[ad_1]

D-Keine

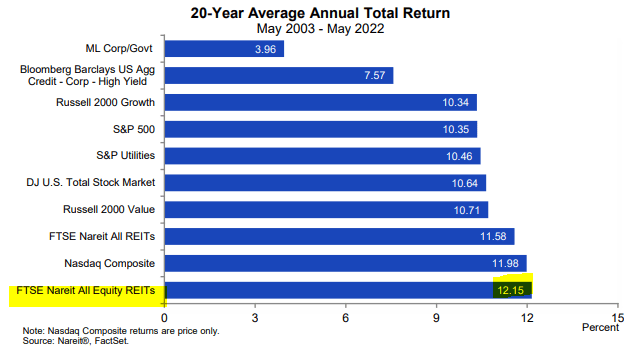

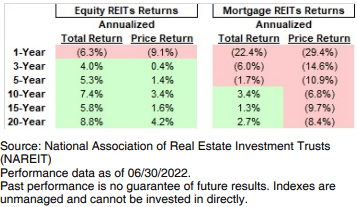

Traditionally, REITs have been a few of the most rewarding investments of all time, incomes as a lot as 12% per yr on common:

NAREIT

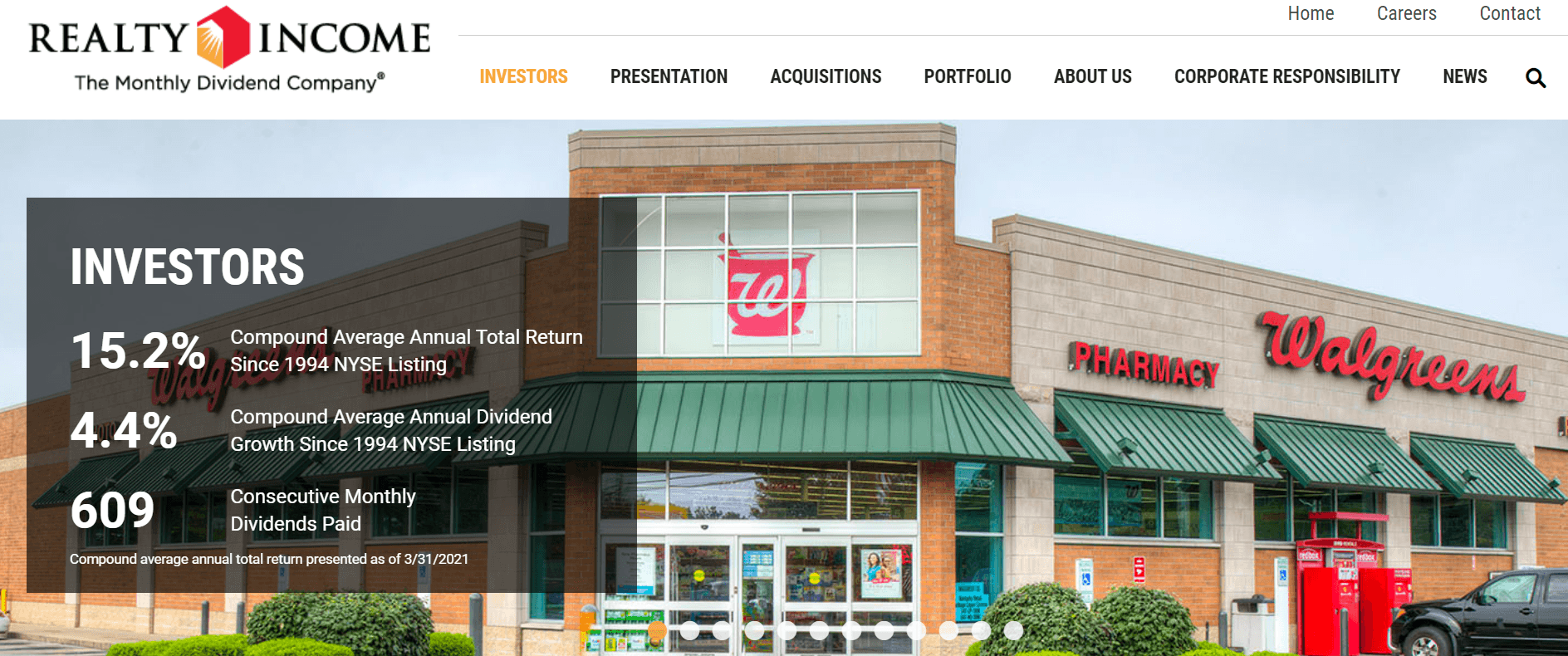

That is simply the common, which incorporates the great and the dangerous. Should you have been selective and managed to weed out the great from the dangerous, you might have earned annual returns as excessive as 15% per yr. Realty Revenue (O), for example, has compounded buyers’ capital by 15.2% yearly since its IPO in 1994:

Realty Revenue

However sadly, the overwhelming majority of REIT buyers by no means really expertise such returns.

I do know this as a result of I positive did not in my early years as a REIT investor, and after writing 100s of articles on REITs right here on Looking for Alpha, I’ve realized that the majority new REIT buyers make comparable errors that value them dearly.

In what follows, I wish to spotlight the 5 greatest errors to keep away from as a REIT investor. Should you can simply keep away from these errors, your returns ought to enhance materially:

Mistake #1: Chasing Yield At All Value

The common dividend yield of REITs is right this moment about 3.5%.

However there are a variety of REITs that yield way more. Some yield as a lot as 10%.

And since all of us love incomes dividends, lots of buyers will naturally go for the higher-yielding names.

The title of our funding neighborhood right here on Looking for Alpha is “Excessive Yield Landlord” so I actually perceive the attraction of incomes greater dividends.

However this is the difficulty: most higher-yielding REITs are priced at a excessive yield for a very good cause. Their dividend just isn’t sustainable, it’s extremely dangerous, and it is not rising. In the long run, higher-yielding REITs usually generate decrease whole returns than the lower-yielding REITs in the long term.

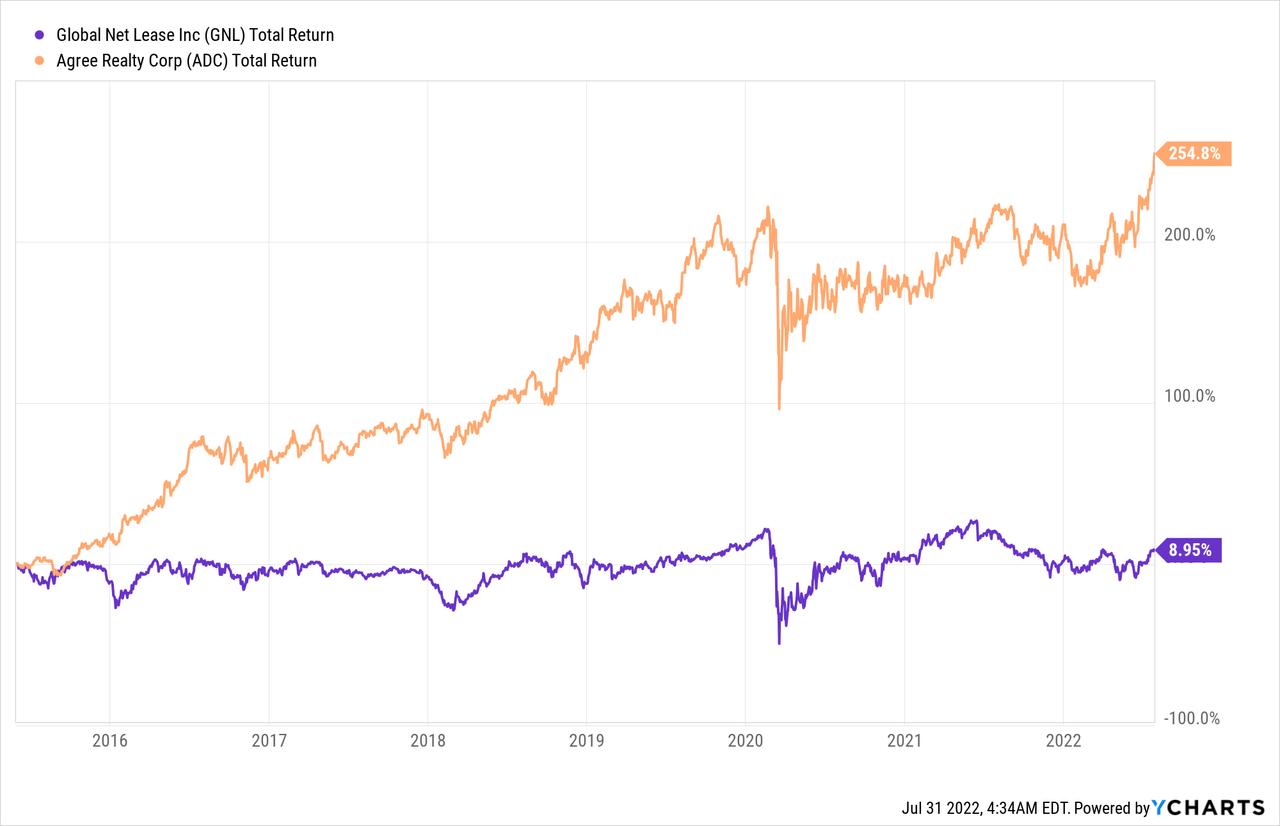

Simply to present you an instance: World Internet Lease (GNL) has yielded 8-12% all through its historical past and but, it has generated far decrease returns than its internet lease peer Agree Realty (ADC), which generally yields solely about 3-4%:

GNL has repeatedly reduce its dividend all through its historical past as a result of it was overpaying and never retaining sufficient money stream for progress.

ADC, alternatively, took the other method, which allowed it to develop its dividend even throughout occasions of disaster, and the inventory market rewarded it accordingly.

This can be a good reminder that REITs usually are not simply earnings automobiles. I believe that lots of new buyers come to REITs as a result of they’re attracted by the excessive dividend funds, however they fail to comprehend that REITs are whole return automobiles and progress issues simply as a lot, if no more than the earnings you obtain.

An excellent rule of thumb is that greater dividend funds will generally lead to decrease whole returns over time and vice-versa.

Mistake #2: Investing in Externally-Managed REITs

REITs could be internally managed or they are often externally managed.

This seemingly small distinction can have a huge effect on funding efficiency.

Internally managed REITs rent their administration as workers of the REIT and so they earn salaries for his or her work.

Externally managed REITs, alternatively, outsource the administration to an exterior asset administration firm that receives charges in change.

The interior administration construction is right this moment the preferred as a result of it does a a lot better job at aligning the pursuits of the administration with these of shareholders. The administration is employed as workers and subsequently, their sole focus is on the REIT and their salaries are generally tied to some efficiency indicators.

Nevertheless, there are nonetheless lots of externally managed REITs and new REIT buyers will typically put money into them not even understanding that they’re externally managed.

The problem with the exterior construction is that the supervisor has a totally completely different revenue motive than the REIT. The supervisor earns charges which can be usually tied to the dimensions of the REIT and subsequently, it is going to try and develop in any respect prices, even when it dilutes shareholders and results in poor long-term returns.

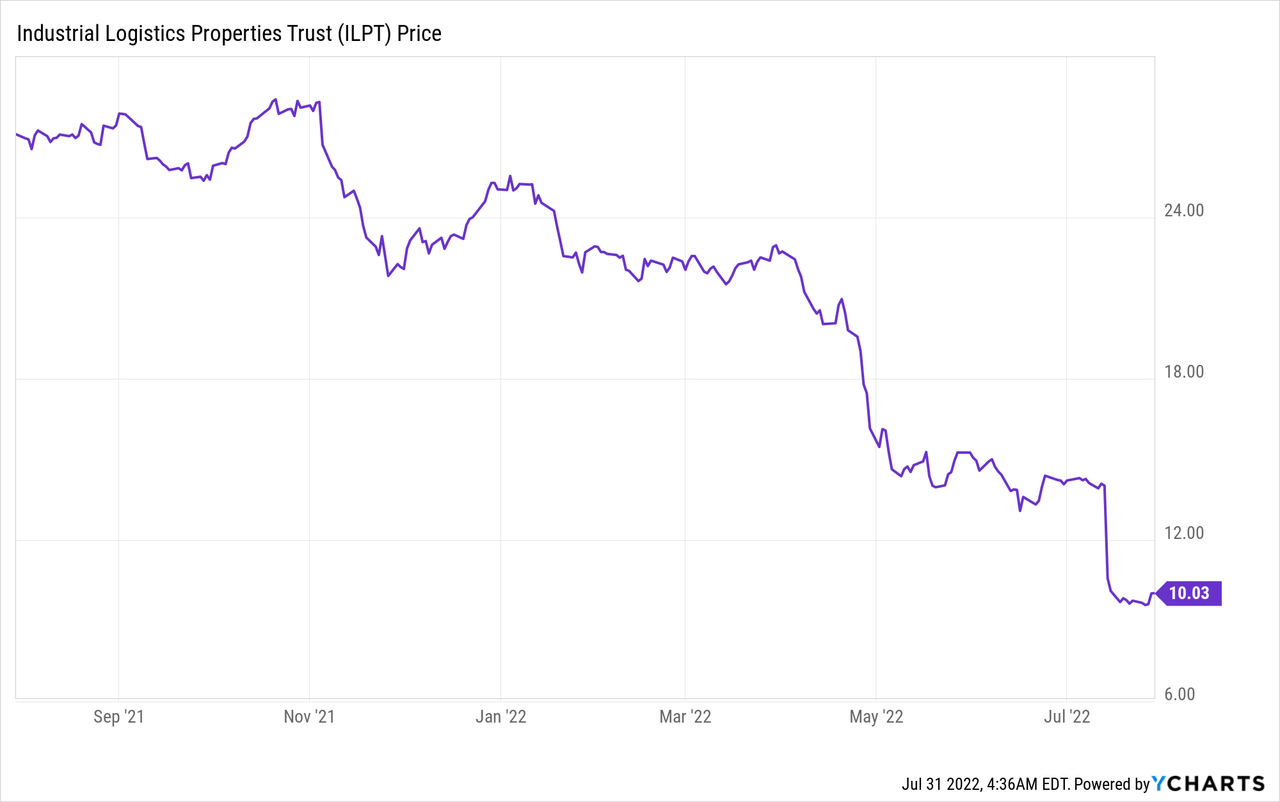

A fantastic current instance is Industrial Logistics Properties (ILPT). It’s externally managed by RMR (RMR), a notoriously conflicted asset supervisor that is solely desirous about incomes charges. Late final yr, it pushed for an enormous acquisition to develop its belongings underneath administration (and its charges) and check out the implications that shareholders suffered:

So earlier than you make investments, be sure that your REIT is managed internally. Until you observe REITs very carefully and actually know what you’re doing, merely keep away from externally managed firms.

Mistake #3: Forgetting to Examine the Steadiness Sheet

Right this moment, REIT stability sheets are stronger than ever. Their debt relative to belongings is at an all-time low of round 35% and debt maturities are additionally traditionally lengthy at 80 months on common.

It could appear counter-intuitive however research have proven that decrease debt leads to greater returns over time.

Larger leverage may also help you earn higher returns through the good years, however it could actually additionally destroy you throughout downturns, which then additionally ruins your common annual returns over a full cycle.

It’s preferable to earn considerably decrease returns through the good years, however then additionally protect your positive aspects through the downturns and even improve them by with the ability to purchase properties from distressed sellers at cut price costs.

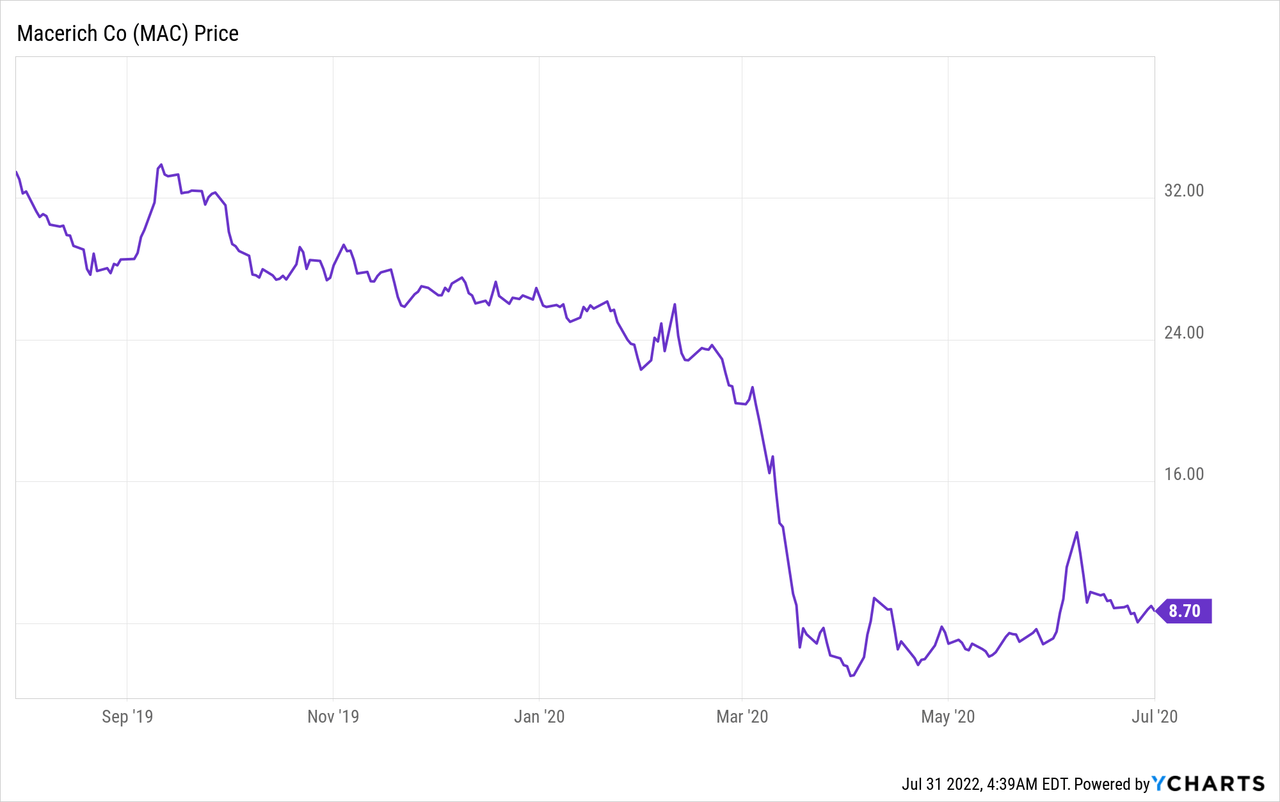

Taking the instance of mall REITs: Macerich (MAC) was overleveraged main as much as the pandemic and it pressured it to chop the dividend and situation costly fairness, diluting shareholders on the worst potential time. Its share value is but to recuperate from the disaster:

Its shut peer, Simon Property Group (SPG), had a stronger stability sheet, and it allowed it to play offense when others have been merely attempting to outlive. Its determination to take care of a stronger stability sheet has resulted in greater returns over time.

Mistake #4: Not Differentiating mREITs from eREITs

I keep in mind that my very first REIT funding was an mREIT, which stands for mortgage REIT. They’re formally structured as “REITs” however they’re very completely different from conventional fairness REITs, or eREITs.

In contrast to eREITs which put money into properties, mREITs will generally put money into mortgages and securities.

Their enterprise mannequin is way nearer to that of a financial institution than a landlord and so they additionally generally use much more leverage.

New buyers are attracted by mREITs as a result of they pay excessive dividend yields however their long-term observe file of making lasting worth for shareholders may be very poor:

Edward Jones

The problem with mREITs is that they’re closely leveraged, typically externally managed, and they’re making bets on the path of rates of interest and their spreads, that are very unpredictable issues.

Usually talking, we keep away from mREITs. We solely personal 2 of them in our Core Portfolio at Excessive Yield Landlord.

Mistake #5: Investing Too A lot in Conventional Property Sectors

The REIT sector is huge and versatile.

There are REITs for virtually all property sectors, together with farmland, billboards, and even casinos.

And but, most new REIT buyers will primarily give attention to condominium communities, workplace buildings, and different conventional property sectors.

The explanation why they put money into these belongings first is that they’ve a way of familiarity with them. For instance, they perceive that everybody will all the time want a roof over their head, and subsequently, condominium neighborhood REITs like Mid-America (MAA) ought to do tremendous over time.

The problem is that everybody is aware of this already and to earn alpha, you could put money into sectors which can be ignored and misunderstood by others.

Casinos are a very good instance. They’re perceived to be dangerous and cyclical by most REIT buyers. Regardless of that, VICI Properties (VICI), our largest REIT holding, is right this moment priced at all-time highs. What buyers seem to have ignored is that VICI leases its casinos on a long-term foundation and it has very robust leases that shield it even through the worst crises. Not even the pandemic might cease its money stream.

VICI Properties

So do not make investments simply in condominium communities simply since you are lazy to study new property sectors. One of the best alternatives are sometimes in area of interest property sectors which can be ignored by others.

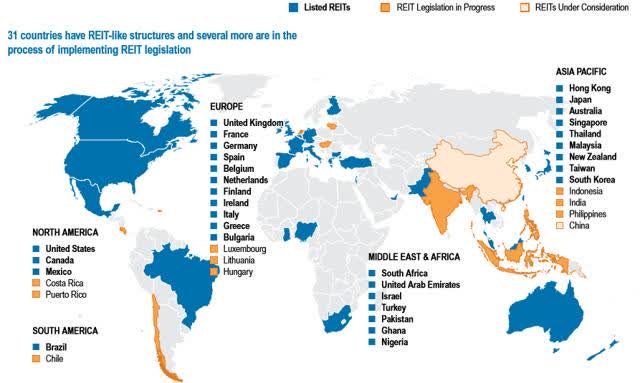

Mistake #6: Ignoring Overseas Markets

Right this moment, there are REITs in over 30 nations and but, most REIT buyers solely search for alternatives within the US.

NAREIT

By investing overseas, you possibly can increase your returns and decrease danger due to diversification.

It’s a no-brainer when you ask me.

It positive takes some effort to study international markets and discovering analysis on these alternatives is extra difficult, however it’s effectively price it.

Mistake #7: Not Paying Consideration to NAV

As a REIT investor, you will need to keep in mind that you’re shopping for actual property, and in actual property investing, the cash is made on the time of the acquisition.

Should you overpay, you already misplaced. Should you underpay, you’ve got already inbuilt a cushion of future revenue.

We pay shut consideration to the worth of the actual property that is owned by the REIT and solely make investments if we will get it at a pleasant low cost.

To offer you an instance, BSR REIT (OTCPK:BSRTF / HOM.U), a Texas-focus condominium REIT is at the moment on the market at an estimated 35% low cost relative to the worth of its belongings, internet of debt. That is a very good deal and we’re shopping for it.

The ‘Landlord’ Strategy to REIT Investing

In my early years as a REIT investor, I underperformed the market averages by making lots of the errors highlighted on this article.

However I realized from these errors and developed my very own method, which finally resulted in vital market outperformance.

Briefly:

- We observe a complete return-oriented method, in search of a very good combination of yield and progress, as an alternative of chasing yield in any respect prices.

- We solely put money into internally managed REITs with managers which have lots of pores and skin within the recreation.

- We pay shut consideration to the stability sheet to not simply develop worth, but additionally protect it throughout downturns.

- We acknowledge that mREITs are very completely different beasts from eREITs, and favor eREITs generally.

- We closely favor specialty property sectors that current higher progress, earnings, and worth for buyers.

- We put money into international markets once we can discover higher alternatives overseas. It boosts our upside and in addition diversifies our portfolio.

- Lastly, we pay shut consideration to the worth we pay. We’re worth buyers and all the time attempt to get a reduction.

We prefer to name this the “landlord” method to REIT investing as a result of we’re shopping for REITs as if we have been shopping for rental properties.

We’re very selective similar to most rental property buyers and solely put money into the easiest alternatives that the market has to supply.

[ad_2]

Supply hyperlink