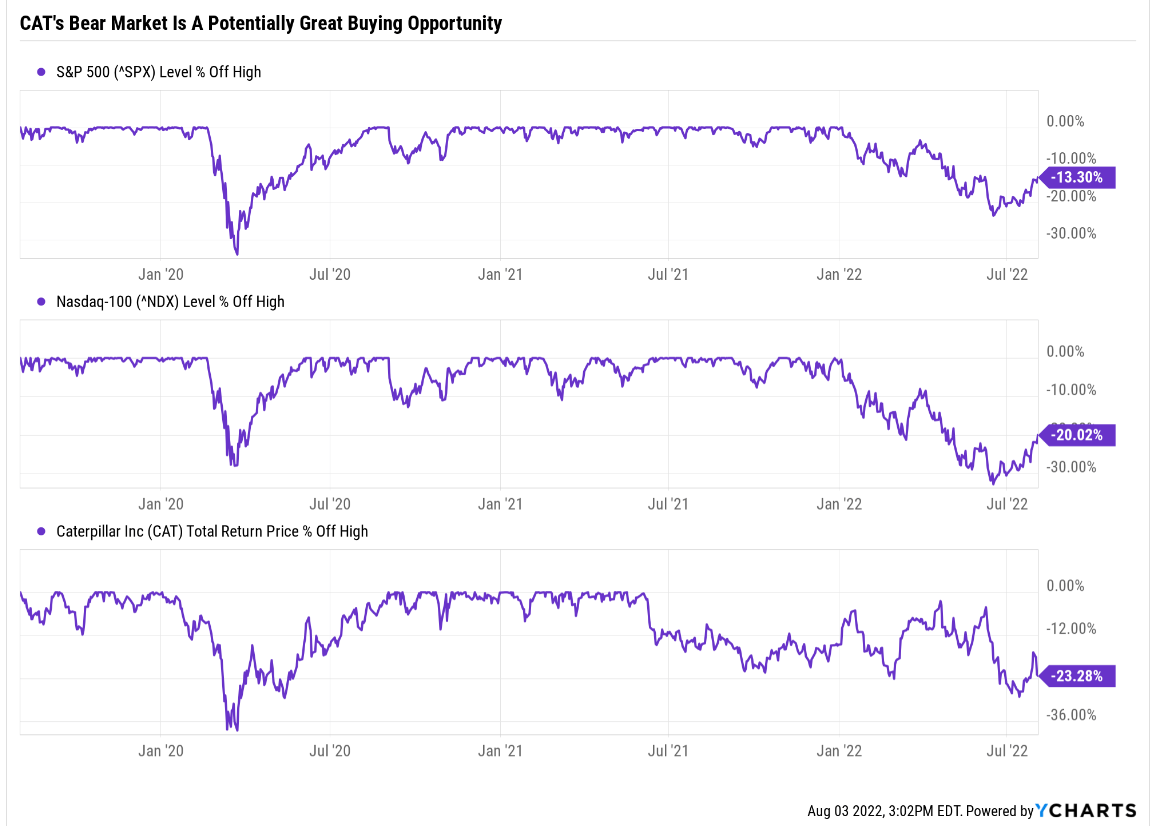

What in regards to the coming recession? Is CAT immune from that? After all not.

- 2023 gross sales progress consensus: 7%

- 2024 consensus: 0%

However 7% progress by way of a worldwide recession? Does that sound like a possible worth entice?

Within the close to time period, we expect how the availability chain progresses would be the key merchandise to look at. Whereas we count on the rest of 2022 to be difficult, we count on to see enhancements in 2023, giving Caterpillar the flexibility to satisfy demand (the corporate has sturdy backlogs). This offers us confidence to undertaking stronger working margins in 2023 (15.8%) in contrast with 2022 (13.9%) as elevated prices begin to ease. Specializing in the infrastructure alternative, we expect sellers will begin to restock inventories in 2023, main us to undertaking over 6% gross sales progress on common for 2023-25.

Analysts agree with Morningstar that issues will not be straightforward for CAT the remainder of the 12 months or the subsequent few years. In any case, we’re probably headed for recession. So what sort of catastrophic earnings declines are CAT anticipated to face within the subsequent two years?

- 2023 consensus: +13%

- 2024 consensus: +9%

Ycharts

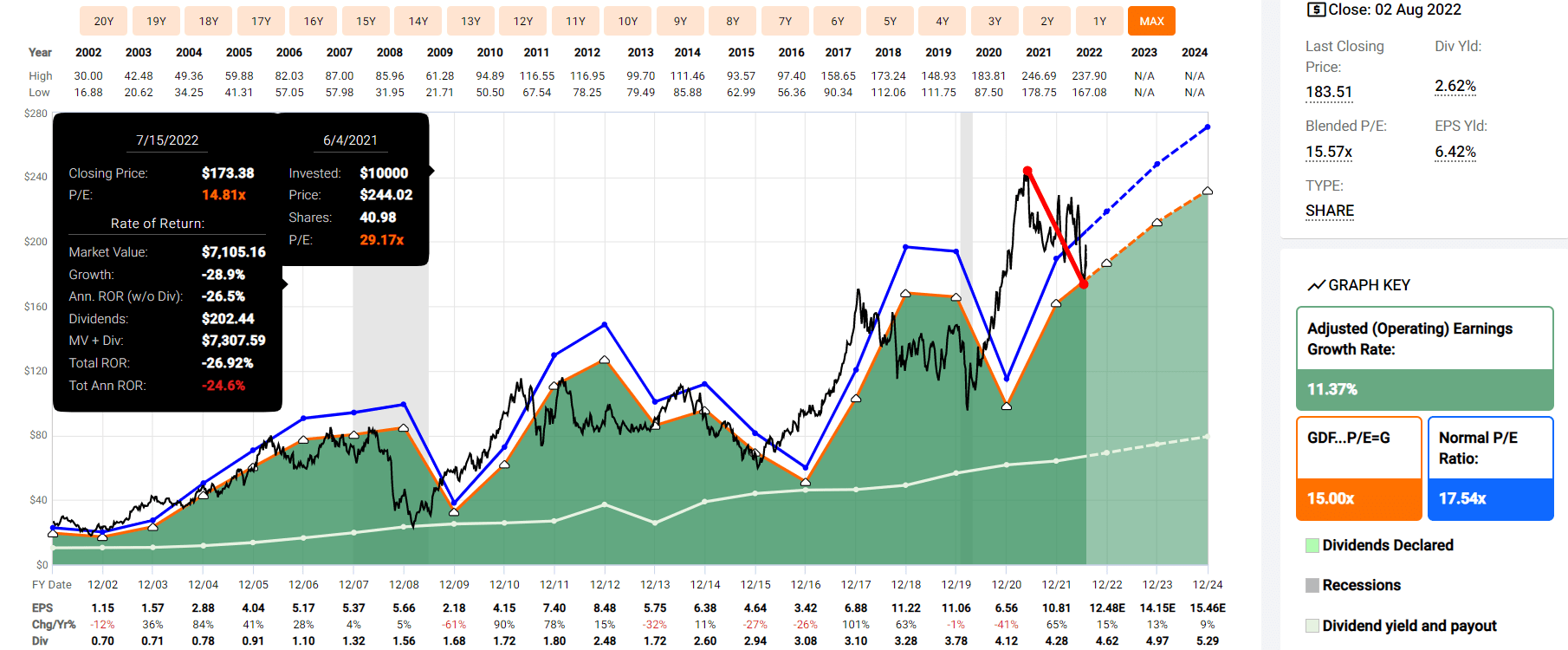

So why is CAT in a 30% bear market? As a result of CAT was buying and selling at 29X earnings at its peak, for a corporation with a historic PE of 17.5.

FAST Graphs, FactSet Analysis Terminal

However guess what? Whereas CAT is not a screaming discount at this time, it’s a probably good purchase for anybody snug with its threat profile.

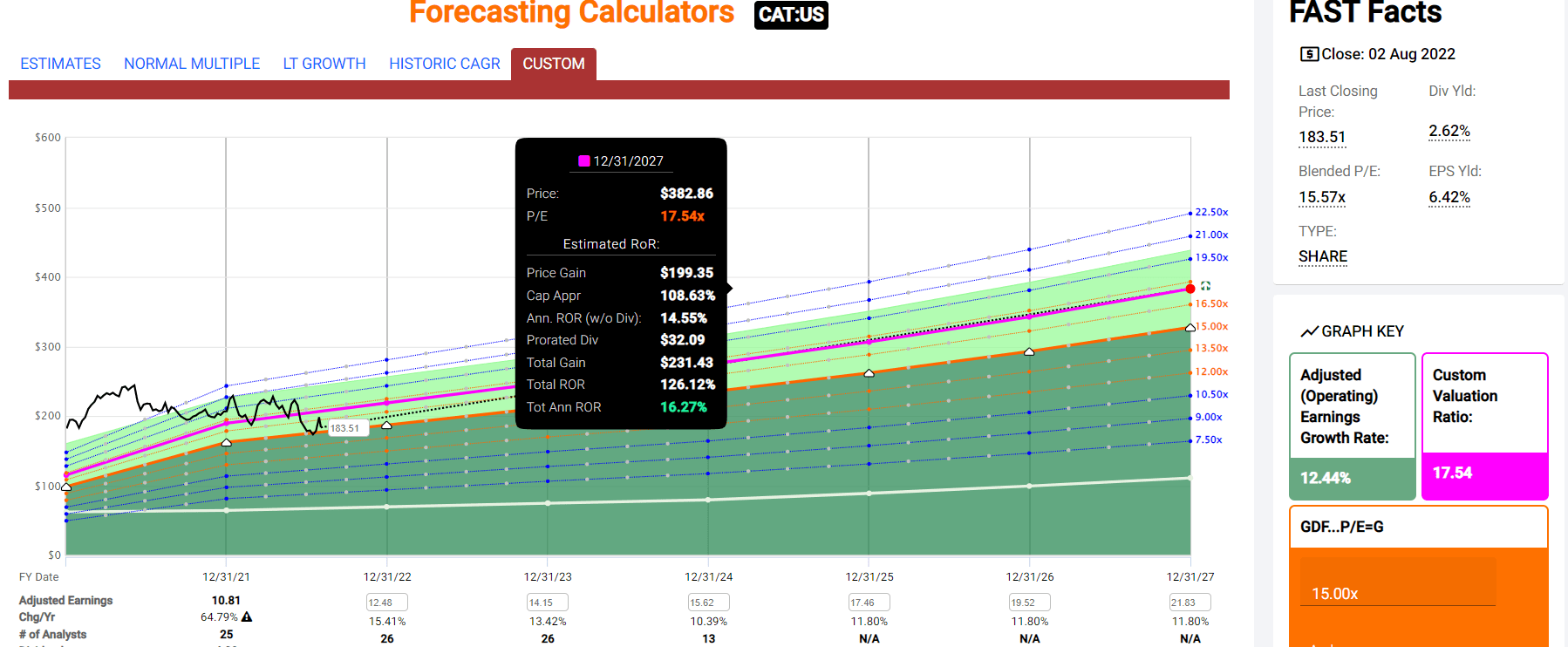

CAT 2024 Consensus Complete Return Potential

FAST Graphs, FactSet Analysis Terminal

Over the subsequent 2.5 years, together with the potential recession, analysts suppose CAT may ship 16% annual returns, or 2X greater than the S&P 500.

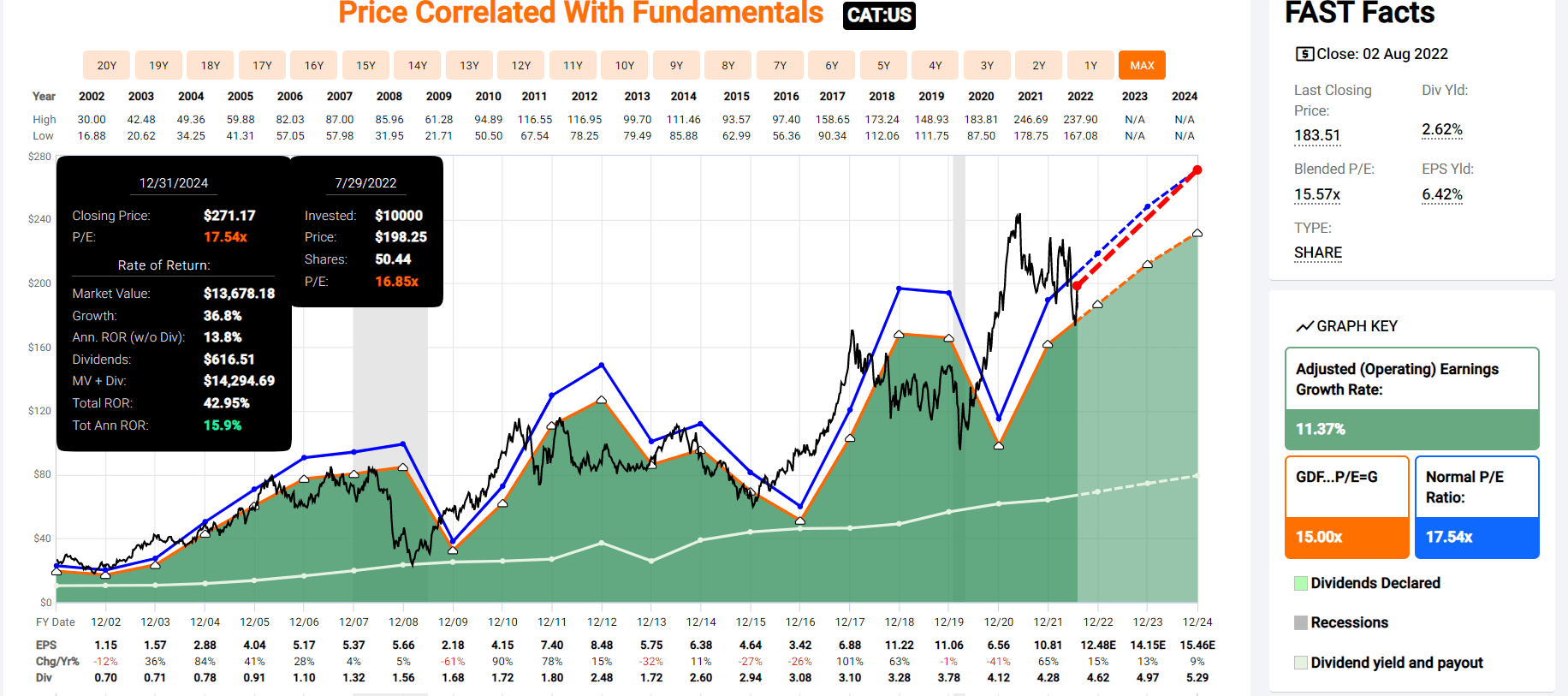

CAT 2027 Consensus Complete Return Potential

FAST Graphs, FactSet Analysis Terminal

By way of 2027 analysts suppose CAT may ship 126% whole returns, or 16% yearly.

- 2.5X greater than the S&P 500 consensus

| Funding Technique | Yield | LT Consensus Development | LT Consensus Complete Return Potential | Lengthy-Time period Threat-Adjusted Anticipated Return | Lengthy-Time period Inflation And Threat-Adjusted Anticipated Returns | Years To Double Your Inflation & Threat-Adjusted Wealth |

10-Yr Inflation And Threat-Adjusted Anticipated Return |

| Caterpillar | 2.6% | 11.8% | 14.4% | 10.1% | 7.6% | 9.5 | 2.08 |

| Dividend Aristocrats | 2.6% | 8.6% | 11.1% | 7.8% | 5.3% | 13.5 | 1.68 |

| S&P 500 | 1.7% | 8.5% | 10.2% | 7.1% | 4.7% | 15.4 | 1.58 |

(Sources: Morningstar, FactSet, Ycharts)

Analysts count on CAT to probably ship 14% long-term returns, operating circles across the aristocrats and S&P.

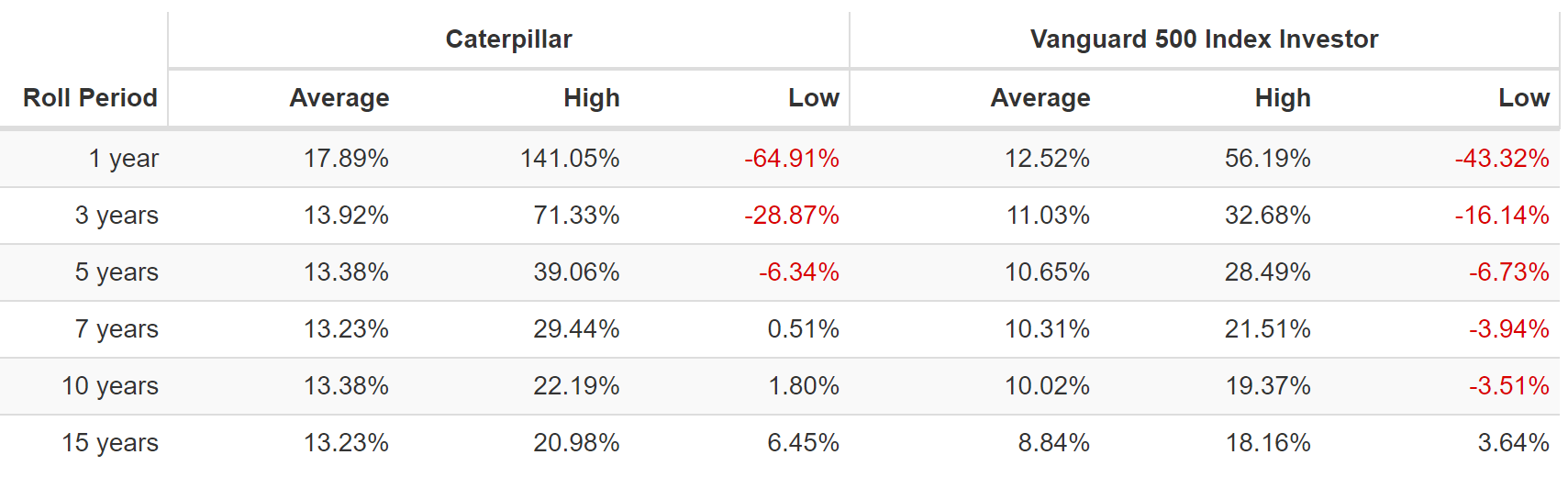

CAT Rolling Returns Since 1985

Portfolio Visualizer Premium

Since 1985 CAT’s common rolling returns have been 13% to 14% CAGR, precisely what analysts count on sooner or later.

- the one purpose CAT might be a nasty purchase at this time is that if the thesis have been damaged

- it is not

- the identical progress price of the final 20 years is predicted sooner or later

- and a $40 trillion megatrend makes that progress possible

How can I be so assured about CAT?

- Administration says the thesis is undamaged

- 28 analysts say CAT will develop at historic charges

- S&P, Fitch, Moody’s, Fitch, and DBRS (Canada’s largest score company) all have A-stable credit score rankings for CAT

- the bond market by way of insurance coverage insurance policies towards default (credit score default swaps) says CAT’s 30-year default threat is 2.4% (A-rated)

- with falling default threat over the past three months

- 5 extra threat score companies contemplate CAT within the 72nd percentile for long-term threat administration

On one aspect are administration and a consensus of 37 analysts, score companies, and the bond market.

This group has studied CAT for many years and is aware of it higher than anybody aside from its wonderful administration group.

And on the opposite are the CAT bears who’re peddling concern, uncertainty, and doubt. Or just arguing that CAT won’t go up within the short-term (momentum merchants).

Properly, guess what I do not care about? Brief-term momentum. Guess what I do care about? Serving to you

Inflation-Adjusted Consensus Complete Return Potential: $1,000 Preliminary Funding

| Time Body (Years) | 7.7% CAGR Inflation-Adjusted S&P Consensus | 8.6% Inflation-Adjusted Aristocrat Consensus | 11.9% CAGR Inflation-Adjusted CAT Consensus | Distinction Between Inflation-Adjusted CAT Consensus And S&P Consensus |

| 5 | $1,451.05 | $1,512.69 | $1,756.84 | $305.79 |

| 10 | $2,105.56 | $2,288.22 | $3,086.49 | $980.94 |

| 15 | $3,055.27 | $3,461.36 | $5,422.47 | $2,367.20 |

| 20 | $4,433.36 | $5,235.95 | $9,526.43 | $5,093.07 |

| 25 | $6,433.04 | $7,920.35 | $16,736.42 | $10,303.38 |

| 30 | $9,334.69 | $11,981.01 | $29,403.23 | $20,068.55 |

(Supply: DK Analysis Terminal, FactSet)

Analysts suppose CAT has the potential to ship 29X inflation-adjusted returns over the subsequent 30 years, the usual retirement time-frame.

| Time Body (Years) | Ratio Aristocrats/S&P Consensus | Ratio Inflation-Adjusted CAT Consensus vs. S&P consensus |

| 5 | 1.04 | 1.21 |

| 10 | 1.09 | 1.47 |

| 15 | 1.13 | 1.77 |

| 20 | 1.18 | 2.15 |

| 25 | 1.23 | 2.60 |

| 30 | 1.28 | 3.15 |

(Supply: DK Analysis Terminal, FactSet)

That is probably 3X the S&P 500’s returns and a pair of.5X higher than the dividend aristocrats.

29X inflation-adjusted returns from a dividend aristocrat? That is loopy, it is unimaginable… it is what CAT has been doing since 1985!

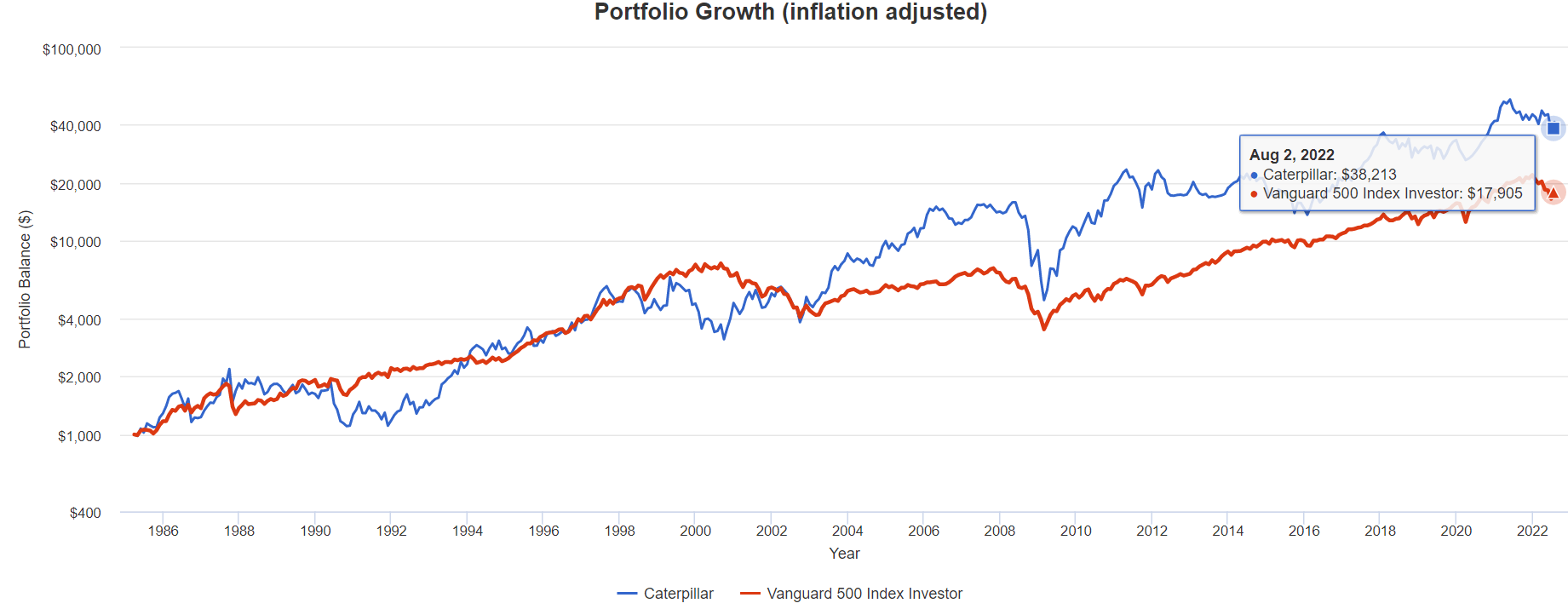

CAT Complete Returns Since 1985

(Supply: Portfolio Visualizer Premium)

CAT is a 106X bagger over the past 37 years.

- You do not want crypto to develop your wealth 100X

- You simply want endurance and the world’s greatest blue-chips

(Supply: Portfolio Visualizer Premium)

How do 38X inflation-adjusted returns that greater than doubled the market sound? Like an unimaginable dream? No, it is actually what CAT did and will probably hold doing for many years to come back.

CAT Cumulative Dividends Since 1986: $1,000 Beginning Funding

| Complete Dividends | $24,825 |

| Annualized Earnings Development Charge | 15.26% |

| Complete Earnings/Preliminary Funding | 24.83 |

| Inflation-Adjusted Earnings/Preliminary Funding | 9.19 |

(Supply: Portfolio Visualizer Premium) – dividends reinvested

Buyers who purchased CAT in 1986 (at a modest 1.6% yield) have loved 15% annual earnings progress for 36 years.

- their yield on value is now 265%

They’ve obtained over 9X their preliminary funding again in inflation-adjusted dividends.

- and in 2023, they are going to get again greater than their preliminary funding

- adjusted for inflation

Behold the magic of long-term dividend blue-chip compounding! Behold the facility of bear market discount looking!

CAT Funding Choice Rating

DK Dividend Kings Automated Funding Choice Instrument

CAT is without doubt one of the most affordable and prudent fast-growing dividend aristocrat alternatives on Wall Avenue for anybody snug with its threat profile.

- 9% low cost vs. 4% market premium = 13% higher valuation

- 2.6% yield vs. 1.7% S&P 500 (and a a lot safer yield at that)

- 40% higher consensus long-term return potential

- 2X higher risk-adjusted anticipated return over the subsequent 5 years

- nearly 2X greater consensus earnings over the subsequent 5 years

Backside Line: Purchase These 2 Dividend Aristocrat Bargains Earlier than Everybody Else Does

Is that this the 4th (and probably last) bear market rally of this downturn? Or the beginning of a 10-year bull market?

Sensible long-term buyers know that these are the incorrect inquiries to ask. The best query is, what world-class blue-chips are you able to entrust along with your hard-earned financial savings on this unbelievable shopping for alternative?

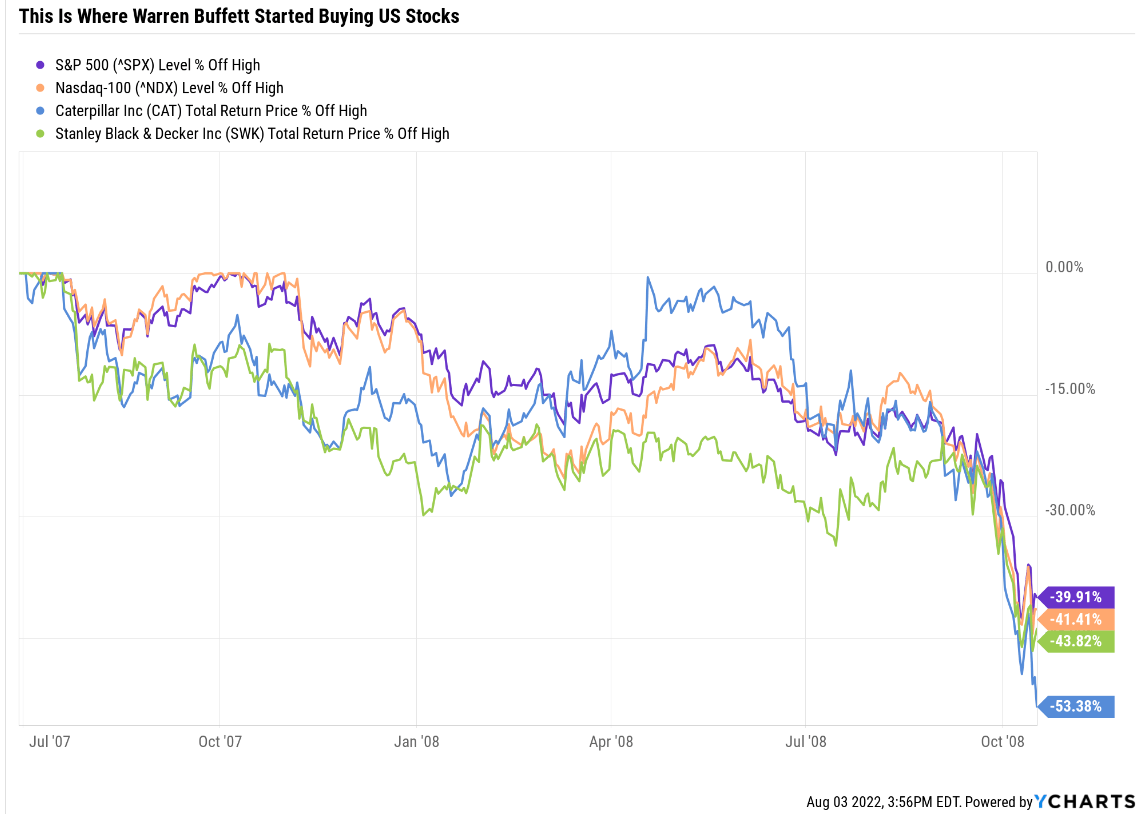

Warren Buffett began shopping for shares by the billions in October 2008. He even wrote an op-ed about it within the New York Instances.

NYT

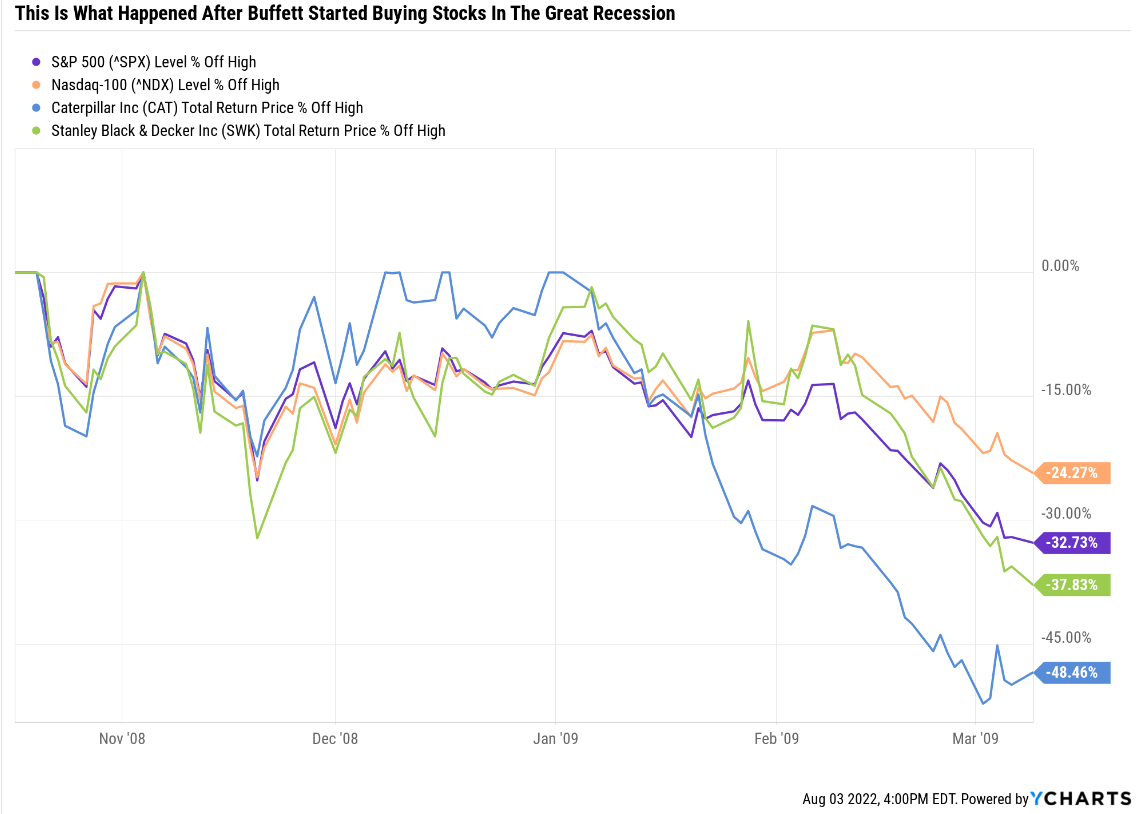

The market was down 40% when Buffett began being grasping when others have been fearful.

Ycharts

The Nasdaq was down 41%, SWK was down 44%, and CAT was down 53%. Did Buffett attempt to time the underside? Heck no! He noticed fats pitch alternatives, and he swung for the fences.

And guess what occurred subsequent?

Ycharts

After Buffett publicly advised People to begin shopping for shares, the S&P fell one other 33%, and CAT was reduce in half… once more.

What an fool! Oracle of Omaha, my butt! Buffett was useless incorrect to purchase shares in October 2008, when it was SO OBVIOUS that shares may solely hold falling.

Are you able to think about the individuals Buffett damage by recklessly telling them to purchase US shares in that bear market?!

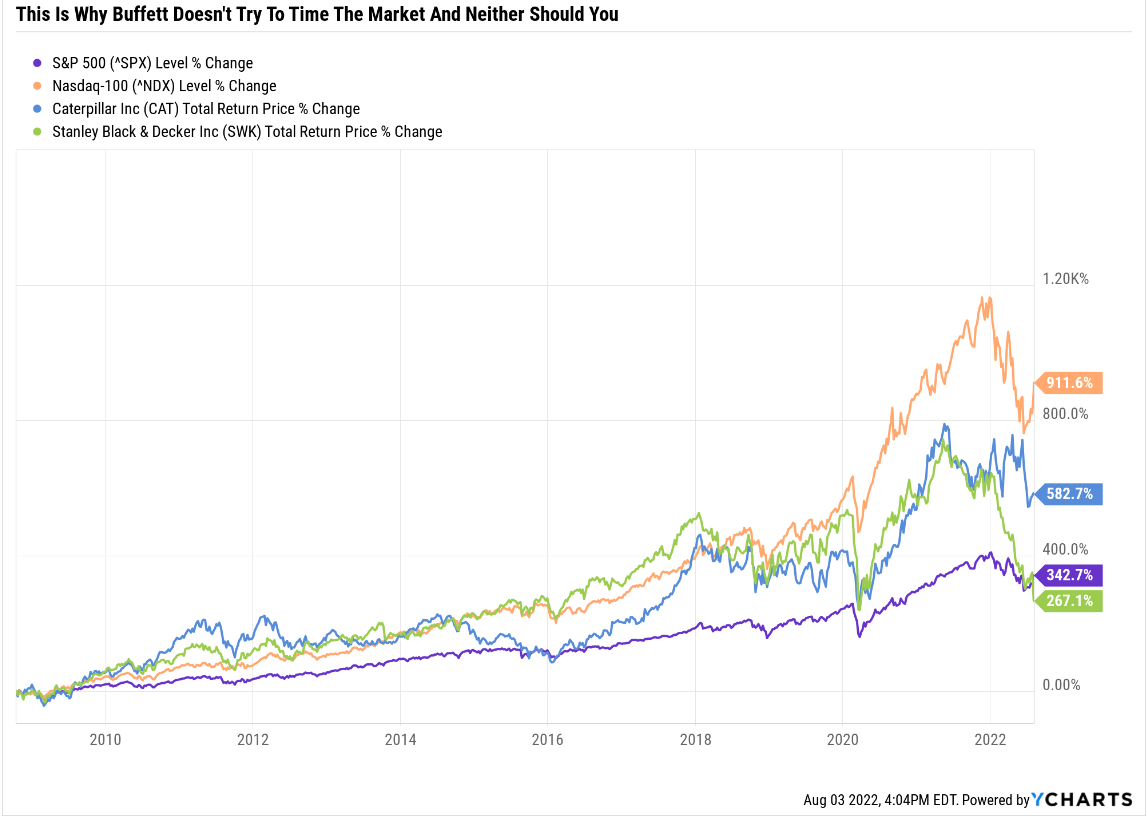

Ycharts

Simply check out how the “idiots” who adopted Buffett’s recommendation did!

| Funding | Positive aspects Since October 18th, 2008 | Annualized Return | Inflation-Adjusted Annual Return |

| S&P | 583% | 14.7% | 12.4% |

| Nasdaq | 912% | 18.0% | 15.7% |

| Stanley Black & Decker | 267% | 9.7% | 7.4% |

| Caterpillar | 343% | 11.2% | 8.9% |

(Sources: YCharts, Bureau of Labor Statistics)

Even with SWK down 57% off its highs, SWK buyers who purchased in October 2008, after which suffered one other 38% decline, have achieved 7.4% annual inflation-adjusted returns!

- They nearly quadrupled their cash shopping for at “the incorrect time” and holding throughout “the incorrect time”

CAT buyers are up nearly 4.5X, together with the present bear market.

S&P buyers are up nearly 7X, regardless of horrible market timing and an incapability to see how “apparent” it was in January 2022 that the market was going to crash.

Nasdaq buyers are up over 10X, regardless of it being so “apparent” that the Fed would tighten and tech blue-chips would crash 30% this 12 months.

“Do not attempt to purchase on the backside and promote on the high. This cannot be executed – besides by liars.” – Bernard Baruch

“Do not attempt to time the market and nail the precise backside. Belief me, in 10 years you will really feel such as you purchased the underside.” – Michael Batnick

I do not care whether or not SWK, CAT, or the market usually goes up, down, or sideways within the subsequent one, two, and even three years.

In the event you aren’t keen to personal a inventory for ten years, do not even take into consideration proudly owning it for ten minutes. – Warren Buffett

I am not right here that will help you rating a fast 2X, 5X, and even 10X return in speculative property like crypto, SPACs, or meme shares.

I am right here that will help you obtain 20X, 30X, and even 50X inflation-adjusted returns over many years.

Speculators attempt to double their cash rapidly. Sensible buyers attempt to change their lives by way of compounding over time.

Gamblers attempt to time the market and get fortunate, and 98% of them fail. Prudent buyers make their very own luck by shopping for nice blue-chips at good to nice costs in occasions like these.

And that is why I’ve no qualms about recommending SWK or CAT for long-term buyers at this time.

I’m 80% assured that for those who purchase them as a part of a diversified and prudently risk-managed portfolio at this time, you will be very pleased with the ends in 5+ years.

As a result of once you purchase aristocrats like these in occasions like these? You do not simply generate profits; you may usually retire in security and splendor.

[ad_2]

Supply hyperlink