")

[ad_1]

Евгений Харитонов/iStock through Getty Pictures

Firm Profile and Alternative

Tellurian Inc. (NYSE:TELL) is an built-in LNG (Liquefied Pure Fuel) producer. TELL owns, develops, and produces its personal pure gasoline, which comes from the close by Haynesville Shale, which has a few of the least expensive pure gasoline on the earth. TELL is constructing Driftwood LNG, a liquefaction facility, which converts pure gasoline into LNG by freezing and compressing it 600 instances. Tellurian’s forthcoming LNG manufacturing shall be placed on a ship FOB (Free On Board) and bought elsewhere on the earth the place costs are a lot larger. The value distinction in the present day between worldwide LNG and US home pure gasoline (Henry Hub) is close to historic highs because of poor European vitality coverage and the Russian invasion within the Ukraine. On August 25th, 2022, the home Henry Hub worth was $9.375/mmBTU, the European “TTF” benchmark was $94.196/mmBTU, and the Asian Japan Korean Marker “JKM” was $69.995/mmBTU. Tellurian’s Driftwood challenge ought to generate billions in cashflow when it’s constructed and working in 2026.

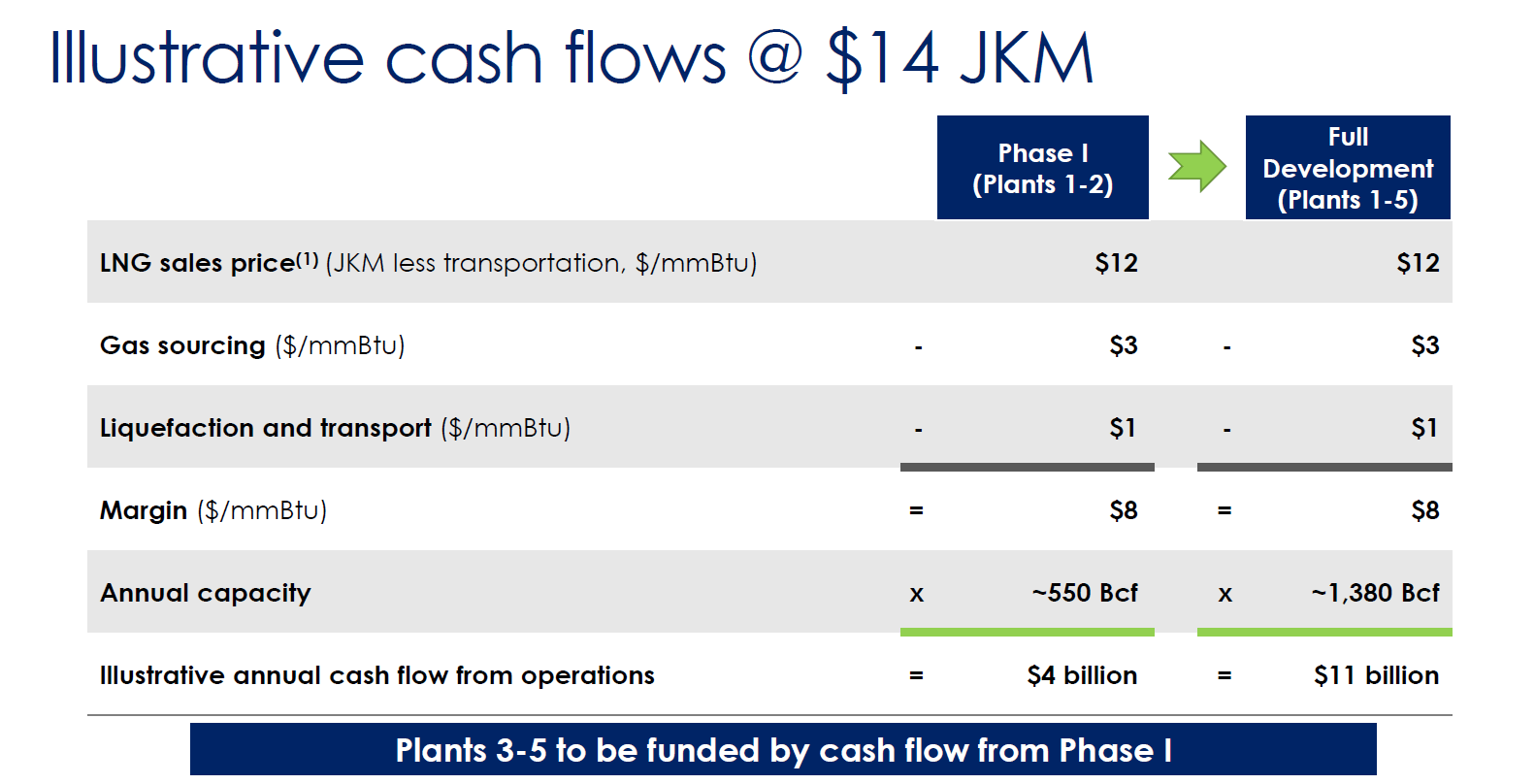

Beneath is an illustration, from the corporate’s most up-to-date investor presentation, that reveals about $Four bn in money movement per yr when Section 1 (2 trains) is full; and, when totally constructed with Section 2 full (all 5 trains), Driftwood ought to generate about $11bn in money movement per yr.

estimated money flows (Tellurian Inc. Investor Deck Aug 2022)

The challenge timing based mostly on Souki’s Cheniere expertise is 40-44 months from April 2022, which was when Driftwood’s building with Bechtel commenced. This means a completion date of September to December 2025.

Charif Souki is Tellurian’s Government Chairman. Souki is a pioneer within the LNG trade; he was co-founder and Co-CEO of Cheniere Vitality, the biggest LNG export firm within the US. Tellurian’s staff “originated and executed c. 79% of U.S. LNG capability growth and c. 36% of world LNG capability growth throughout 4 continents.” Tellurian’s mannequin is transformative; its built-in mannequin seeks to seize the US versus worldwide pure gasoline worth unfold quite than function as a toll highway course of supplier. Tellurian has “all FERC and DOE permits secured for Driftwood LNG terminal and pipelines.”

Tellurian’s high-octane mannequin requires $12.Eight bn which it expects to boost by 2/Three debt and 1/Three fairness. This can be a troublesome process, however Souki’s background as an funding banker, profitable entrepreneur, and Co-Founding father of Cheniere makes him a seasoned government and profitable LNG financier. As one vitality banker stated, “If anybody can do it, Souki can.” Not all are satisfied.

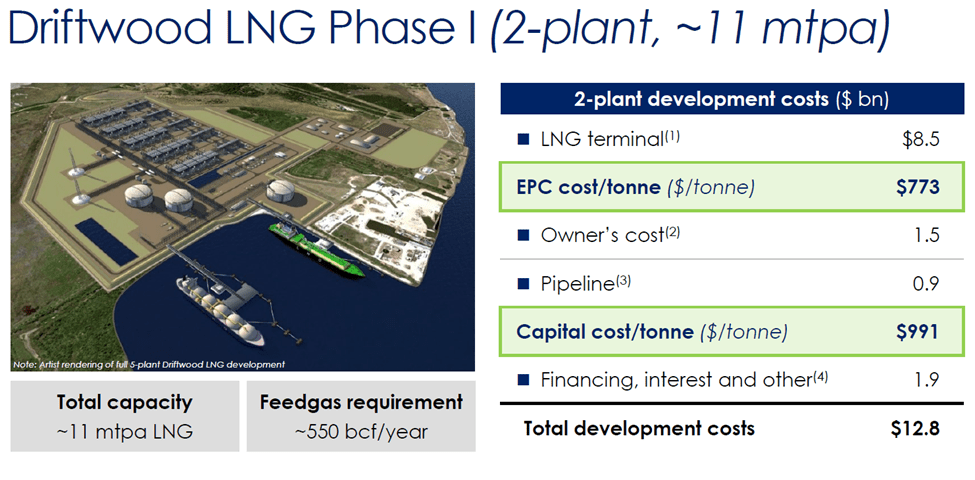

The illustration under reveals the positioning and prices for Driftwood LNG Section 1 facility. As soon as Section 1 is accomplished, Tellurian seems to be to fund Section 2 (trains 3, 4, and 5) out of money movement produced by Section 1.

Tellurian’s estimated money flows for 2 and 5 trains. (Tellurian August 2022 deck)

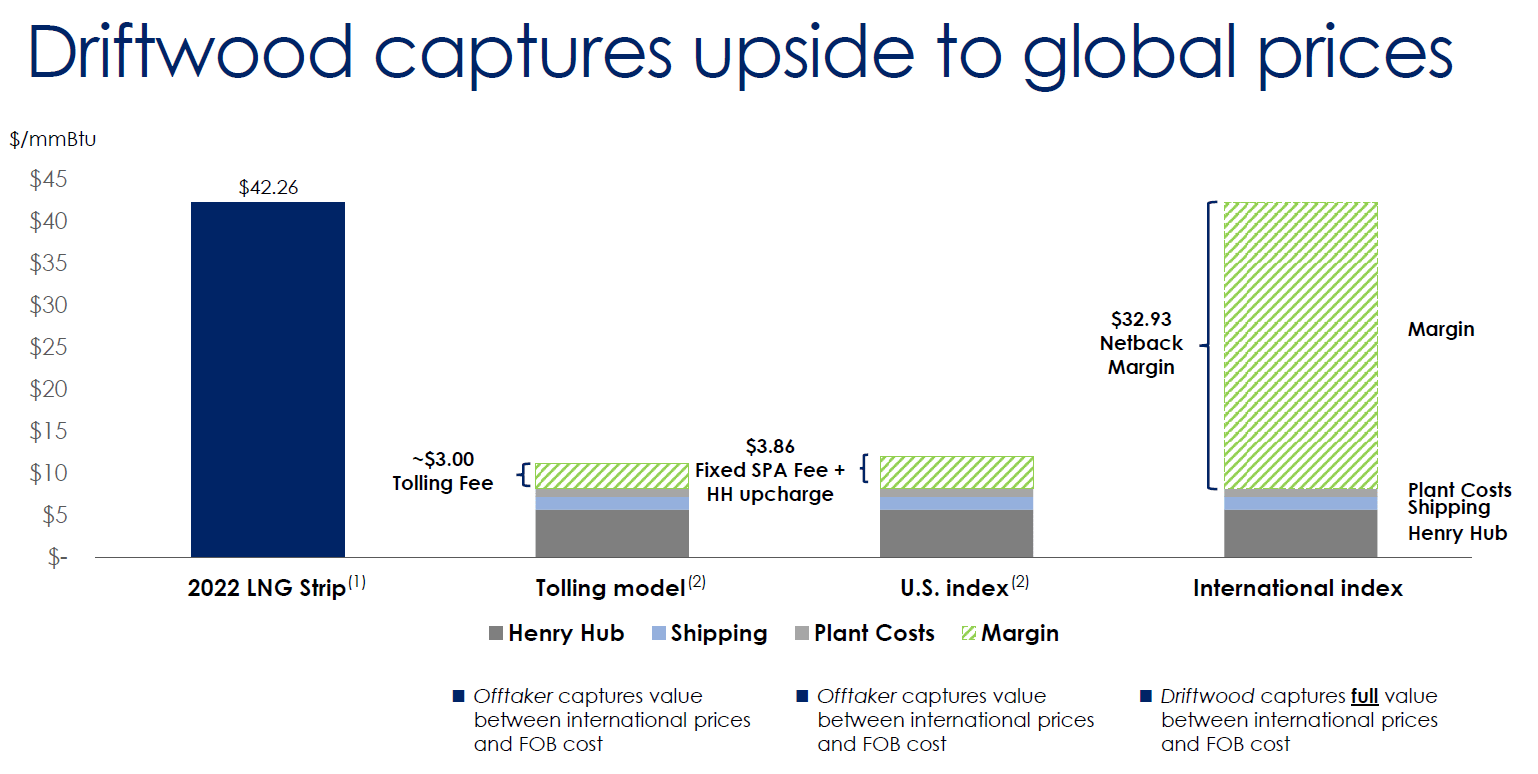

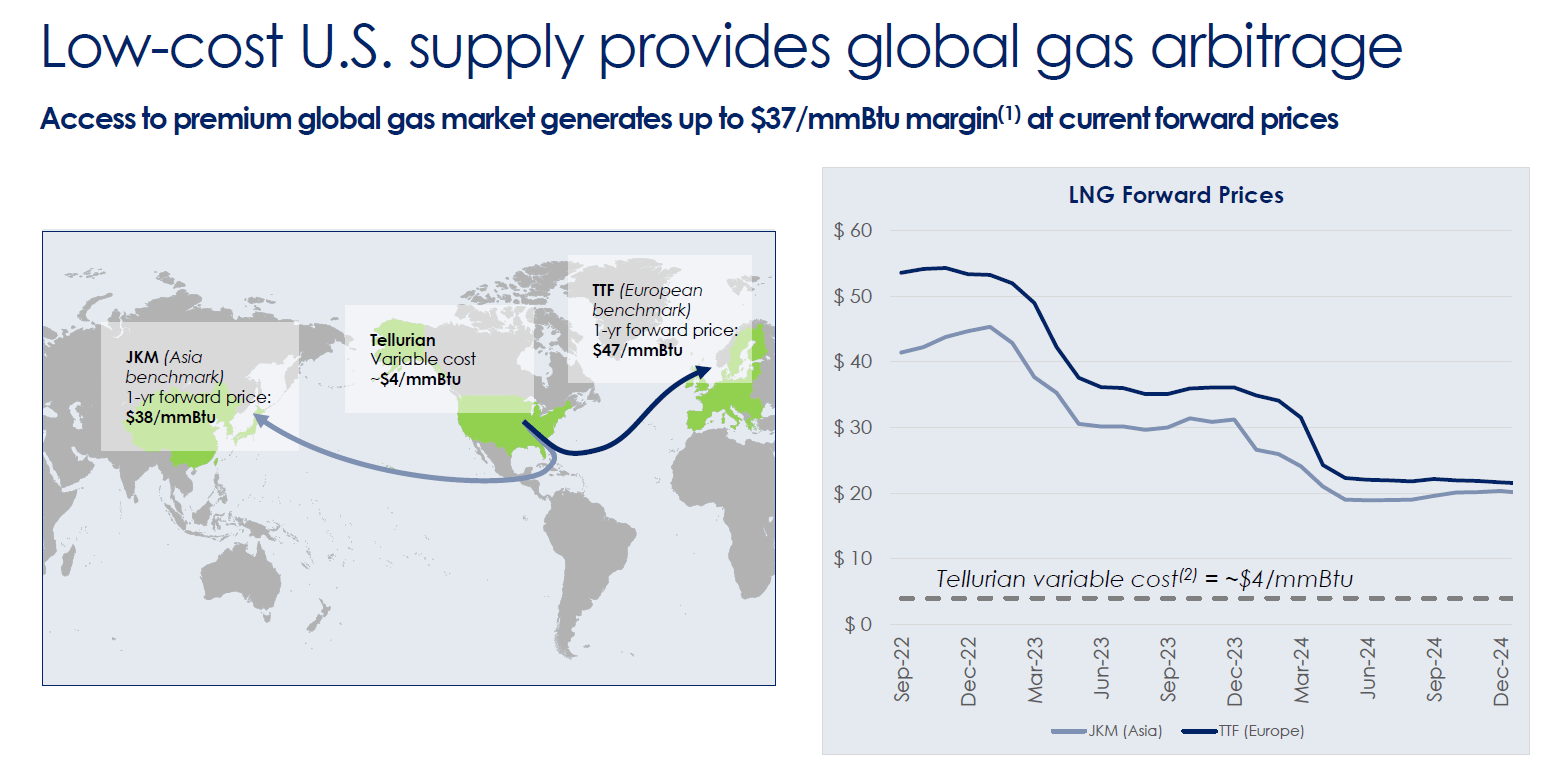

Attributable to Russia’s invasion of Ukraine and in the present day’s vitality disaster, which is particularly extreme in Europe, in the present day’s $32.93/mmBTU Netback Margin (see chart under) is almost 4 instances the $8/mmBTU Tellurian has projected within the first chart which estimates $Four bn cashflow from Section 1 and $11 bn cashflow from Section 2. Tellurian’s funding prospects are aided partially by the Biden Administration’s dedication to ship 50 BCF/yr to Europe by 2030 to switch Russian pure gasoline.

margin illustration (Tellurian Investor Deck)

As a result of Tellurian’s Driftwood LNG is a excessive threat and excessive return challenge and because of latest years’ vitality market volatility, TELL inventory has been fairly risky. Charif Souki places his cash the place his mouth is. He personally skilled margin calls within the 2020 COVID-19 market crash. Tellurian’s administration owns 20% of Tellurian’s inventory, so shareholders’ pursuits are aligned with administration.

two yr chart (Two Yr Tellurian Chart Yahoo Finance)

The Pure Fuel and LNG Market

The world has embraced local weather change and UN Sustainable Growth Objectives and has sought to transition from fossil fuels to renewables like wind and photo voltaic. Sadly, this technique and these objectives haven’t been deployed uniformly and with restricted success. In truth, earlier than the February 24th Russian invasion of Ukraine, Europe was already engulfed in an vitality disaster. Consequently, final yr, Europe modified coverage and proposed each LNG and nuclear as “transition fuels” to offer the wanted vitality for fundamental utilities at an inexpensive worth whereas the transition performs out over the a long time forward.

The vitality disaster is international and never simply European. Europe and North America get pleasure from excessive requirements of residing, however a lot of the remainder of the world wants extra vitality for his or her economies to develop and converge towards our excessive requirements of residing. 3.5 billion individuals globally don’t get pleasure from steady electrical energy. With UN Sustainability Purpose #1 to finish poverty and #2 to finish starvation, there shall be large calls for for vitality sooner or later and pure gasoline seems to be to be probably the most compelling vitality supply throughout the vitality transition of the approaching a long time.

The illustration under reveals how low-cost US pure gasoline can present the world with wanted vitality and emit half the carbon emissions of coal and oil. The diagram on the proper reveals how the ahead contracts level to decrease future LNG costs which are comfortably larger than our first illustration that confirmed a $8/mmBTU margin producing $Four bn in money movement per yr.

LNG supply routes (Tellurian Investor Deck)

Radical Decarbonization with Fossil Gasoline Pure Fuel

One other highly effective case for secular pure gasoline progress is made by the biggest pure gasoline producer within the US, EQT Company. EQT argues compellingly that if we merely change all of the worldwide coal manufacturing with pure gasoline, we might hit the decarbonization objectives nicely forward of 2050! A lot of the worldwide carbon emissions come from China and India which burn huge quantities of coal. If all worldwide coal manufacturing was changed with LNG, the world would hit our local weather objectives quicker and with out the devastating vitality price inflation plaguing the world.

The chart under particulars the LNG worldwide coal alternative technique advocated by EQT and others. This underscores the significance of LNG to the vitality transition and the scale of the addressable market.

LNG routes globally (EQT Company)

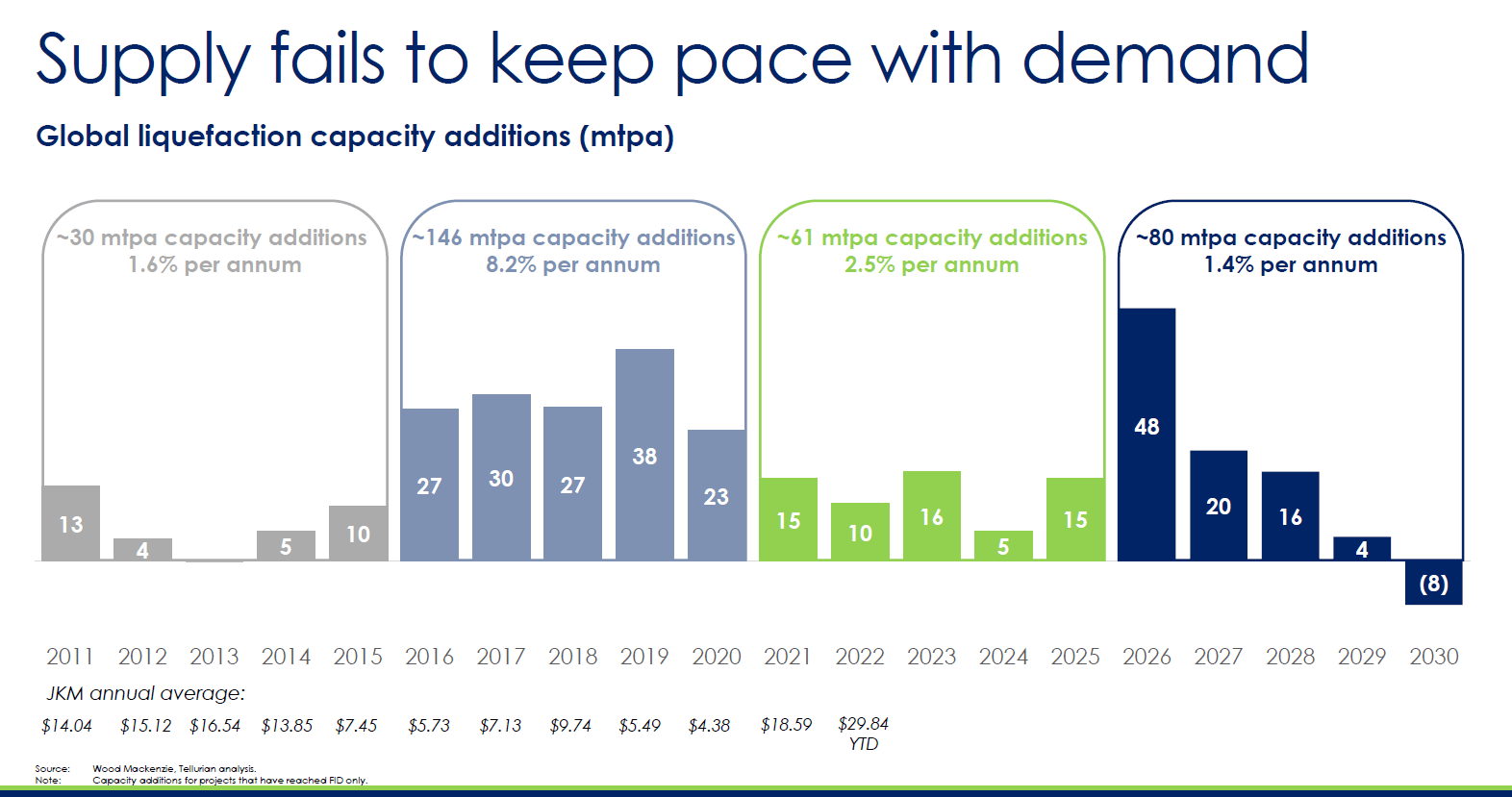

At present, the worldwide liquefaction capability progress projections counsel the market is early in its progress cycle. Additional, the chart under reveals that projected LNG manufacturing capability is inadequate to fulfill future wants. The shortage of latest LNG tasks means that future costs are usually not liable to over-capacity.

LNG’s historic and deliberate capability progress (Tellurian Investor Presentation 8.2022)

Valuation and Souki Historical past:

Tellurian Inc.’s market cap is $2.56 billion, in the present day, and share worth $4.50. As of 6/30/2022, Tellurian’s widespread fairness was $653 million and money $823 million, so little of Driftwood LNG’s worth is being attributed to Tellurian’s market capitalization.

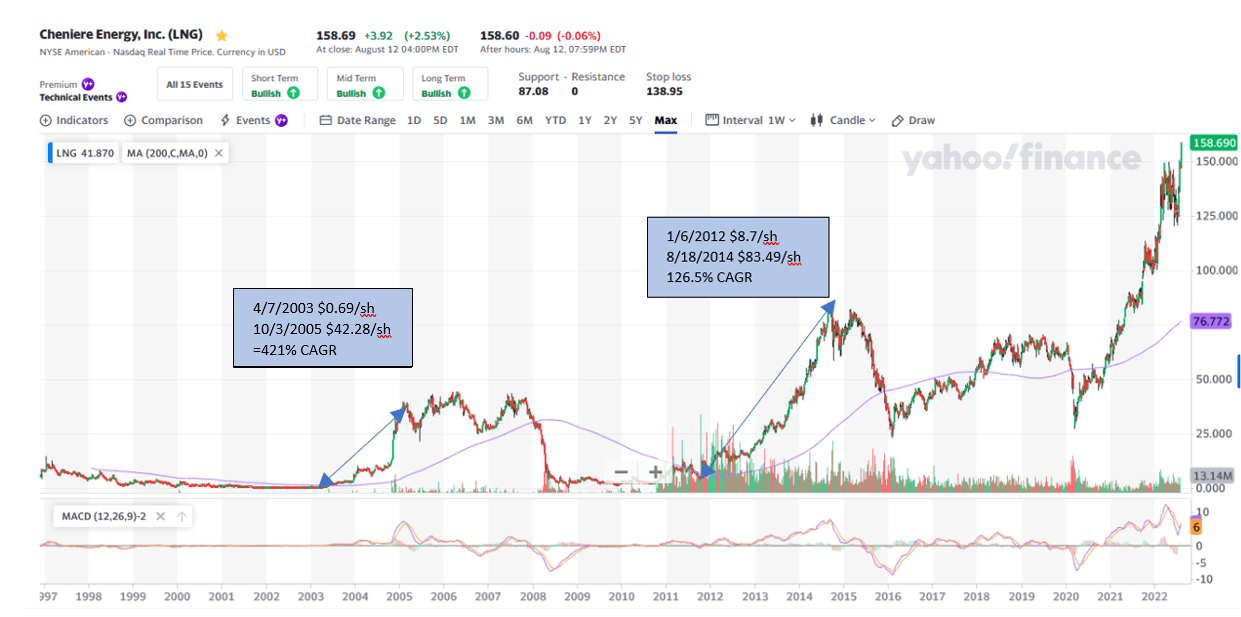

When Cheniere’s (LNG) long-term inventory chart, we observe that the Cheniere’s shares skilled their most fast progress throughout the finance and building intervals. For instance, Cheniere’s first challenge was a gasification facility when the corporate was importing LNG and gasifying it. Throughout that interval, 2003-2005, Cheniere’s inventory appreciated at 421% CAGR. Secondly throughout 2011-2014, Cheniere’s inventory appreciated at 126.5% CAGR when Cheniere was constructing its first liquefaction facility and the corporate restructured to turn into a LNG producer and LNG exporter.

Consequently, we consider this financing interval for Tellurian traders shall be as crucial as was the case with Cheniere when it went by its financing and building intervals in 2003-2005 and 2011-2014. Because the prospects for financing turn into a actuality and the corporate turns into totally financed, Tellurian shares might admire at equally abnormally excessive charges, if the corporate efficiently funds Driftwood LNG.

The chart under of Cheniere Vitality, Inc. spotlight the intervals of surprising appreciation.

Finance and Development interval efficiency for Cheniere (Yahoo Finance IGA analysis)

Charif Souki and Tellurian Inc. have seen wild swings. When Cheniere constructed its first facility, the plant was a degasification plant based mostly upon excessive home US pure gasoline costs and low worldwide gasoline costs. Within the early 2000s, as fracking grew to become widespread, the invention of plentiful related pure gasoline in US shales modified the enterprise proposition for Cheniere. This game-changing US pure gasoline discovery rapidly reversed the financial proposition for importing LNG. From January 2008 to November 2009, Cheniere’s shares plunged from $32.07/share to $1.78/share – a 94.5% decline in underneath two years.

Souki then restructured and redesigned Cheniere to transform low-cost US pure gasoline into LNG. This was an incredible problem as a result of whereas Cheniere was initially profitable, Souki needed to persuade his traders to reinvest within the huge new liquefaction facility. Souki succeeded with this monumental problem. Cheniere’s inventory took off once more rising to $83.59/share, from a low of $1.87 in 2009, earlier than Charif Souki left the board in December 2015 because of a board struggle with famend shareholder activist Carl Icahn.

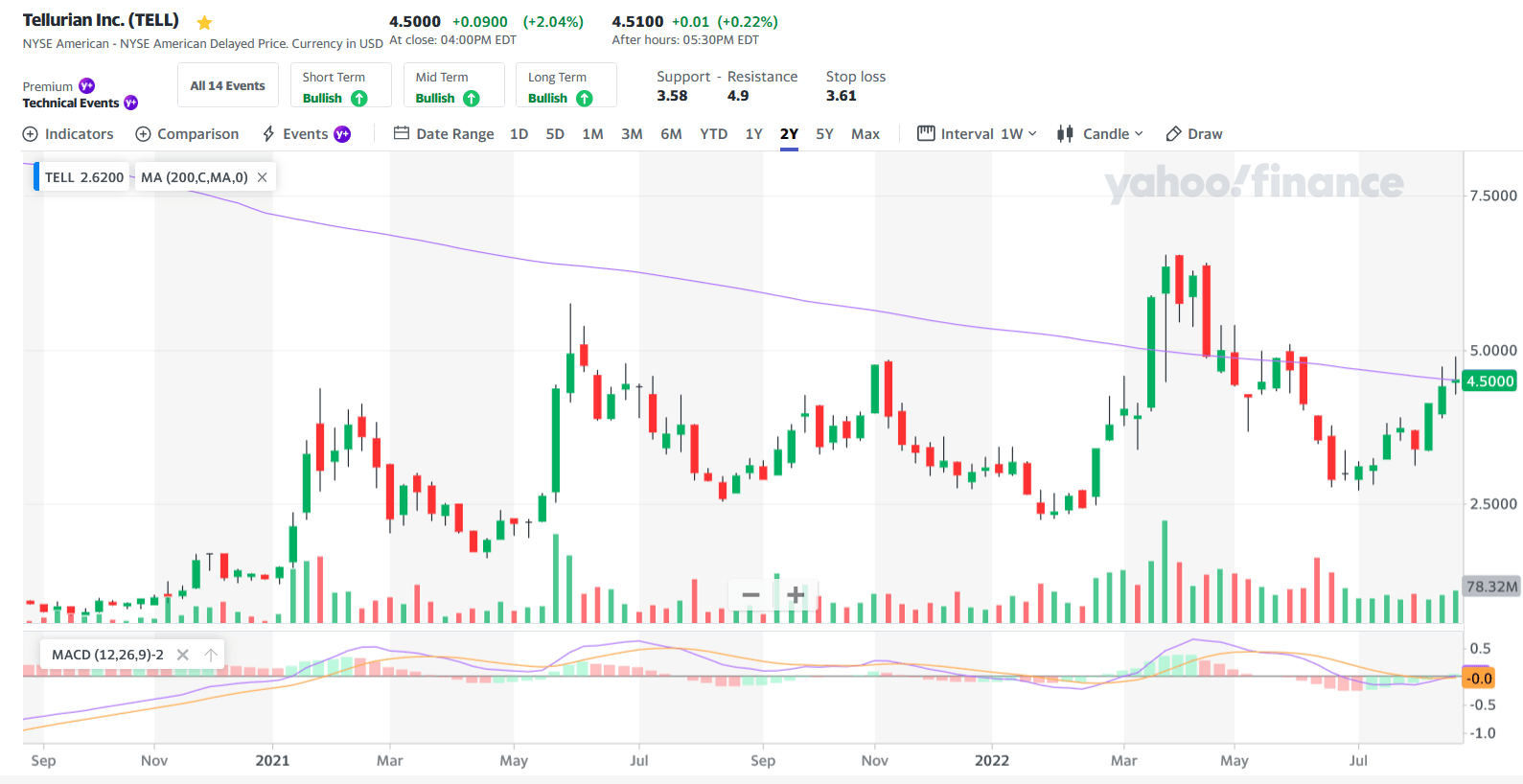

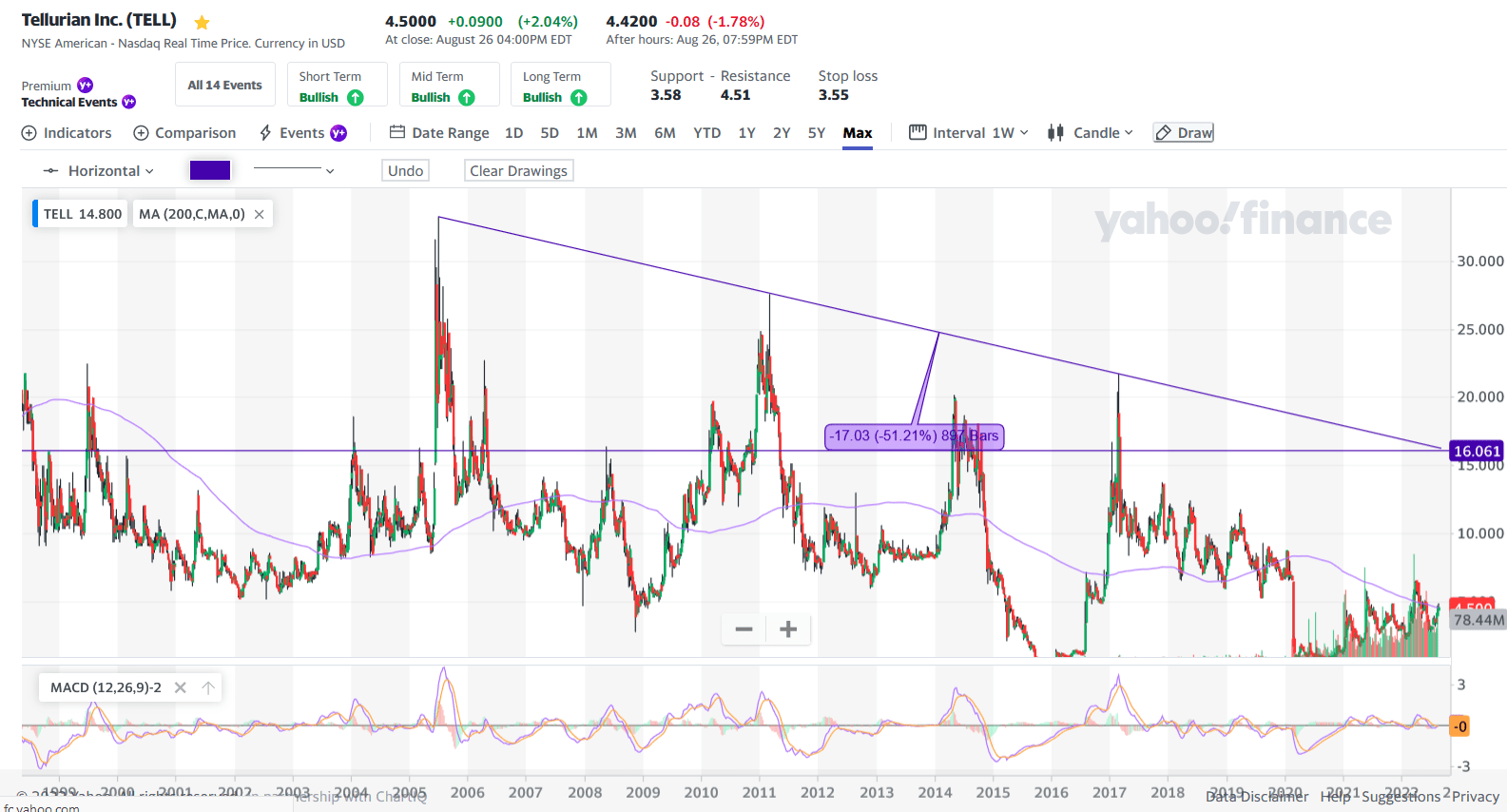

If financing goes by, the long run money flows are discounted at a a lot decrease fee, very similar to a biotech firm transferring by medical trials and getting FDA approval. We estimate that the low cost fee for TELL presently is about 40%, however on FID or FNTP the low cost fee will drop to 15%. That ahead valuation ought to enhance 2.66 instances based mostly on a reduction issue contraction from 40% to 15% (40/15=2.66). That derisking would indicate a worth goal of $12 per share (2.66 x 4.5/share = $12/share) on FID. Moreover, a long-term downward sloping development line within the chart under suggests a worth goal on FID derisking might take the inventory to $16/share.

Technical worth goal (Yahoo Finance IGA analysis technical worth goal)

Assuming $11 billion in money movement in 2026, based mostly on TELL’s investor package deal forecast and a three-times money movement a number of, TELL might have a market cap of $33 billion in 2026-27. Assuming Tellurian has one billion shares excellent, because of dilution from convertible bonds and convertible inventory issuance, TELL may very well be a $33/share inventory or 13 “bagger” as Peter Lynch wrote in One Up on Wall Avenue.

Financing Mannequin Change

Tellurian modified its financing mannequin goal from “FID” Ultimate Funding Determination to a rolling fairness and money movement funding technique. This financing technique change annoyed shareholders and emboldened shorts. In late 2021, Souki had introduced that Tellurian would announce their banking group by yr finish. The corporate has stated that the financing could be 1/Three fairness and a couple of/Three debt. Consequently, when the financial institution financing syndicate staff, representing $Eight bn in financial institution debt or placement capability, was not introduced, traders have been disenchanted. This will have occurred because of the firm not buying sufficient Haynesville pure gasoline to safe that financing dedication or rates of interest rising. Early in 2022 Souki had projected that Tellurian would obtain FID within the first half of the yr. When the FID was not introduced, this once more damage the inventory as a result of the financing of the Driftwood challenge is a major derisking of Tellurian’s “raison d’etre” building challenge. Many thought that saying the FID would transfer TELL inventory to the double-digit worth vary. Then the inventory would begin a gentle upward march, very similar to Cheniere’s inventory did throughout its second financing run.

The opposite key valuation aspect was TELL’s fairness finance facet. Many thought that Tellurian’s solely fairness supply was promoting widespread inventory. This merely was not true. TELL’s fairness can come in several varieties, together with TELL’s upstream belongings/money movement, infrastructure funding (like the unique Blackstone/Sabine Go deal), a strategic investor (LNG off taker or home E&P), convertible inventory, or TELL inventory (which is least favored and most dilutive.) These building finance transactions might be complicated. They are often carried out on the Driftwood degree or on the Tellurian Inc. degree. Blackstone’s convertible cope with Cheniere in 2012 illustrates the complexity of a convert deal and is a logical confirmed financing technique TELL could use — Cheniere Agrees to Promote $2B of Fairness for Sabine Go Liquefaction Undertaking – Blackstone

Souki is a former funding banker, and the administration owns 20% of Tellurian inventory, so we count on that Souki will look to make use of each viable choice to pursue the least dilutive alternative to boost capital. Consequently, utilizing their very own money movement from upstream operations and or discovering a strategic investor-customer could be the popular path to financing, even when it takes longer and to the chagrin of retail traders.

Strategic Fairness Investor Nat Fuel E&P or Worldwide Off Taker

On February 24th, the world modified with Russia’s invasion of Ukraine. Inside per week of the Russian invasion of Ukraine, Germany’s Chancellor Olaf Scholz reversed the nation’s inexperienced coverage, ordering the building of LNG import amenities, terminating plans for the Nord Stream 2 pipeline with Russia, and sending weapons to Ukraine. Now Europe might want to change 20 Bcf/d of Russian gasoline, the equal of c. 35% of the world’s LNG market. This led to a pointy spike in LNG costs and Tellurian’s inventory within the six weeks following the invasion.

It appeared that Germany would rapidly purchase Driftwood’s offtake, however they didn’t. It appeared that Germany additionally sought to construction a cope with the Qatari’s however that additionally didn’t transpire. Evidently Europe’s plans to transform to hydrogen made a few of these offers problematic. Asia doesn’t appear so rigid and which may be why we see TELL use the JKM marker for its money movement illustration above, regardless that the European TTF worth is larger.

With the strengthening of the US economic system curiosity prices rose. With this yr’s beautiful vitality disaster, alternatives for strategic traders grew following the Russian invasion of Ukraine. Home strategic traders additionally emerged as extra compelling funding sources. Souki, in his informative two-minute YouTube movies on the Tellurian web site, defined on Could 17th that a number of pure gasoline producers had expressed curiosity in getting access to the worldwide markets by LNG. Two minutes with Charif Souki on corporations seeking to have a bigger presence in U.S. LNG

A number of public pure gasoline corporations reported their curiosity in taking an fairness position in LNG. Potential fairness traders embody: EQT Company (EQT), Chesapeake Vitality Company (CHK), Comstock Sources Inc. (CRK), Devon Vitality Company (DVN), Antero Midstream (AM) and Southwestern Vitality Firm (SWN). Souki stated that the Cheniere Sabine Go facility was first funded with the fairness after which the banks adopted.

We now consider that EQT Company, the nation’s largest pure gasoline producer, could be a logical strategic investor in Driftwood. Moreover, EQT simply renewed a $2.5 bn five-year line of credit score and with the signing of the Inflation Discount Act, the Mountain Valley Pipeline ought to make connecting the Utica and Marcellus shales within the Northeast with Driftwood extra viable.

Moreover, on August fifth, Southwestern Vitality Firm (SWN), the biggest Haynesville pure gasoline producer within the US, stated of their convention name “We’re evaluating on a threat adjusted foundation, potential alternatives to profit from international pricing by leveraging our approximate dependable long-term provide functionality to assist allow liquefaction tasks to attain FID”, Invoice Approach, CEO. That reads like a transparent indication that SWN would possible fund TELL.

The New Milestone FNTP versus FID

One of many tales that the shorts have been touting was that the SPA contracts of Vitol and Shell would expire on July 31, 2022, if a Full Discover To Proceed “FNTP” was not agreed to by Bechtel for Driftwood. (See web page 21 underneath situation precedent.) That risk got here and went. Amendments to the SPAs have been introduced and neither Vitol nor Shell cancelled their SPAs. (See web page 22.) Vitol and Shell personal the LNG transport ships and cost a price for his or her service, except the challenge regarded unlikely to succeed, why would they cancel these agreements if LNG is in nice demand?

What grew to become clear is that FNTP is extra significant than the FID, in that if Bechtel commits to constructing the ability, then the prospect the ability being constructed is assured and the ultimate parts of the financing are of secondary concern to Bechtel. Although FNTP financing quantity required by Bechtel has not been made public, it’s lower than the total FID of $12.Eight bn.

We see a sequential funding continuing like this. Tellurian raises $3.Four billion from strategics EQT and SWN with every contributing $1.7 billion every, then with TELL’s personal $800 million ($675 million money and $200 million in money movement 2022), then the $4.2 billion in fairness could be coated. Then Tellurian would possibly elevate $Four billion in debt by its financial institution syndicate and or convertible inventory. Souki had disclosed that that they had signed over 50 NDAs signed with potential funders. Then Tellurian might have about $8.2 billion which is perhaps sufficient for Bechtel’s FNTP milestone. Beneath NDA, Tellurian would possibly have the ability to disclose funding sources just like the EXIM financial institution or different financing choices which might fulfill Bechtel.

Consequently, we consider that FNTP is the important thing milestone for Tellurian to derisk its inventory. With a better inventory worth and a decrease threat profile, with or with out EXIM financial institution, Tellurian might obtain its FID as late as 2023, however shareholders may very well be rewarded for his or her persistence since this rolling financing construction could be TELL’s least dilutive financing course of.

Current Optimistic Information Helps Tellurian’s Imminent Financing

On June 1, 2022, Tellurian signed a $500mm convertible bond deal. As well as, on July 13, 2022, Tellurian entered into an settlement to amass further Haynesville Shale land and manufacturing from EnSight strengthening its potential to self-fund. On August 3rd, Tellurian reported a 47% sequential enhance in pure gasoline manufacturing. On August 18th, the creator initially printed an analogous TELL article on In search of Alpha, TELL closed 13% larger and benefited from their Haynesville EnSight deal closing information. So as to get the Inflation Discount Act handed, Joe Manchin negotiated for approval of the Mountain Valley Pipeline. The August 16th passage of the Inflation Discount Act ought to facilitate EQT being a strategic investor together with SWN, although different entities or combos might make the strategic fairness funding in Driftwood to assist it safe its focused the $4.2 billion in funding.

On July 13, 2022, Souki made a considerate critique of the pay for service or toll highway mannequin versus Tellurian’s built-in mannequin declaring that Cheniere needed to ask for an emissions waiver and that the Freeport explosion reveals that there’s little room for error within the conventional price for service mannequin which Tellurian is in search of to displace. Two minutes with Charif Souki on the Tellurian mannequin. The undeniable fact that Icahn Enterprises L.P. (IEP) just lately bought its Cheniere inventory again to Cheniere is sort of attention-grabbing, particularly when Icahn stepped into Cheniere inventory simply as its growth plans have been materializing.

Tellurian is using cutting-edge Zero Emissions know-how and dealing with Bechtel, the EPC Cheniere used. We consider that most of the finance relationships that Souki cast whereas at Cheniere provides him a deep bench of funding prospects with whom Souki has credibility. We additionally like Tellurian’s institutional shareholders, a few of who we think about among the many smartest on Wall Avenue: Blackrock Inc., Paulson & Firm, Inc., Shaw, D.E. & Co. Inc., and Citadel Advisors, LLC. Tellurian seems to be in good place to safe funding for FNTP and turn into a strong progress story like Cheniere and an vitality transition star. The macroeconomic atmosphere with spiking pure gasoline costs couldn’t be higher for Tellurian to finance Driftwood LNG.

[ad_2]

Supply hyperlink