")

[ad_1]

peshkov

Elevator Pitch

I downgrade my funding ranking for Devon Power Company’s (NYSE:DVN) shares from a Purchase to a Maintain. In my earlier April 19, 2022 replace for DVN, I decided that Devon Power is an effective dividend inventory. Within the present article, I contact on DVN’s current share value weak spot and talk about the place the corporate’s shares will head going ahead.

Devon Power’s inventory began dropping since June due to oil value weak spot, and the outlook is {that a} swift rebound in DVN’s share value is not on the playing cards. As such, I’ve a Impartial view of Devon Power, which interprets right into a Maintain ranking.

Why Did DVN Inventory Drop?

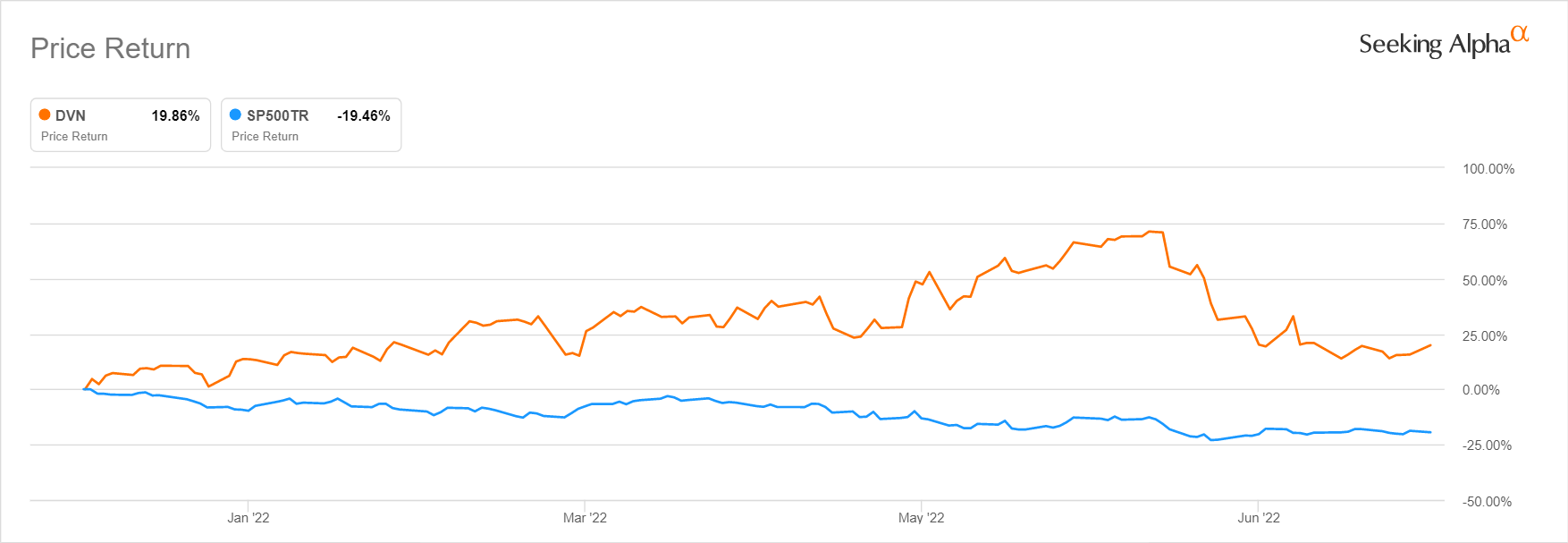

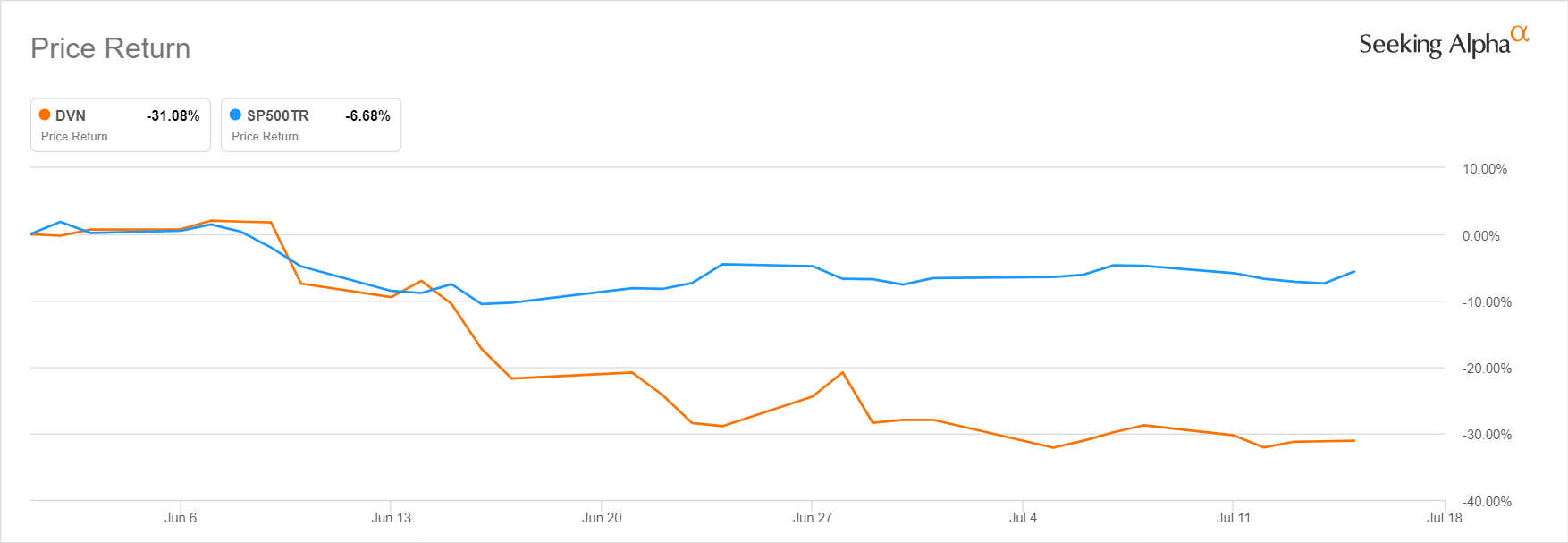

DVN’s inventory has carried out properly this yr, with its shares up by +19.9% year-to-date as in comparison with a -19.5% decline for the S&P 500 throughout the identical interval. Nonetheless, Devon Power’s shares started to offer again a few of its earlier positive aspects because the begin of June 2022. Between June 1, 2022 and July 18, 2022, the S&P 500 pulled again by -5.6%, however DVN’s inventory value dropped by -31.1% on this interval. In June alone, Devon Power’s share value fell by -27.9%.

Devon Power’s 2022 12 months-to-date Inventory Value Chart

In search of Alpha

DVN’s Share Value Efficiency Since June 2022

In search of Alpha

To grasp why DVN’s shares have dropped because the starting of June 2022, it’s price referring to Financial institution of America (BAC) analyst Doug Leggate’s feedback at Devon Power’s Q1 2022 outcomes briefing on Might 3, 2022. Doug Leggate famous at DVN’s first-quarter name that “your share value is just about flat because the oil value stopped going up in the beginning of March.” The analyst principally hit the nail on the pinnacle, as vitality shares’ short-term value actions are largely correlated with oil costs.

A July 6, 2022 In search of Alpha Information article highlighted that “Brent, U.S. crude each stoop under $100/bbl” within the early a part of this month. A mix of things reminiscent of rate of interest hikes, the strengthening US greenback, and recession fears have precipitated oil costs to development downwards previously one month or so. As such, it’s unsurprising that DVN’s shares have dropped in tandem with the correction in oil costs.

Is Devon Power Inventory Anticipated To Rise Once more?

The share value outlook for Devon Power relies on two key elements: valuations and oil costs.

DVN at present trades at a ahead free money circulation yield of 12.2% based mostly on a free money circulation of $4,241 million (the typical of the Wall Avenue’s consensus FY 2023-2026 free money circulation projections as per S&P Capital IQ) and its market capitalization of $34.Eight billion.

As a cyclical vitality inventory, I’ll deem Devon Power’s shares to be enticing at a free money circulation yield within the mid-teens share vary. In that respect, DVN’s present valuations aren’t sufficiently interesting to assist a considerable rebound in its inventory value.

Individually, the U.S. Power Data Administration or EIA diminished its 2H 2022 Brent crude oil value forecast from $108/bbl as per its prior June 2022 report to $101/bbl in its newest July 2022 replace, which it attributed to the “anticipated will increase in world oil inventories in late 2022.”

Moreover, EIA expects the Brent crude oil value to say no additional to $97/bbl and $94/bbl for the fourth quarter of 2022 and 2023, respectively. Making an allowance for the expectations of an additional pullback in oil costs, it’s unlikely that Devon Power’s shares will rebound strongly anytime quickly.

In abstract, Devon Power’s inventory is not anticipated to rise in a significant method once more within the close to future, based mostly on an evaluation of the inventory’s present valuations and future oil value tendencies.

DVN Inventory Key Metrics

Wanting past the near-term outlook for Devon Power’s shares, you will need to assessment DVN’s key metrics by way of dividends, buybacks and deleveraging disclosed as a part of its most up-to-date Q1 2022 monetary outcomes.

With respect to dividends, DVN’s quarterly dividend payout grew by +27% QoQ and +274% YoY to $1.27 per share for Q1 2022, which comprised of a variable dividend per share of $1.11 and a set dividend per share of $0.16.

In relation to buybacks, Devon Power’s whole shares excellent have declined by roughly -3% between November 2021 and Might 2022, after the corporate spent $891 million on share repurchases throughout this era. DVN had roughly $1.1 billion remaining from its present share repurchase authorization as of early-Might 2022, which signifies that the corporate has the capability to proceed shopping for again its personal shares for the remainder of 2022.

Almost about deleveraging, DVN’s objective is to additional scale back its monetary leverage from 0.6 occasions internet debt-to-EBITDAX as of end-Q1 2022 to 0.2 occasions internet debt-to-EBITDAX as of end-FY 2022. The corporate revealed at its Q1 2022 earnings briefing that it plans to “totally retire the $390 million of 2027 notes that turn into callable in October” 2022, which can assist it to satisfy its year-end monetary leverage goal.

In conclusion, Devon Power continues to make good progress on its key capital allocation priorities reminiscent of returning extra capital to shareholders through buybacks and dividends, and bettering the monetary well being of the corporate by paying down debt.

Is DVN A Good Lengthy-Time period Funding?

DVN will turn into a superb long-term funding, if there’s higher acceptance of the corporate’s variable dividend coverage and it turns into extra aggressive in allocating capital to supporting future progress.

As indicated earlier on this article, variable dividends, pegged to 50% of extra free money circulation, accounted for 87% of Devon Power’s Q1 2022 dividend payout. This suggests that DVN’s comparatively low mounted dividend payouts will not be as enticing for sure revenue traders preferring higher certainty by way of future dividend expectations.

On the firm’s Q1 2022 outcomes name, Devon Power emphasised that “what’s undervalued within the (firm’s) story is the repeatability (of enterprise efficiency and dividends)”, in its response to a query relating to “areas the place you continue to assume that traders may not be totally appreciated or appropriately rewarding you all but.”

In different phrases, it’ll take time for extra traders to be assured that the variable dividend mannequin works and variable dividend payouts are sustainable; and when that occurs, it will likely be supportive of a constructive re-rating of DVN’s shares.

Individually, Devon Power disclosed final month on June 8, 2022 that it proposed a “bolt-on acquisition within the Williston Basin” with the deliberate buy of “the leasehold curiosity and associated belongings of RimRock Oil and Fuel, LP.”

Earlier at its first-quarter earnings briefing in Might, DVN has burdened that “we have all the time had an actual excessive bar of asset purchases” and talked about that its “#1 precedence” is “returning money again to shareholders.” As such, it got here as a constructive shock that Devon Power introduced a brand new deal one month later after its feedback on the Q1 name.

Notably, a rise in M&A does not essentially translate into decrease shareholder capital returns. DVN had guided that the proposed acquisition is anticipated to be accretive and can result in a +13% progress in quarterly mounted dividends for the corporate assuming the deal closes efficiently. Wanting ahead, traders will view DVN as a extra enticing funding proposition, if it could possibly strike a superb stability between capital return and capital investments (reminiscent of M&A driving future progress).

In conclusion, DVN has the potential to be a superb long-term funding. However Devon Power must persuade traders that its variable dividend coverage will operate properly in the long term, and it is ready to allocate capital in a method that helps progress with out compromising on shareholder capital return.

Is DVN Inventory A Purchase, Promote, or Maintain?

DVN inventory is a Maintain. Devon Power has good long-term funding potential, however its shares are more likely to be range-bound within the close to future. The blended view of Devon Power explains my Maintain funding ranking for the inventory.

[ad_2]

Supply hyperlink