[ad_1]

ronniechua

China Lockdown

Following months of intense pandemic restrictions, China’s “zero COVID” coverage pressured residents to isolate at house, the plenty had been quarantined, and enterprise operations halted. The sacrifices made by residents and companies in a number of the world’s largest hubs like Shanghai and Beijing are lastly seeing some reprieve.

As we have a look at the decline in worldwide markets like China, buyers keen to take some dangers when others are fearful may even see the advantages. As I not too long ago wrote in Diamonds In The Tough: Three Prime Rising Market Shares, worldwide shares have been struggling below inflationary and recessionary pressures. Over the past 12 months, Chinese language markets have bought off by greater than 27%. These selloffs have created labor shortages all through the nation and affected world transport and provide chains across the globe. Discovering good shares in rising markets can require some digging. Looking for Alpha gives instruments to create your personal inventory screeners to ship buyers’ the names of basically sound corporations in a number of the largest growing nations. I used these screens to establish these shares. Based mostly on our quant scores, I’ve chosen three Chinese language corporations with Purchase suggestions to think about diversifying a portfolio.

Investing Within the China Reopening

Any firm domiciled in China has sustaining political dangers. One of many largest dangers concerned China’s poor healthcare system – the Achilles heel for reopening – forcing China to have a number of countrywide shutdowns given the shortage of entry to enough healthcare to combat the pandemic. These impacts had been felt across the globe, given the shortages within the Chinese language labor market, demand, and world provide chains.

Politics, authorities rules, and transparency are different issues for buyers. China has a repute for falsifying information stories that decision into query the integrity of firm financials. As well as, the government-imposed restrictions, censorship, and so forth., have all posed challenges and issues for buyers. Take, as an illustration, Alibaba’s (BABA) meant IPO of Ant Group was held up by Chinese language regulators. Or the gaming limitations and pandemic controls positioned on Tencent Holdings Restricted (OTCPK:TCEHY) and different establishments pose dangers to buyers investing in any Chinese language firm. Now my level is to not discourage buyers from contemplating corporations in China. I merely need to define some potential dangers and emphasize that the secret’s performing due diligence and in search of corporations with robust fundamentals.

Chinese language markets have been down greater than 27% during the last 12 months in comparison with the S&P 500, which was down greater than 10%. Most of the dangers and issues highlighted above have been discounted, as seen by China’s fairness market underperforming the U.S. benchmark over this 52-week interval. Nonetheless, extra not too long ago, as the federal government’s easing rears its head in China, its markets have rallied. This development began in mid-June as reported by SA Information, Alibaba, JD.com rise as sentiment in the direction of Chinese language tech begins to regular. As evidenced within the beneath chart, the MCHI is now outperforming the SPY on a year-to-date foundation.

MCHI vs. SPY year-to-date efficiency

MCHI vs SPY YTD efficiency (Looking for Alpha Premium)

Following final week’s information that China is contemplating a $220B stimulus to spice up its economic system, a number of Chinese language shares carried out favorably, together with two of our picks, JD.com (NASDAQ:JD) and Baidu (NASDAQ:BIDU). China would permit native governments to promote as much as $220B in bonds, the primary time bonds could be bought earlier than the beginning of the 12 months. I see this as a chance that would show favorable. For now, I consider wanting into sectors that rallied over the past a number of weeks within the U.S. post-stimulus, like progress and a few cyclical consumer-driven sectors post-COVID – and a few tech – at their present valuations may show useful. JD and BIDU are properly off of their 52-week highs. The tide might be turning for these shares as all three have outperformed the S&P 500 during the last Four weeks. With a deal with core metrics, fundamentals, and stable steadiness sheets, my three inventory picks expertise some nice returns for portfolios.

Three Chinese language Shares To Purchase

China is thought for its superior tech industries and ranging services. As its economic system begins to get better from strict lockdowns, we consider three Chinese language shares stand to profit from the nation’s reopening that could be price contemplating for a portfolio. Take a look at these three inventory picks.

1. JD.com, Inc. (JD)

-

Market Capitalization: $98.90B

-

Quant Ranking: Purchase

-

Quant Sector Rating (as of seven/8): 67 out of 527

-

Quant Business Rating (as of seven/8): 1 out of 61

Headquartered in Beijing, China, JD.com, Inc. is the must-needed provide chain-based expertise and logistics firm providing varied merchandise and market providers. It develops, owns, and manages logistics services. The corporate has a wholesome steadiness sheet with greater than $7.3B money available and vital year-over-year cashflow progress. In comparison with different big-name Chinese language corporations like Alibaba and Tencent Holdings, its enterprise outperforms. Following indicators of accelerating income final Thursday, JD inventory rallied as a lot as 3%. Regardless of a lower than superb D Valuation grade, a number of the underlying valuation metrics coupled with stellar momentum grades point out this inventory is a stable purchase.

JD Valuation & Momentum

Like many Chinese language corporations, JD.com felt the results of prolonged lockdowns and destructive sentiments surrounding corporations overseas. Whereas JD’s inventory worth comes at a premium, ahead EV/Gross sales of 0.52x point out a -50.89% low cost in comparison with its friends. Its B- ahead Worth/Gross sales are additionally stable, with a close to 30% distinction to the sector.

JD Momentum Grade (Looking for Alpha Premium)

As we have a look at the inventory’s momentum grade and quarterly worth efficiency, JD outperforms friends quarterly, with six- and nine-month price-performance practically 4x and 2x (respectively) higher than the sector median. Though the inventory’s worth is -6.47% YTD and JD.com is more likely to proceed going through headwinds given geopolitical elements, the corporate continues to extend its buyer base, gross sales, and thus income year-over-year. Based mostly on the latest earnings report and potential enterprise ramp-up amid China’s reopening, JD may see super progress and profitability.

JD Progress & Profitability

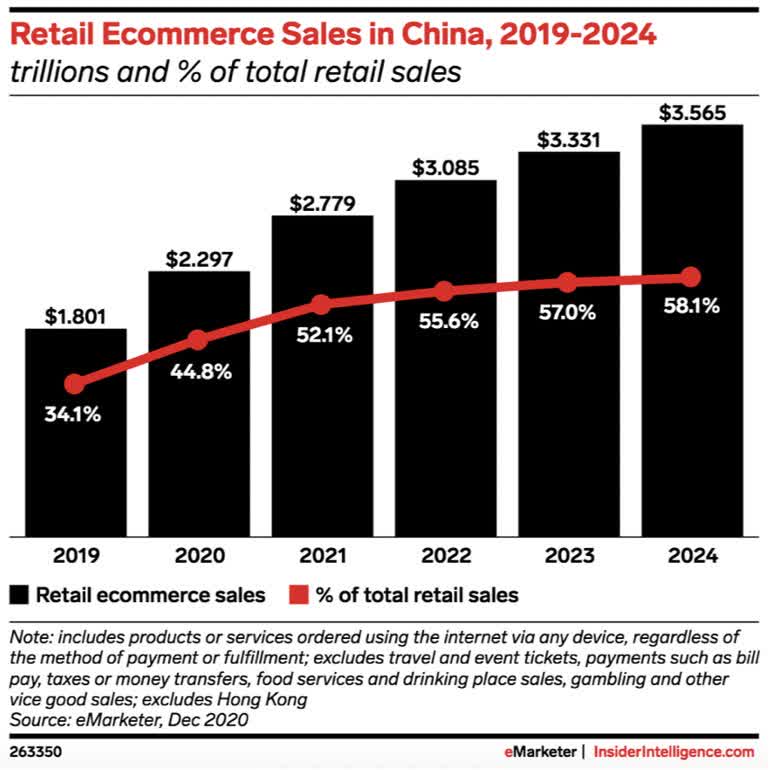

The Might kickoff of JD.com’s annual procuring pageant referred to as 618 Grand Promotion proved profitable. Though {industry} developments point out that retail e-commerce gross sales in China have flattened over the previous few years, JD continues to expertise excessive progress, together with JD’s logistics CAGR of 6% forecasted from 2021 to 2026.

Retail Ecommerce Gross sales in China, 2019-2024 (eMarketer|InsiderIntelligence.com)

JD possesses diversified earnings streams that embrace e-commerce, logistics, and expertise.

-

JD E-commerce – The biggest on-line retailer in China and main one-stop e-commerce platform, JD is a Fortune World 500 firm.

-

JD Logistics – As of March 31, 2022, JD.com operates greater than 40 of Asia’s largest and most automated sensible success logistics facilities. Utilizing superior applied sciences, JD has achieved prime charges of success of practically 90%.

-

JD Expertise – By way of industry-leading revolutionary retail provide chain applied sciences, JD.com is on the forefront of robotics and automation, providing the primary drone industrial deliveries and unmanned automobiles. Ai and machine studying instruments are on the forefront of their want to carry sensible logistics to prospects.

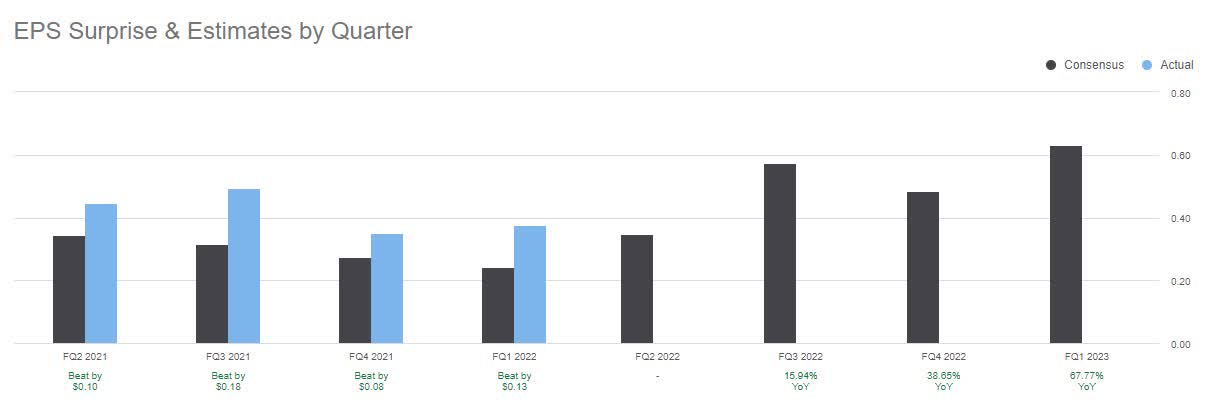

As showcased within the current earnings report, JD beat each top-and bottom-line outcomes. With an EPS of $0.38 beating by $0.13 and income of $35.58B beating by $850.74M (12.69% YoY), these figures point out that JD prospects are utilizing the platform, and the agency is experiencing larger consumer progress.

“China’s Web {industry} is getting into a extra mature improvement stage going ahead as we optimize and broaden our omnichannel ecosystem and we proceed to broaden and meet the variety of our customers, creating long-term consumer worth…We’re proud that JD’s provide chain capabilities and the enterprise mannequin have confirmed themselves helpful within the combat in opposition to the epidemic…Sooner or later, we’ll proceed to optimize general working effectivity and drive a sustainable high-quality progress with wholesome money movement and profitability” –Lei Xu, JD.com CEO.

JD.com EPS (Looking for Alpha Premium)

Along with regular income for Q1 2022, JD’s govt workforce plans to deal with optimizing operations and creating a greater buyer construction.

Concerning profitability, a number of the standard metrics for the twelve-month trailing are underwhelming in comparison with the sector. With this in thoughts, as talked about above, the corporate possesses $7.31 Billion in Money from Operations. On this atmosphere, ‘Money is King’. Given the chip shortages and worth will increase which have affected a few of their tech classes, the reopening of warehouses and success services, and the success of the 618 Grade Promotion, JD stands to see bettering outcomes, which is why the Looking for Alpha quant scores assist this inventory as a purchase.

2. Baidu (BIDU)

-

Market Capitalization: $51.55B

-

Quant Ranking: Purchase

-

Quant Sector Rating (as of seven/8): 18 out of 248

-

Quant Business Rating (as of seven/8): Four out of 60

Stringent rules and insurance policies have created hurdles to restrict the variety of Chinese language shares, significantly these within the tech sector like Baidu. These limitations have brought on their shares to fall, and now with reopening and different tailwinds, I consider these shares could also be positioned to realize.

With recessionary fears and geopolitical uncertainty surrounding China, the announcement of a possible $220B stimulus got here proper on time, prompting Baidu’s inventory to leap for pleasure final Thursday. The downturn skilled by many tech giants on account of a crackdown on Chinese language expertise has created some issues for buyers. Baidu is a tech big whose core internet advertising enterprise (79%) generates the majority of its income. Baidu gives web search providers and an internet neighborhood by way of Baidu Core and iQIYI segments. Experiencing a one-year worth decline of greater than 13%, Baidu has not too long ago undergone an up-trend. Closely investing in Ai and autonomous automobiles, Baidu could also be a inventory for the long run.

BIDU Valuation & Momentum

Though BIDU’s C- valuation will not be superb and underlying metrics come at a little bit of a premium, the inventory continues to be buying and selling properly beneath its 52-week excessive and possesses tailwinds for upside potential in step with A+ momentum.

BIDU Momentum Grade (Looking for Alpha Premium)

As you possibly can see from the momentum grades, BIDU’s worth efficiency considerably outperforms its friends on a quarterly foundation. As Looking for Alpha contributor Chen Yang writes:

“Baidu’s valuation a number of is low. Nonetheless, within the subsequent three years, I estimate that each AI Cloud and autonomous driving enterprise will develop exponentially. In 2024, non-ad enterprise may take 50% of complete core income. Cloud enterprise may take ~28% (46% CAGR), the remaining (Apollo, Jidu, Xiaodu, Kunlun) may present the remaining 22%…By that point, Baidu may have the next valuation a number of on account of extra tech parts. The very best buying and selling technique is to carry it.”

Along with diversified income streams, this inventory showcases a stable progress and profitability outlook.

BIDU Progress & Profitability

With a fast-growing cloud enterprise and digital promoting section, BIDU has continued to beat earnings estimates, regardless of a slowdown attributed to the pandemic, regulatory issues, and its streaming video service iQIYI, which Baidu is rumored to be bought for $7B. Baidu holds a majority share of iQIYI that quantities to 53%, which it says is not a part of its core enterprise.

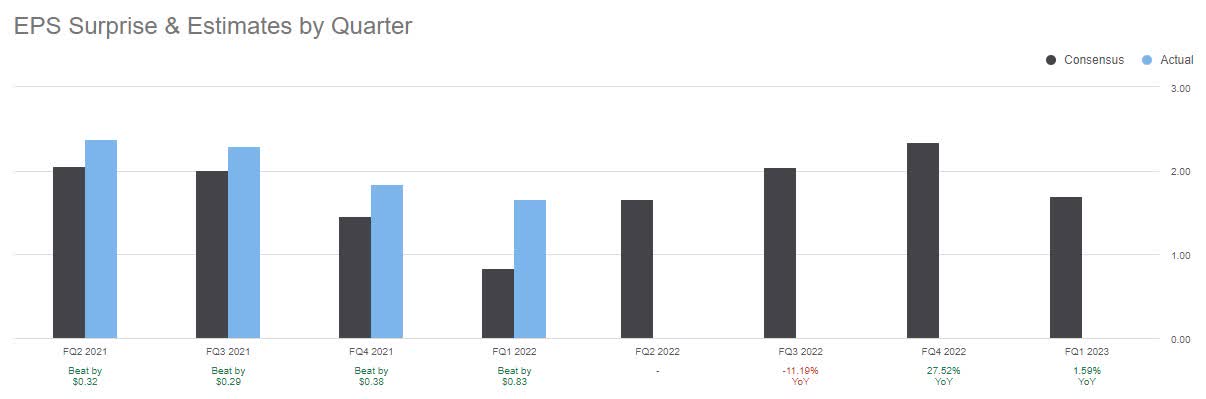

For 2022 Q1, the Baidu App MAU grew 13%, considerably larger than the two% progress of cellular customers. Beating top-and bottom-line earnings, EPS of $1.67 beat by $0.83, and income of $4.22B beat by $58.95M.

BIDU EPS (Looking for Alpha Premium)

With substantial dry powder ($2.82B) to spend money on Ai and expertise, Baidu’s cloud expertise has grown 45% year-over-year plus seen a 35% improve in non-online advertising income +850M for Q1.

“We see nice alternatives to make use of expertise to speed up the event of the actual economic system. Organizations in varied sectors, comparable to power and utilities, manufacturing, finance, and the general public sector, have come to appreciate that not solely they want digitize what they do, they will additionally use all types of AI applied sciences to boost their competitiveness by means of value discount and effectivity enchancment. So the demand for digitization and AI come on the identical time. That presents a novel alternative for us to ship Baidu AI Cloud options in a seamless method” –Robin Li, Co-Founder & CEO of Baidu.

Baidu is in a rising sector that appears to the long run and is making an attempt to scale whereas reducing prices efficiently. Though uncertainty surrounds this tech chief, given regulatory headwinds and opponents like Alibaba and Tencent in its area, BIDU’s R&D, dominant consumer base, and ecosystem efficiently centered on cellular purposes ought to function a moat. We consider this expertise behemoth and our subsequent smaller-scale tech firm will likely be Chinese language shares price investing in.

3. Daqo New Power Corp. (NYSE:DQ)

-

Market Capitalization: $5.29B

-

Quant Ranking: Sturdy Purchase

-

Quant Sector Rating (as of seven/8): 1 out of 630

-

Quant Business Rating (as of seven/8): 1 out of 30

Headquartered in Shanghai, China, and within the enterprise of certainly one of my favourite tech sectors, semiconductors, I’ve written about Daqo New Power Corp. as a powerful Inventory For a Horrible Market. The inventory is up 90% for the reason that writing of the Might 12th article. Nonetheless, from a valuation perspective on ahead P/E, it stays at a big 82% low cost to the IT sector and a 31% low cost to its 5-12 months historic common. Daqo is a number one producer and vendor of low-cost semiconductor tools for high-purity solar energy options. Utilizing polysilicon materials, a preferred and first conducting element required by photo voltaic merchandise, DQ ought to stand to profit from its renewable enterprise, as the corporate continues to be a number one clear power firm with excessive document gross sales, income, and earnings. Along with its industry-leading monitor document, Daqo’s subsidiary Xinjiang Daqo obtained approval from the China Securities Regulatory Fee for a personal A-share providing for use for growth. If that’s not an indicator of potential progress and income, let’s dive into these metrics.

DQ Progress & Profitability

Thought-about a sizzling inventory on a photo voltaic shares rally, DQ advancing virtually 15% final Thursday and because the frontrunner as photo voltaic and clear power information beloved the stories of a China stimulus bundle. DQ has been operationally sound and one of many prime gainers within the semiconductor tools {industry}.

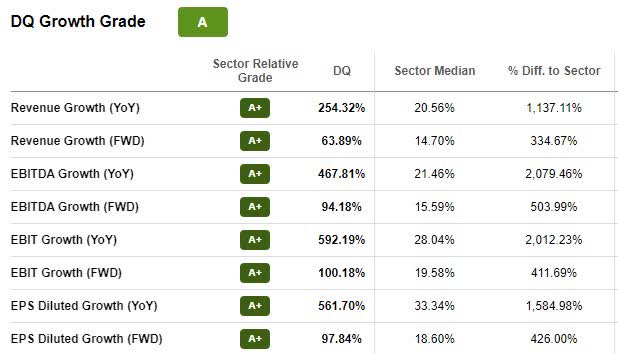

With income progress of +254% year-over-year, and experiencing a rise in gross margins, the corporate is poised to proceed outperforming the market.

DQ Progress Grade (Looking for Alpha Premium)

Because the push for inexperienced power grows and DQ takes benefit of its low manufacturing prices for polysilicon, it may possibly keep its aggressive benefit. Over the past 90 days, seven analysts supplied FY1 Up revisions, and document revenues had been recorded for Q1 2022.

“We recorded $1.Three billion in income, additionally greater than 3x of the income for the fourth quarter of 2021, and we recorded working earnings of $797 million, internet earnings attributable to Daqo New Power shareholders of $536 million, earnings per share of $7.17 per share and EBITDA of $827 million, all representing substantial sequential and year-over-year progress,” stated Daqo CEO Longgen Zhang

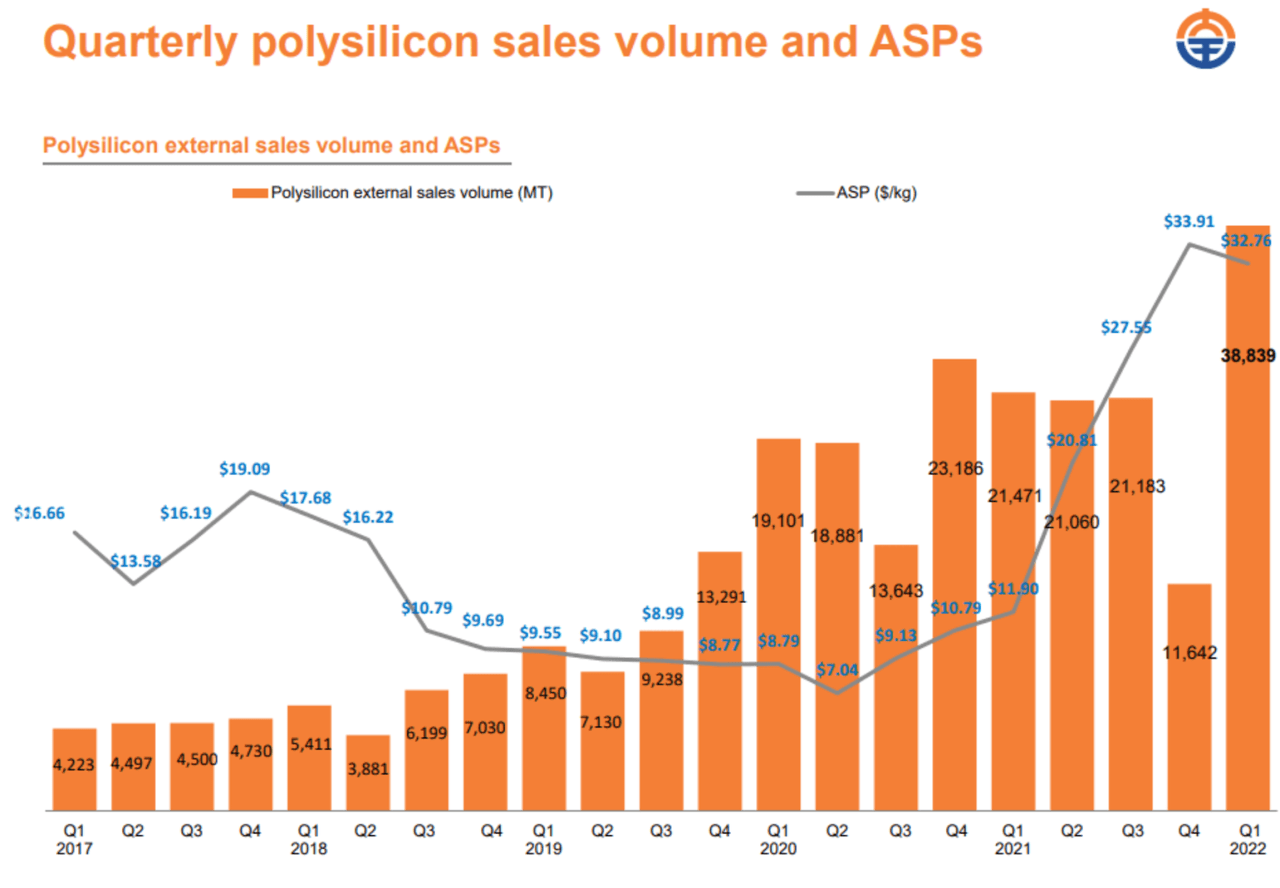

DQ’s excessive purity polysilicon materials is crucial in producing photo voltaic photovoltaic (PV) expertise which converts mild into electrical energy. This genius conversion of sunshine into electrical energy has enabled Daqo to expertise excessive demand and gross sales volumes, prompting a ramp-up in manufacturing.

DQ’s Polysilicon Gross sales Volumes (DQ Q1 2022 Investor Presentation)

Not solely has 2022 Q1 resulted in gross income of $813.6M in comparison with 2021 This autumn of $118.9M, the gross margins additionally noticed will increase attributed to decreased manufacturing prices for uncooked supplies and better demand. With robust free money movement and money from operations, it’s no shock that DQ has plans for continued growth in varied enterprise traces.

“Final 12 months, Daqo arrange a roadmap to extend manufacturing capability to 270,000 metric tons MT by the top of 2024, representing a 50% annual progress price. In Q1, the brand new Section 4B manufacturing facility was accomplished. The brand new facility elevated complete polysilicon capability by 35,000 MT. Slight will increase in manufacturing quantity are seen every quarter, that are attributable to the ramp-up part within the newest facility” –Friso Alenus, Looking for Alpha Contributor.

DQ Profitability Grade (Looking for Alpha Premium)

Though the corporate faces related dangers, together with geopolitical and lockdown-related, the general outlook stays robust for DQ on the present worth level.

DQ Valuation & Momentum

12 months-to-date, DQ is +75%, and during the last 12 months, +7%. DQ’s collective issue grades are spectacular. With A’s practically all throughout the board and a valuation severely discounted relative to its friends, this inventory is undervalued.

Possessing a ahead P/E ratio of three.69x, DQ trades at greater than 82% low cost and maintains a PEG (TTM) of -98.18% distinction to the sector.

DQ Issue Grades (Looking for Alpha Premium)

Quarterly, DQ’s worth efficiency outperforms sector friends considerably. Though the dangers related to this firm generally is a bit off-putting for buyers, the inventory’s bullish momentum, discounted worth, super progress, and profitability are key concerns when investing on this inventory. Though these inventory picks may face some headwinds, I consider that JD, BIDU, and DQ are Three Chinese language shares whose purchase scores are justified primarily based on their quant scores and stable underlying metrics.

Investing in Chinese language Shares

For quite a lot of years, on a political degree, tensions between america and China have remained heightened. China is a really aggressive financial associate to america – the important thing phrase right here being a associate. The depth of the connection between each international locations may be present in commerce information from The US-China Enterprise Council. As of 2020, the commerce relationship accounts for multiple million American jobs. Accordingly, American corporations exported $188 billion in Items and Companies Exports to China. It is a aggressive relationship, however it’s mutually useful to each international locations in some ways.

Whereas a bit scary, world market situations can show favorable, particularly within the three completely different sectors I’ve chosen. Though YTD the MSCI China is down 11%, it’s begun a rally, outperforming the S&P 500 by greater than 7% for a similar interval. As such, there is a chance to capitalize. No threat. No reward! When you’re keen to deal with shares with stable earnings and progress potential, in occasions when concern is shifting markets, proudly owning shares with robust funding traits and Quant purchase suggestions may see the chance for a powerful rebound.

The Chinese language market is full of growth-oriented corporations that search to take just a little threat and need to diversify. JD, BIDU, and DQ supply an important basket in different sectors: shopper discretionary, communication providers, and expertise.

[ad_2]

Supply hyperlink