[ad_1]

KangeStudio

Are we heading for a recession?

That is the query on everybody’s thoughts as markets fell sharply through the second quarter on the heels of excessive inflation information factors and the Federal Reserve Financial institution’s resolve to combat inflation even when it creates a recession. We expect a greater query is “what may a recession truly appear like when (not if) it occurs?” Within the post-World Battle II US financial system, we expertise a recession as soon as each six years and this contains the extended growth post-Monetary Disaster by means of COVID-recession.

Contemplating that our funding time horizon is 5 years, we all the time ponder a recession someplace inside affordable distance of our underwriting course of on each funding we make. One chilly, arduous actuality of investing that everybody should face is how there will probably be durations of growth, durations that appear like we’d head for contraction, and precise contractions (what we name recessions). In different phrases, there isn’t a investing with out contending with close to recessions and precise recessions, although we solely know the distinction between the 2 in hindsight.

One downside that many battle with at the moment is that outdoors of the COVID lockdown-induced recession of 2020, we now have not skilled a recession for the reason that Nice Monetary Disaster. Recency bias leads most to anticipate the carnage of any “subsequent” recession to appear like the Nice Monetary Disaster, relatively than the extra benign, typical recession of the post-World Battle II period.

To simplify, in an financial system just like the US, there are two sorts of recessions: first, the standard selection; and, second, debt deleveragings. Allow us to be clear right here: there aren’t any good recessions, although recessions are needed evils that cleanse excesses that construct up over time in an financial system. The excellence between the 2 sorts of recessions is vital: the standard selection is wholesome and has a pure cadence, whereas debt deleveragings are damaging and might go away all the financial system “staring into the abyss.”

In our early years at RGAIA, we visited the recession query quite a few instances as folks feared a “double dip,” the European disaster, the power implosion, Fed hikes of 2018 and all the things in between. We’ve got constantly shared a framework that’s particularly vital proper now, for our expectation of what a recession will appear like appears particularly on level proper now.

In our preview for 2015, we stated the next: “Importantly, we expect the following recession will come from an financial system that accelerates an excessive amount of and have to be slowed down through a tightening of financial coverage, relatively than one the place a credit score contraction places us on the precipice of deflation. In different phrases, the following recession will probably be of the run-of-the-mill selection, that are by no means enjoyable, however are far much less troubling than once-in-a-lifetime monetary crises.”

This clarification ought to sound particularly acquainted in mild of latest occasions, with Federal Reserve chairman Jerome Powell evolving his language to now embrace the notion {that a} recession is “actually a chance.” Given the historic nature of “Fed Converse,” actually a chance may as properly translate to “extra seemingly than not,” although Powell continues to insist “we’re not making an attempt to impress…a recession.”

Will we keep away from recession or find yourself in a recession? The reality is that there’s functionally no distinction for the market. Earnings estimates seemingly want to return down in both situation, however the excellent news is that given any recession is sure to be of the standard selection, there is not going to be compelled deleveragings in areas that can completely alter the trajectory of the financial system. How can we are saying this so assuredly? As a result of outdoors of the Federal Authorities, complete debt within the personal sector is at very snug charges, particularly on the family degree.

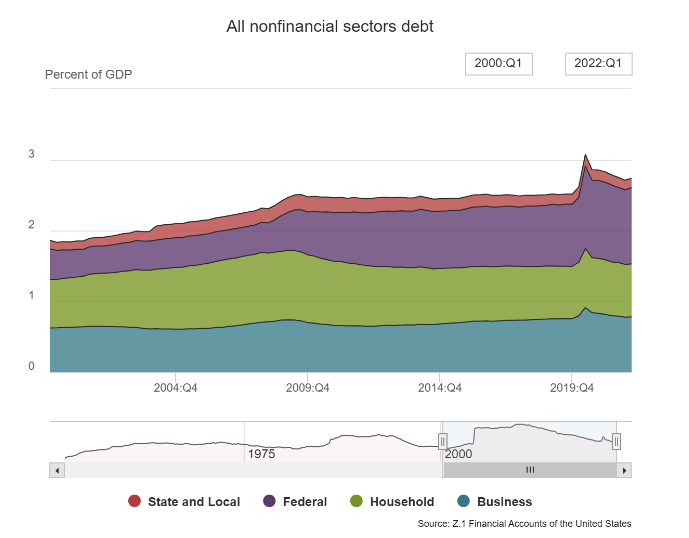

Additional, the monetary sector is as safe-and-sound because it has been in any of our lifetimes. When you recall the Nice Monetary Disaster, it was the monetary sector’s extreme leverage that introduced us to the brink of meltdown. We are able to see the leverage state of affairs fairly clearly within the chart under:

The image would look even higher on a internet foundation, displaying belongings much less debt, although illustrating debt is extra useful for seeing why we ended up with main financial headwinds from debt deleveraging in 2009-2012. Households and the monetary sector (not proven right here) particularly have been the areas that skilled many of the deleveraging. Add within the trajectory of rates of interest and never solely have been debt ranges introduced down meaningfully, so too was the price of the debt in absolute and relative phrases, because the period of debt was prolonged on the low prevailing charges.

This creates a constructive backdrop going ahead. Some may query the extent to which the federal government has levered up, however that’s precisely the position the federal government’s steadiness sheet is meant to play when the personal sector de-levers so as to guarantee the guts of the financial system continues apace. Consequently, going ahead we want households and companies to drive progress, relatively than stimulus. In different phrases, we want a more healthy financial system.

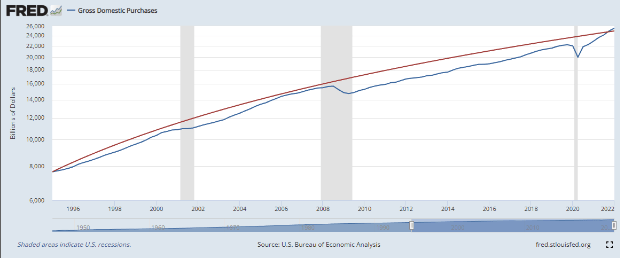

In the identical 2015 preview the place we spoke about what the following recession would appear like, we additionally addressed the query of whether or not we have been experiencing “secular stagnation.” There is likely to be a useful reply to the capability of the personal sector to help the following growth. Beneath we’re Gross Home Purchases (GDP much less exports).

The notch down within the blue line under the purple within the shaded grey space between 2008 and 2010 is what has been referred to as “secular stagnation”–the notion that the capability of the financial system to develop had been decreased by the Nice Recession. With COVID stimulus, the blue line caught again as much as the purple line, and that raises the query whether or not we’d truly not be dealing with “secular stagnation” and additional begging as as to if extra stimulus earlier within the GFC may have prevented our slower progress of the final decade.

Though it’s not possible to show counterfactuals, it’s price eager about whether or not progress from right here can truly be higher than the final decade.

One easy actuality of markets is that when issues get difficult within the financial system, timeframes of the typical investor shorten for numerous causes. We all the time function with a long-term mindset and that strategy is much more advantageous at the moment. In prior paragraphs, we talked about how recessions are an inevitability and one thing we anticipate inside our time-frame in approaching any funding. No firm is completely proof against recessions, however our corporations aren’t the type whose enterprise dimension and alternative will change over the course of a cycle solely by advantage of what occurs in a recession.

Furthermore, our corporations function with a considerable quantity of internet money. As such, the steadiness sheets in our portfolio are a supply of alternative relatively than threat. Leverage can destroy a sound enterprise in a recession if the construction is just too dangerous, in the meantime internet money can be utilized for opportunistic repurchases or strategic M&A that speed up an organization’s progress as soon as the downturn inevitably ends. To present an instance for what we imply: within the 2008 downturn, banks needed to dilute their fairness holders significantly so as to rebuild their steadiness sheets and function going ahead with significantly much less leverage.

These adjustments completely altered the earnings energy of banks. Right this moment, a recession means a short-term reset in expectations each on income and earnings, but it surely doesn’t imply that in some unspecified time in the future over the following 5 years when a traditional surroundings returns, that our corporations’ earnings energy will probably be any much less. That is vital for driving out the storm with conviction.

Macro to micro

With this as a preface, we have to discuss inflation, recession threat and what it means for our shares. As we now have been emphasizing by means of this era of upper inflation, the typical firm in our portfolio predominantly deploys intangible belongings and generates appreciable free money movement, thus rising enter prices by and huge infect our portfolio far lower than they do the S&P at giant. Plus, our common firm boasts appreciable internet money and little to no debt.

That is vital as rates of interest rise, for our portfolio corporations is not going to be uncovered to rising charges of their earnings and price construction. Rising charges do movement by means of when it comes to the low cost price of money flows, however importantly, in our evaluation by means of the 2 prolonged durations of ZIRP, we now have by no means assumed permanence of low charges and have valued corporations based mostly on “normalization” of charges in some unspecified time in the future

That stated, the heightened macro volatility does nonetheless result in issues. The truth that these issues are occurring instantly on the heels of appreciable successes left many caught flat-footed investing behind progress, on the expectation of additional progress, solely to have income sluggish. Investments can’t be reversed instantly and due to this fact a few of these corporations have been left with too bloated a value construction for the fact of at the moment’s surroundings. This isn’t ideally suited, but in addition not catastrophic.

Two of our portfolio corporations, each UK listed small caps, sadly have appreciable publicity to rising prices–Bare Wines (OTCQX:NWINF) and Fever-Tree Drinks (OTCPK:FQVTF).

Bare Wines fell sufferer to a difficult surroundings whereby throughout COVID, stock ranges have been too mild to satisfy demand. The corporate then ordered extra stock that sat in port for too lengthy, so to preempt additional issues, the corporate continued a gentle state of stock acquisition. In the meantime, new buyer acquisition slowed. This left the corporate having invested far an excessive amount of cash in stock and dealing with the powerful alternative of paring again some progress spend or taking an asset-backed mortgage in a tightening credit score surroundings that featured some powerful covenants.

Sadly, we expect the corporate made a mistake in judgment – persevering with to plow forward with their progress plans regardless of the altering and difficult post-Covid surroundings. This left shares susceptible as risk-appetites receded. The silver lining right here is that though shares have taken a beating, the core enterprise continues to function stronger retention of current clients than we ever anticipated, particularly shifting past the COVID interval.

Additional, we expect the corporate is appropriately contemplating the tradeoffs in mild of at the moment’s new realities and will probably be positioned to consolidate their strengths and get well worth in an affordable period of time.

Because it stands at the moment, Bare Wines is valued at lower than the stock on their steadiness sheet. They’re additionally valued at a steep low cost to the runoff worth of their current buyer base. These two methods to strategy liquidation supply a considerable margin of security, as a result of both sharp traders or a strategic purchaser will discover this worth far too compelling to go up for a strategically important asset.

Fever-Tree pre introduced earnings shortly after the tip of the quarter and the market response was abysmal. There had been some issues whether or not the premium value of the product would lead shoppers to commerce down amidst tightening budgets. This was not the case, as revenues continued to exhibit energy. The issue was that inflationary pressures on glass and a decent labor surroundings within the US prevented the corporate from totally launching their US manufacturing plans and realizing anticipated value financial savings.

We expect administration is making the powerful, however prudent option to proceed to serve demand within the US from UK manufacturing, regardless of the near-term hit to margin. The truth that this occurred after a number of quarters of declining gross margins made some traders lose religion in administration; nevertheless, we deeply imagine that these margin pressures will type themselves between supply-chain normalization and actions taken by administration which have to movement by means of.

Way more of the worth over our anticipated holding interval will outcome from how massive the premium mixer enterprise may be than from what level the corporate achieves the optimum margin construction. Instantly following the earnings report, Fever-Tree traded at its lowest ahead multiples ever, on what can be lower than half their historic common margin. Trough multiples on trough margins is a potent recipe for sturdy future returns and we’re not stunned shares have swiftly recovered most of their swoon.

Issues will seemingly stay unstable from right here, however even when the corporate by no means grows once more and margins don’t get well (and allow us to be clear: we anticipate each progress and a margin restoration), the inventory can be as low cost as something within the beverage or spirits trade.

Worth is progress, progress is worth

Though our corporations are typically extra insulated from inflation than most, they have an inclination to reside on the “growthier” finish of the spectrum. In essence, our portfolio corporations in combination make much less free money movement (although nonetheless wholesome quantities of it) at the moment than the S&P, however in addition they develop at a sooner clip. With issues about progress, the market has favored so-called worth shares, whereas punishing these which exhibit progress.

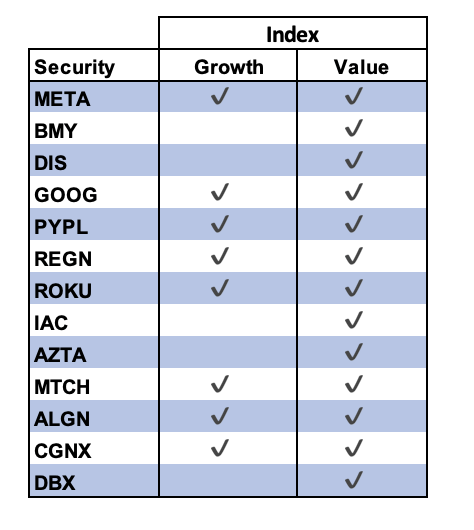

Consequently, many former progress darlings now qualify as “worth” shares to the purpose the place the Russell 1000 Worth Index even contains our progress holdings. An incredible instance of that is one in all our latest purchases: Meta Platforms (META, the corporate previously often called Fb). Because it stands at the moment, META is the fifth largest holding of all within the Russell 1000 Worth Index.

We’ve got all the time self-described as GARP traders, that means we wish to discover progress at an affordable value. Additional, we require progress, reasonableness of valuation and high quality, whereas additionally searching for strategic significance, optionality and some extent of change. We’ve got 22 core holdings at the moment, 5 of which have their major listings on worldwide markets. Of the 17 remaining holdings with US major listings, 13 of them are constituents of the Russell 1000 Worth Index, which represents the universe of huge and mid-cap “worth” shares within the US.

Of these 13 worth constituents, eight additionally seem within the progress index. Actually, at the moment, we now have extra holdings within the “worth” issue than within the “progress” issue, although regardless of this actuality, our portfolio nonetheless trades predominantly with growthier shares. Though this harm us these days, we’re assured the day will come the place shares with sturdy progress and demonstrable worth return to the market’s favor.

Beneath are the 13 holdings within the worth index and their standing within the progress index as properly:

Why are we sharing this? First, as a result of we would like you to know that our portfolios encompass corporations with demonstrable (in distinction to inventive) worth, that clearly checks the established criterion of a scientific worth technique. Second, we discover it extremely attention-grabbing and notable that progress has grow to be worth in at the moment’s market. Over the course of our careers, no such interval has existed the place one can purchase a lot progress at worth costs.

Therein lies each the issue and the chance. The issue is that within the very close to time period, market timeframes are shrinking and whereas progress estimates of those corporations get slashed, few patrons wish to step in; however, the chance is for many who can look by means of to a day when the financial system both avoids or will get previous a recession, the twin forces of progress and worth compounding on each other will result in particularly favorable outcomes.

The chance of at the moment

Allow us to now flip to the fact of bear markets. It’s simple to query each sale not made and each buy. Bear markets put on on traders and provoke self-reflection, introspection and sadly, some extent of doubt.

The reality of the matter is that these are literally the sorts of environments the place the actual returns are made. Timeframes of the typical market participant shrink from years to days. Individuals isolate on the latest datapoint and extrapolate that advert finitum. To an extent, this sort of over-extrapolation has been in place from the second the COVID crash began, however at the moment we’re at a juncture the place extending one’s timeframe is an important method to inevitably reap stable long-term returns.

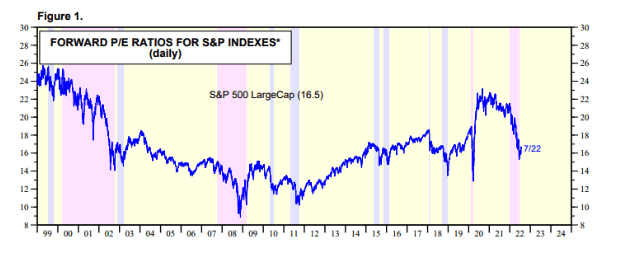

We’ve got all the time operated with a long-term mindset. On what is likely to be the eve of recession, with markets already down considerably, it’s that rather more vital to consider what the world seems like on the opposite facet (ie post-recession) than in it. The exception is with these corporations whose steadiness sheets provoke issues about their means to outlive an hostile surroundings. There’s this widespread saying proper now: “the market has repriced the a number of, now we now have to cost the correct “E” for earnings.”

It’s been asserted by many and it sounds interesting, however we strongly disagree with the premise. We might phrase it as such: “the market has repriced the a number of BECAUSE it doesn’t belief the E.”

Right here is the way it seems as of at the moment, with the repricing much more acute in smaller capitalization shares:

supply: Inventory Market Briefing: Chosen P/E Ratios

Those that proffer this argument in regards to the subsequent leg reflecting earnings threat counsel the a number of has repriced as a result of the risk-free price has moved greater for the reason that begin of the 12 months. That is true and we might be remiss to not settle for that some portion of a number of compression stems from the rise within the 10-year particularly, however the repricing available in the market’s a number of has been extra excessive than what can be justified by the 10-year alone and the market’s a number of is now decrease than it was when the 10-year was at comparable ranges earlier than COVID.

Multiples and earnings are inherently tied on the hip. One would pay a better a number of for extra progress. When progress estimates come down, so too does the a number of. We imagine our argument is appropriate for 2 major causes: 1) the “repricing of threat” began within the growthier COVID beneficiaries lengthy earlier than the 10-year commenced its ascent. This space of the market began feeling ache when it turned clear progress charges had peaked and there was little readability on both the magnitude or size for the way the expansion curve would decelerate.

Thus far, this pocket of the market has skilled essentially the most dramatic a number of compression of all of them; and, 2) a number of the most excessive down strikes have occurred on earnings disappointments themselves over the previous two quarters. That is true of particular shares and the market. On the very least, earnings have been a considerable a part of the repricing right here.

Latest market actions

Early within the second quarter, we offered our Twitter (TWTR) shares on the official announcement that Elon Musk would purchase the corporate at $54.20 per share. Though we usually would anticipate what was then a big 7% merger/arb unfold to shut, we figured on this market surroundings it will be useful to maneuver apart within the occasion future drama may ensue whereas constructing money so as to opportunistically deploy into higher alternatives. In the course of the quarter, we noticed the prospect to take action and purchased shares in 4 corporations.

Within the course of, we’re additionally broadening our portfolios and diversifying into extra concepts. There’s a tradeoff between focus and diversification, however in instances like these when the market is throwing many shares out of the window (or “infants out with bathwater” because the saying goes), broadening the aperture of alternative is a worthwhile endeavor. The extra positions we now have that match our standards, the extra possibilities we now have for one thing to go proper for us and the much less anybody threat issue can additional harm the portfolio. We are going to briefly cowl every within the following paragraphs.

Meta Platforms, Inc (META) f/okay/a Fb— we adopted Fb for years and have been typically requested “why personal Twitter when you should buy Fb?” Certain sufficient, Twitter’s return was much better over our holding interval and we now deployed an honest portion of our Twitter proceeds into META. META at the moment strikes us as one of many most cost-effective shares in all the market and one of many extra attention-grabbing setups we now have seen. META was hit with a triple-whammy of powerful COVID comps, adjustments in Apple’s privateness insurance policies and rising competitors from TikTok.

Regardless of all this, the corporate continues to develop, albeit at slower charges. At its lows this 12 months, META was buying and selling for a low teenagers ahead P/E (15x 2022 numbers at the moment) and that is regardless of investments within the Actuality Labs division at round a $10b annualized price. If we exclude the Actuality Labs investments, the core META properties of Fb, Instagram and WhatsApp would earn someplace round 23% extra in backside line EPS. This might chop about 2.5 turns off the corporate’s P/E.

Talking realistically, there isn’t a signal Mark Zuckerberg would completely cease these investments; nevertheless, we do suppose Zuckerberg is life like about his inventory value and really properly may defer a big portion of the funding till core earnings reaccelerate. Additional, we expect it’s applicable to worth the corporate on a sum of the elements foundation and relatively than totally expense the Actuality Labs investments towards the core properties, we must always take into consideration what the precise worth of that funding may yield. Both approach, even totally expensing Actuality Labs, this firm is way too low cost to disregard.

Align Expertise (ALGN)– we now have adopted Align with admiration for years. The corporate has constantly executed its mixture of worthwhile progress, whereas disrupting the orthodontics trade and enhancing its providing past the pure product. Particularly, Align’s Invisalign is by far the perfect clear aligner and the corporate has used its providing to construct what is basically the “working system” foran orthodontics apply. COVID Stimulus led to a surge in demand from which there’s now a hangover.

Consequently Align is at its lowest valuation a number of in a decade (sub 15x EV/EBITDA); decrease than when fears of a patent expiration led some to imagine emergent competitors may derail Align’s momentum (it didn’t). Align is extra “discretionary” than the everyday healthcare firm, as a result of their core clientele are grownup sufferers with orthodontic issues. This implies there’s some portion of cyclicality; nevertheless, the actually long-term alternative is capturing the core teenager orthodontic trade, which stays the overwhelming majority (over 80%) handled with steel braces.

It’s inherently tougher to drive adoption on this demographic contemplating invisible aligners are costlier and require affected person compliance, although we expect the era rising up seeing themselves on Instagram and TikTok will inevitably steer in the direction of clear, the place Align is dominant. As they are saying, the long run right here is shiny.

Cytek Biosciences, Inc (CTKB)– Cytek is a type of corporations we expect may find yourself a real present from this surroundings. The corporate went public in 2021 and raised appreciable capital as a result of enthusiasm of the chance for Cytek to essentially change movement cytometry–a important piece of organic analysis and diagnostics to research cells or particles. Move cytometers are in all places, although we don’t typically hear about them.

Quick ahead to at the moment and Cytek’s shares have collapsed from the IPO value, regardless of the corporate being free money movement optimistic and holding 30% of its market cap in internet money ($362 million). The corporate’s proprietary know-how changed costly vacuum tubes with less expensive avalanche photodiodes, which permits for each greater precision, sooner throughput and most significantly decrease value of possession and operation. What clients don’t need higher high quality at a lower cost?

Competitors shouldn’t be even shut. Cytek sells movement cytometers, however importantly they’re now constructing a reagent enterprise to enhance their instrument. This implies they may have a razor blade and enterprise mannequin, promoting the instrument with a pleasant revenue margin and the reagents for throughput at an excellent higher margin. Regardless of appreciable progress investments, the corporate is worthwhile (on an adjusted EBITDA and money movement foundation) at the moment and will probably be much more so sooner or later.

MacCyte, Inc. (MXCT)– Cell and gene therapies are the frontier of innovation in biotech. MaxCyte is uniquely properly positioned to profit, regardless of who the exact winners are, as a decide and shovel supplier to the trade. MaxCyte develops and sells electroporation devices, that possess “unparalleled consistency and minimal cell disturbance.” Like Cytek, Maxcyte boasts a razor and blade enterprise mannequin, with excessive gross margins on each the instrument and consumable piece.

The instrument is mission important to edit the DNA of a cell outdoors of the physique and it can’t be used with out MaxCyte’s proprietary consumables. In analysis, clients use a single instrument, however as a research strikes to the formal FDA scientific course of extra devices are deployed and on an approval down the road, much more. Past the razor and blade income swimming pools, MaxCyte’s instruments are so helpful that their clients signal on for “Strategic Platform License” (or “SPLs”) preparations.

SPLs supply MaxCyte licensing revenues as milestones are achieved and a p.c of revenues as soon as a remedy is authorised to be used. The corporate is partnered with 17 main cell and gene remedy corporations for these SPLs. Not solely would a single approval from one in all their 95+ accomplice packages justify the present valuation, however considerably a couple of approval is believable.

On high of this, we bought MaxCyte at a value the place over half of their market cap is pure money and at their current price of burn, the corporate has over a decade of money wants coated. As such, the market is giving little or no credit score to a top quality enterprise mannequin with distinctive optionality.

The excessive value of an vital lesson

Whereas this surroundings has not been conducive to investing in equities, we’re fairly annoyed with our personal relative efficiency. Regardless of a difficult macro surroundings, we view our predisposition in the direction of inaction in our greatest concepts as a failure of our personal making. This tendency has served us properly for nearly everything of the final decade and it has value us mightily of late.

We should ask ourselves: ought to we revisit our low turnover goal or is there one thing else underlying at the moment’s predicament that may assist us navigate comparable environments sooner or later? We ask these questions as a result of it’s how we’re wired and since we all know we are able to do higher.

One of many traits on the core of what we do at RGA is to continually study, develop and advance. Our choice is to study from historical past books; nevertheless, inevitably some errors we should make on our personal so as to internalize and synthesize the correct lesson. An unlucky actuality with markets is that there aren’t any second possibilities to make up for previous errors, although the sweetness is that in pursuing investing as a lifelong endeavor there are an infinite variety of alternatives to deploy previous learnings down the road. Not solely can we do higher, we completely will do higher.

Wanting backwards, we are able to establish two distinct issues:

- Within the rebound from the COVID crash, our portfolio concentrated itself right into a sure type of place. This was not an express endeavor on our half, actually, we felt the portfolio was pretty barbelled between COVID losers and COVID winners. Because the winners soared in tandem and the losers stagnated, nearly all of our e book consisted of corporations sharing two important traits: excessive progress and a digital-first providing. Previously, we now have skilled epochs of time the place our portfolio holds one or two giant winners. From the start, we now have had a self-calibrating process, whereby our position-size ceiling would require a sale, even when we nonetheless believed within the worth and prospects of the enterprise.

- In 2020 by means of early 2021, with a lot of our portfolio shifting in tandem, just one place reached our dimension restraints and that one, we did certainly trim. This led to a big realized capital achieve and prompted us to imagine we had extra time to steadily scale out of some COVID winners so as to as soon as once more personal a extra balanced portfolio.

Half one displays how we lacked a self-calibrating course of when a big a part of our portfolio functionally turns into one commerce. This ties in with half two, which is the behavioral actuality of the state of affairs. The aim of automated constraints is to take some extent of decision-making away from choices which may get clouded by judgment name. One irritating actuality of this current state of affairs is how we acknowledged the diploma of over-concentration in a sure type of inventory.

We began the method of steadily paring again winners and reallocating to newer areas; nevertheless, we felt there was time to unfold the inevitable tax hit over years relatively than notice all the things instantly. There’s a diploma to which we’re not sure the occasions which have transpired during the last two years will ever reappear, however we’re within the means of contemplating what the suitable constraints must be. What is not going to change is that we very a lot imagine over the long term, letting winners journey is important to distinctive outcomes and letting corporations intrinsically compound is important for optimizing after-tax outcomes.

We do know one thing vital that will probably be completely different in our portfolio administration course of from right here: we pays extra consideration to the correlations between the positions in our portfolio and when an uncomfortable quantity of our portfolio is appearing functionally as one commerce and retains taking over an outsized share of our portfolio, we will probably be deliberate in paring again publicity. Over time, we are going to extra clearly articulate what this seems like, however for now it’s a rule that features one thing that’s goal, utilized with a level of subjectivity.

Thanks to your belief and confidence, and for choosing us to be your advisor of alternative. Please name us straight to debate this commentary in additional element – we’re all the time completely satisfied to deal with any particular questions you could have. You may attain Jason or Elliot straight at 516-665-1945.

Heat private regards,

Jason Gilbert, Managing Associate, President | Elliot Turner, CFA, Managing Associate, Chief Funding Officer

Editor’s Notice: The abstract bullets for this text have been chosen by Looking for Alpha editors.

[ad_2]

Supply hyperlink