")

[ad_1]

Chaay_Tee/iStock through Getty Pictures

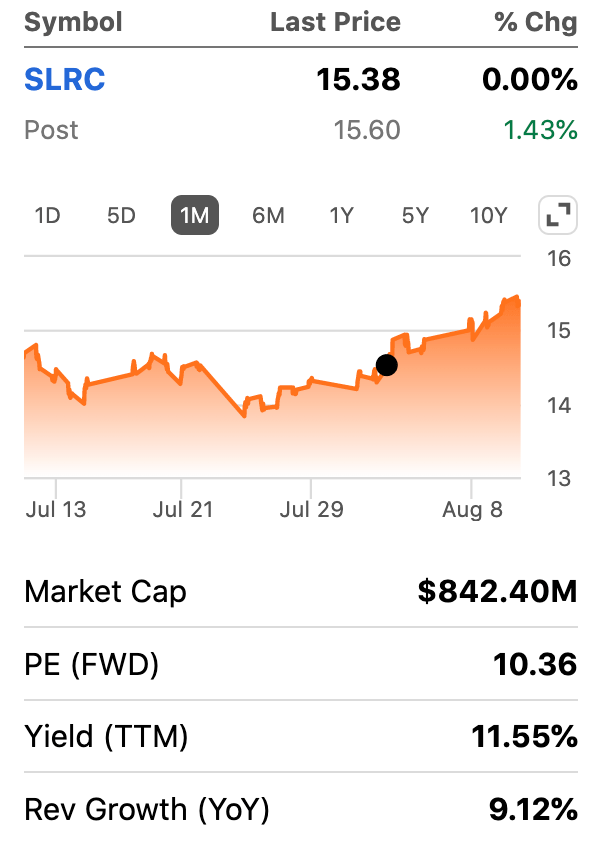

That is our third article this 12 months for Searching for Alpha on enterprise improvement firms (“BDCs”). SLR Funding Corp. (NASDAQ:SLRC) could be a possible alternative, however we’re skittish following the discharge of its Q2 ’22 monetary report two weeks in the past. SLRC shares moved up nearly a greenback since then and appear to have momentum once more.

Value Chart SLRC (seekingalpha.com)

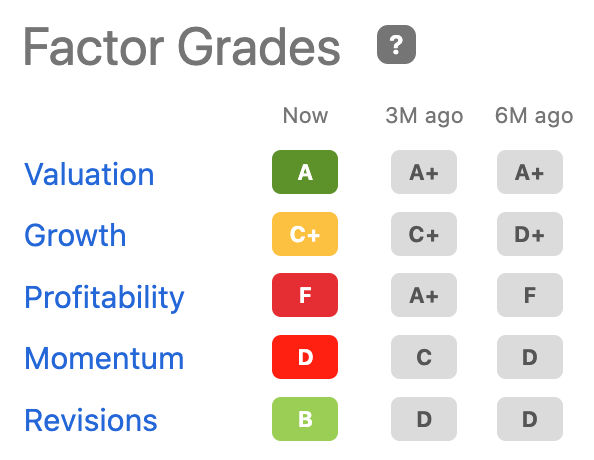

Searching for Alpha’s Quant Ranking for all three BDCs, SLR, Goldman Sachs BDC (GSBD), and Capital Southwest (CSWC), are a maintain, tiptoeing into the buy-side of the ranking. CSWC shares are up ~$2 per share since early June. GSBD shares are up ~$1 since our article. The tone of our articles was constructive in regards to the different two firms as a result of they’re worthwhile. We’re much less bullish about SLRC as a result of it sports activities weak Issue Grades and “maintain” suggestions from S A authors, Wall Avenue analysts, and the S A Quant Ranking:

Issue Grades (seekingalpha.com)

Snapshot

SLR Funding Corp. specializes in making secured and unsecured lending investments throughout a diversified subject of industries and for a number of functions. Investments are between $5 million and $100 million. The fund invests in firms with revenues between $50 million and $1 billion and EBITDA between $15 million and $100 million. It makes senior secured loans, and mezzanine loans, and accepts fairness securities. SLR Funding typically makes investments in thinly traded public firms. The fund makes non-control fairness investments.

SLRC shares are usually not risky. Their Beta charges at 0.32, effectively under one for market actions. We do not anticipate any occasions that may fortuitously transfer the share value. The typical value goal we count on will meander between $15 and $17 over the subsequent 12 months. Shares are overvalued and are driving the market uptick. The share value would possibly slip to $13 per historic multiples, previous returns, development, and forecasts.

A latest main announcement by the corporate is it revised its intent “to make month-to-month distributions to stockholders as an alternative of quarterly distributions.” This announcement follows a merger with SLR Senior Funding Corp this previous April. The mixed firm has property of ~$2.6B and about $1.1B whole web property. Primarily, the merger was to streamline funding alternatives, reduce working bills, and heighten synergies.

Funding Highlights

SLR Funding’s web funding earnings for Q2 ’22 is reportedly 37 cents per share equal to final 12 months. It beat estimates for the straight fourth quarter that this time forecast EPS at $0.34. SLR Funding additionally beat income estimates. We count on the EPS for Q3 would be the identical or a penny larger, because the financial system improves. SLRC shares are down +20% for the 12 months and +28% over the previous 5 years. The profit to retail worth traders, like with comparable BDC shares, lies within the dividend (TTM) yield at 11.55%. The P/E ratio is 73.24. Quick curiosity is nil.

The corporate holds a $2.7B funding portfolio that features ~780 firms. It made $274.8M in investments in Q2. Internet funding earnings was $20.3M. Because the merger, we forecast an annual earnings development of 140%. Income on the shut of the primary week in August is touching $200M for the 12 months; earnings are $86.5M.

Two Warnings

The corporate took a one-off lack of $58.4M that straight lowered monetary outcomes and drove the inventory all the way down to a 52-week low of $13.75. Final 12 months, the revenue margin peaked at 58.4%; the final report had it at 3.7%.

The corporate’s web debt-to-equity ratio is a excessive 61% from about 33%. Working money stream is unfavorable, and EBIT doesn’t cowl curiosity funds.

On the intense aspect, the typical supervisor’s tenure is over 14 years. These seasoned professionals maintain a wholesome 2.5% stake within the firm. Personal firms personal lower than 4% of the shares whereas establishments personal solely 40%. The rest, 53% to 54%, are held by the general public. The CEO and founder upped his holdings by 214%.

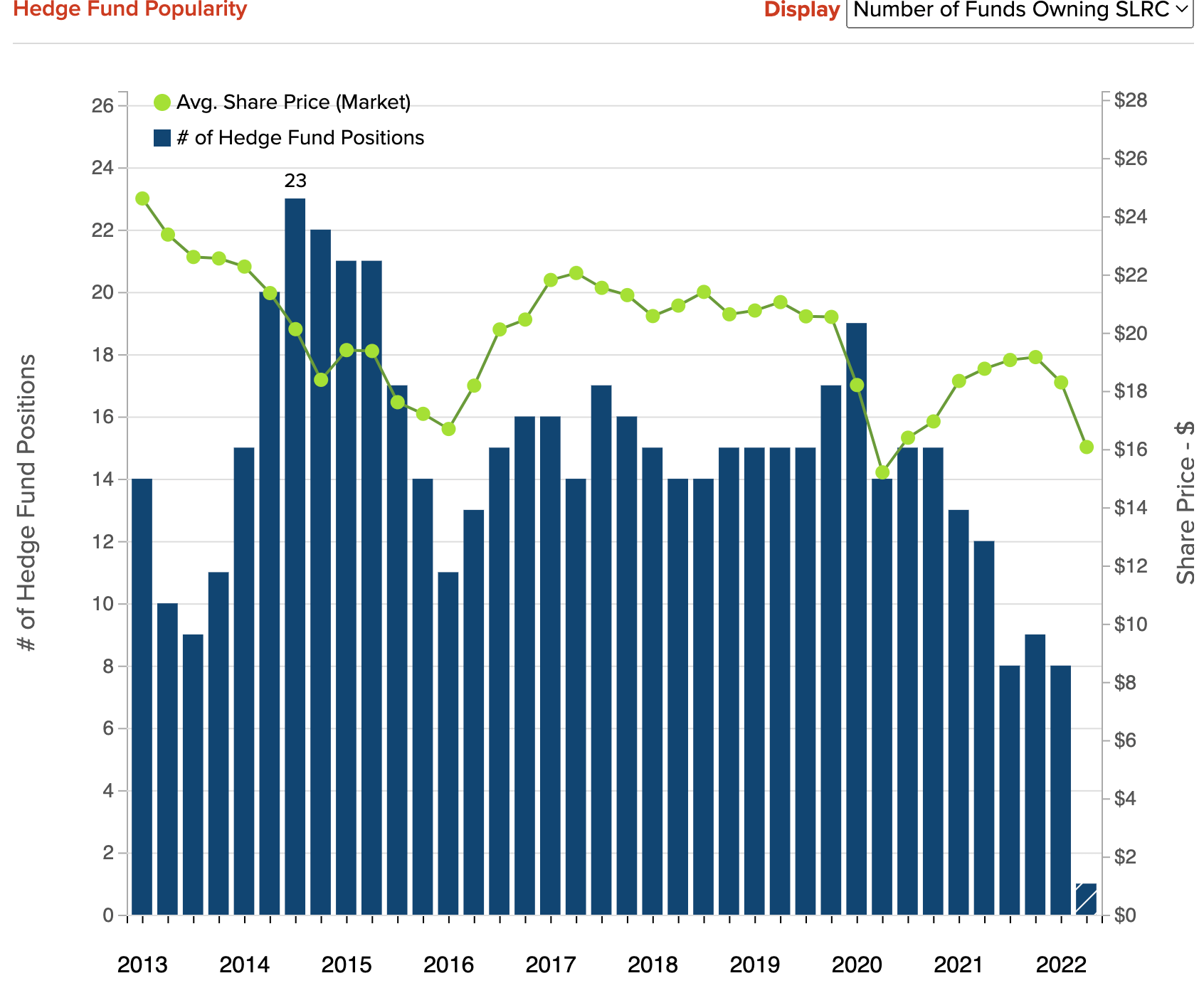

Within the final quarter, hedge funds elevated their holdings by 272.5K shares however there aren’t any beamish portents suggesting this shall be a development in 2022.

Hedge Funds in SLRC (insidermonkey.com)

Higher Do not Commit

We imagine the downsides and uncertainties dealing with SLR Funding depart us flummoxed and unable to do greater than suggest holding shares. The dividend yield is sweet, however different BDCs are extra strong and worthwhile. Time could flip this round. This firm has weaker monetary power and profitability than others. We doubt important development is within the playing cards. The merger sparked momentum, however debt could be overwhelming. The subsequent earnings report date is November 3, 2022. For now, higher do not commit.

[ad_2]

Supply hyperlink