[ad_1]

Worth motion has been primarily sturdy this week, a improvement that any investor can have a good time. The best way issues are shaping up, the S&P 500 is on its method to recording its third weekly shut within the inexperienced out of the final ten.

It goes with out saying that it’s been a harsh atmosphere to put money into all through 2022. A hawkish Fed, provide chain points ensuing from the battle in Ukraine, and COVID-19 uncertainties have all negatively impacted monetary markets year-to-date.

Nonetheless, the market rolls on.

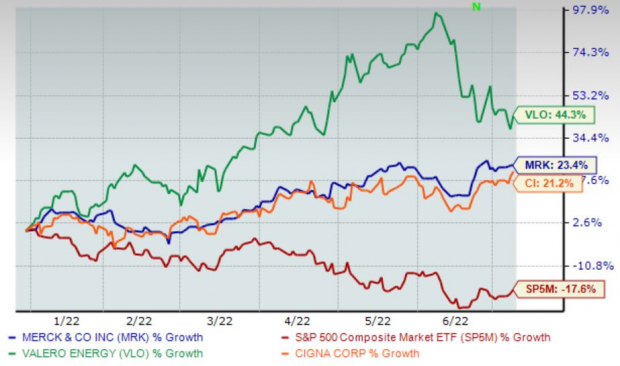

Surprisingly sufficient, there are corporations on the market within the inexperienced year-to-date, together with Cigna Corp. (CI – Free Report) , Merck (MRK – Free Report) , and Valero Power Corp. (VLO – Free Report) . The year-to-date chart under reveals the efficiency of all three corporations’ shares whereas mixing within the S&P 500 as a benchmark.

Picture Supply: Zacks Funding Analysis

As we are able to see, all three corporations have loved sturdy performances year-to-date, simply outperforming the S&P 500.

All three are large-cap corporations with sturdy Zacks Ranks – a major perk that instills confidence in these corporations’ share performances transferring ahead.

Massive-cap corporations are usually much less unstable investments and usually pay dividends. In spite of everything, who doesn’t get pleasure from getting paid?

Let’s look at every firm intently to see why they’d be strong portfolio provides transferring ahead.

Cigna Corp.

Cigna (CI – Free Report) is a worldwide well being companies firm that delivers selection, predictability, affordability, and entry to high quality care by built-in capabilities and linked, personalised options that advance whole-person well being. Cigna is a Zacks Rank #2 (Purchase) with an total VGM Rating of an A.

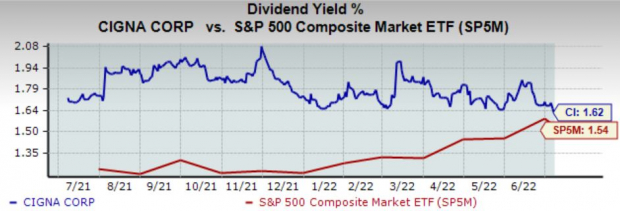

The corporate rewards its shareholders through its annual dividend that yields 1.6%, with a payout ratio sitting sustainably at 21% of earnings. What stands out to me is the corporate’s five-year annualized dividend development fee of a triple-digit 224%.

As well as, the yield is larger than that of the S&P 500.

Picture Supply: Zacks Funding Analysis

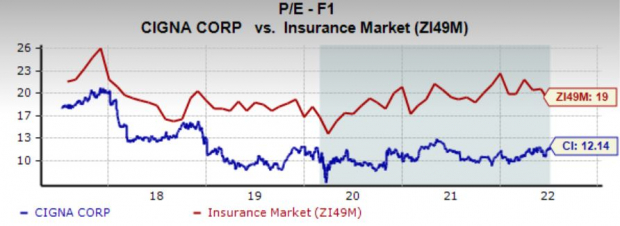

CI additionally sports activities attractive valuation metrics. Its 12.1X ahead earnings a number of is effectively under 2017 highs of 20.5X and represents a beautiful 36% low cost relative to its Zacks Business.

Picture Supply: Zacks Funding Analysis

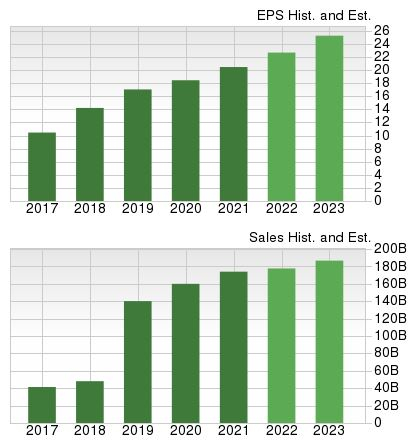

The $22.68 per share consensus EPS estimate for the present fiscal yr displays a notable double-digit enhance in earnings of practically 11% year-over-year. Moreover, for the upcoming quarterly report, earnings are forecasted to develop 4% from the year-ago quarter.

The highest-line is forecasted to increase properly as effectively. The FY22 income estimate of $177 billion pencils in a 2% uptick in income year-over-year. Quarterly income is forecasted to achieve $44 billion within the upcoming quarter, reflecting a decent 3% enhance in income from the year-ago quarter.

Picture Supply: Zacks Funding Analysis

Merck

Headquartered in New Jersey, Merck (MRK – Free Report) is an American multinational pharmaceutical firm that develops and produces medicines, therapies, and different well being merchandise. Merck is a Zacks Rank #2 (Purchase) that boasts an total VGM Rating of an A.

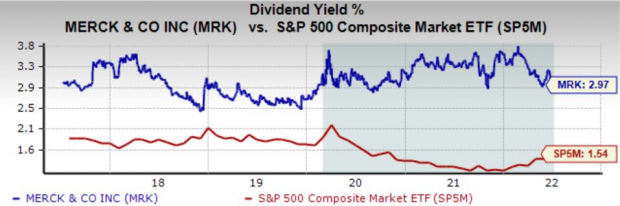

Merck has a strong annual dividend that yields 2.9%, with a payout ratio sitting sustainably at 39% of earnings. Impressively, the corporate has elevated its dividend six occasions over the previous 5 years, with a five-year annualized dividend development fee sitting at 9%.

Moreover, the yield is way larger than that of the S&P 500.

Picture Supply: Zacks Funding Analysis

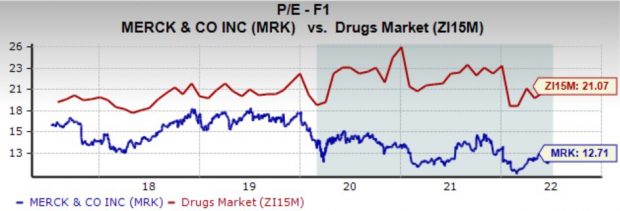

MRK additionally sports activities an enticingly low 12.7X ahead P/E ratio, effectively under 2019 highs of 18.4X and properly beneath its five-year median worth of 14.4X. Moreover, the worth displays a deep 40% low cost relative to its Zacks Business.

Picture Supply: Zacks Funding Analysis

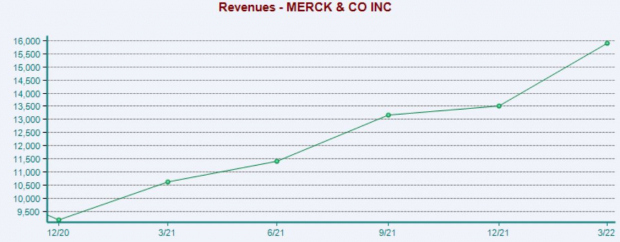

Prime-line forecasts for the present fiscal yr show energy. In FY22, MRK is forecasted to rake in a mighty $58 billion, which interprets to a 16% enlargement within the top-line year-over-year. Quarterly income additionally appears to be like to stay sturdy, with the corporate forecasted to extend its quarterly gross sales by 21% within the upcoming quarter.

Picture Supply: Zacks Funding Analysis

As well as, the $7.31 EPS estimate for the present fiscal yr represents a robust double-digit enlargement within the bottom-line of practically 22%.

Valero Power Corp.

Valero Power (VLO – Free Report) is the biggest unbiased refiner and marketer of petroleum merchandise within the US. The corporate has refineries situated within the US, Canada, and the UK. VLO sports activities a Zacks Rank #1 (Robust Purchase) with an total VGM Rating of an A.

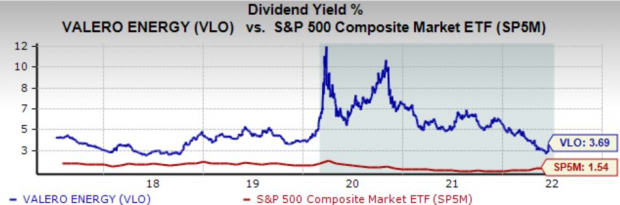

Valero Power’s annual dividend yield sits on the upper aspect at 3.7%, with a barely steep payout ratio sitting at 60% of earnings. The corporate has been devoted to rewarding its shareholders, as displayed by its three dividend will increase over the previous 5 years and a five-year annualized dividend development fee of seven.2%.

Picture Supply: Zacks Funding Analysis

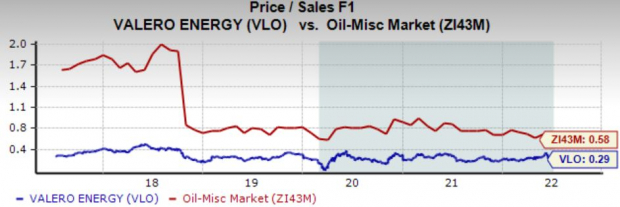

VLO sports activities a 0.3X ahead price-to-sales ratio, which is nowhere close to 2018 highs of 0.5X. As well as, the worth represents an attractive 51% low cost relative to its Zacks Business.

Valero Power has a Type Rating of a B for Worth.

Picture Supply: Zacks Funding Analysis

For the upcoming quarter, the $7.13 per share estimate pencils in a large quad-digit development in earnings of 1385% from the year-ago quarter. Moreover, the $18.08 per share estimate for FY22 interprets to a triple-digit enlargement within the bottom-line of greater than 540% year-over-year.

Clearly, the corporate has benefitted from the rise in vitality costs, which is an enormous motive analysts have revised their earnings estimates considerably over the past 60 days.

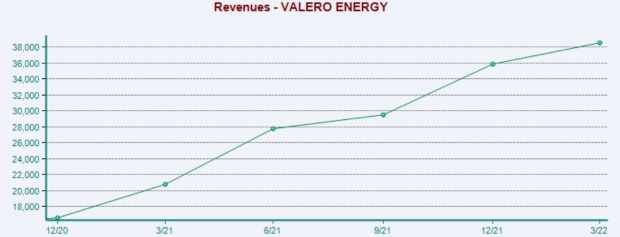

Income is forecasted to climb to an enormous $154 billion in FY22, a considerable 36% enhance year-over-year. Moreover, the $40 billion income estimate for the upcoming quarter interprets to a 41% enhance in quarterly income in comparison with the year-ago quarter.

Picture Supply: Zacks Funding Analysis

Backside Line

All three corporations’ shares have been a shiny spot in 2022, which means patrons have remained in management all year long.

All three corporations have sturdy dividend metrics, strong year-over-year development for the present fiscal yr, and carry a robust Zacks Rank. For buyers wanting so as to add some high quality shares to their portfolios, these three can be a terrific place to start out.

[ad_2]

Supply hyperlink