")

[ad_1]

olm26250

Shares of Horizon Therapeutics (NASDAQ:HZNP) are down roughly 50% from late 2021 highs, a consequence of the extended biotech bear market, and extra just lately, the expansion scare associated to Tepezza. The corporate missed Q2 income estimates and diminished the 2022 gross sales development steering for Tepezza from the mid-30s to the excessive teenagers. There was additionally an at-risk launch of generic Pennsaid 2%, however that’s extra a nuisance than a really vital impression on the corporate’s fundamentals for the reason that irritation phase was in terminal decline for a few years now and this at-risk generic launch has solely accelerated the inevitable.

I imagine that Horizon Therapeutics represents among the finest investments in biotech as we speak. The setbacks the corporate has skilled in latest months are both not vital (the Pennsaid 2% challenge) or are non permanent in nature (the Tepezza development scare), and the corporate has a number of significant catalysts that may drive continued development and a number of enlargement within the following quarters and years.

A very powerful catalyst is Tepezza returning to stronger development, pushed by the corporate’s just lately adjusted gross sales method and elevated investments to assist its development, and, extra importantly, pushed by the section Four outcomes of Tepezza within the power thyroid eye illness (‘TED’) inhabitants within the first half of 2023. There may be additionally a stealth however longer-term catalyst for Tepezza – worldwide enlargement, particularly if the corporate can discover a option to safe approval and good pricing in Europe. Retreatment is a further alternative since Tepezza is (for now) thought of a one-and-done therapy.

Secondary catalysts embrace:

- Improved gross sales momentum of Krystexxa after the latest approval for the therapy of refractory gout together with methotrexate. The mixture has achieved higher efficacy and security in comparison with Krystexxa monotherapy in a placebo-controlled trial, and Horizon is now free to advertise the mixture to rheumatologists and nephrologists.

- Pipeline hitting an inflection level in 2023 and 2024 with a number of readouts. Horizon has made appreciable efforts to increase its pipeline within the final two years and the investments ought to lastly begin to pay dividends in 2023 and past.

- Continued enterprise improvement exercise. Horizon has constructed a robust observe file of delivering shareholder worth by making good offers. Tepezza and Krystexxa are clear examples of this method with Horizon paying $145 million upfront to accumulate River Imaginative and prescient which introduced Tepezza (together with some downstream commitments) and $550 million to accumulate Crealta which introduced Krystexxa.

No funding comes with out dangers, and Horizon is under no circumstances risk-free – the primary threat being potential opponents coming to market, however as I’ll describe, the corporate is well-positioned to ship vital shareholder worth even within the presence of opponents, and I’m certain it is not going to stand nonetheless and watch different corporations threaten its management positions within the two most vital markets – TED and refractory gout.

My valuation vary is seemingly aggressive at $152 to $189, however I imagine it displays how undervalued the corporate is. And the valuation doesn’t embrace Horizon’s pipeline, which the corporate believes has the potential to generate $10 billion in annual peak gross sales. And it’ll solely increase going ahead with Horizon making further in-licensing offers or acquisitions. For the needs of my thesis, the pipeline serves as upside to my valuation vary, and alternatively, as a backup/compensating mechanism if the 2 predominant property – Tepezza and Krystexxa, don’t dwell as much as my expectations.

Tepezza is Horizon’s key asset – why I imagine it might develop to grow to be (at the very least) a $5 billion a yr product for Horizon by 2026

Horizon offered off when the corporate reported second quarter earnings, lacking the analyst consensus and decreasing the full-year income and EBITDA steering and the gross sales development steering for Tepezza.

Within the first half of the yr, the corporate observed the impression of Omicron on the expansion trajectory of Tepezza, however it, in actual fact, masked the slowing development of the product throughout this era and the post-Omicron restoration was not as robust as administration had anticipated.

In consequence, administration now expects Tepezza gross sales to develop within the excessive teenagers this yr and never within the mid-30s. Together with reiterating the boldness within the long-term outlook of Tepezza, the corporate mentioned it expects 2023 web gross sales development at the very least within the mid-teens.

That doesn’t sound like lots from the place we stand as we speak, however they aren’t assuming the potential optimistic impression of the power TED information which can be anticipated within the first half of 2023. And I imagine administration opted for a tough reset of expectations that may set the stage for the beginning of a brand new development cycle within the second half of 2022.

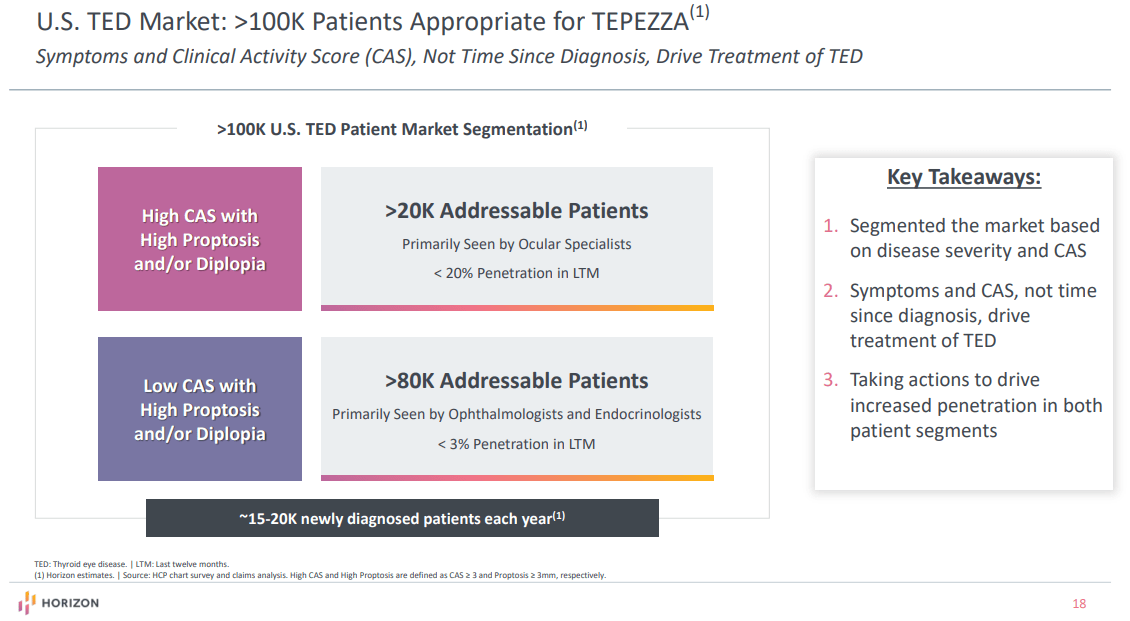

As a reminder, power TED is an on-label indication however medical information on this inhabitants are missing as a result of Horizon centered on the energetic TED inhabitants in each the section 2 and section Three trials. The information from a placebo-controlled medical trial ought to considerably enhance the boldness of all stakeholders and re-accelerate Tepezza’s development in 2024 and past.

The danger of the trial failing is low as a result of it’s the similar illness, however not within the flare-up section and there may be already respectable real-world use and case collection experiences in over 50 sufferers counsel the efficacy of Tepezza is analogous in power and energetic TED sufferers. Particularly, one examine in 31 power TED sufferers confirmed:

- 28 of 31 sufferers had diminished eye bulging (proptosis) by at the very least 2mm of their extra extreme eye (the first endpoint of the trial is a discount in proptosis).

- Of the 15 sufferers with double imaginative and prescient, 10 confirmed enhancements in double imaginative and prescient after taking Tepezza and eight of these 15 had a whole decision of double imaginative and prescient.

- All 31 sufferers with power TED had redness, swelling, and eye ache earlier than taking Tepezza, and after taking Tepezza, 28 of 31 had little to no redness, swelling, and eye ache with 18 of 31 having their redness, swelling, and eye ache fully go away.

The web page with the outcomes I linked additionally reveals the exceptional earlier than and after footage.

Total, efficacy seems similar to the efficacy noticed within the energetic TED inhabitants within the section 2 and section Three trials of Tepezza.

Worldwide enlargement is one other doubtlessly vital development driver for Tepezza. The preliminary focused market is Japan with OPTIC-J leads to the Japanese TED inhabitants anticipated subsequent yr and potential approval and launch in 2024. Horizon has guided for worldwide peak gross sales of $500 million and it expects to generate most of those gross sales in Japan.

And in all of the latest negativity, the market ignored the excellent news – the corporate mentioned on the Q2 earnings name that it’s within the strategy of assessing the launch alternative in Europe, a market the place Horizon was not prepared to go in any respect as a result of lack of orphan drug designation and pricing energy.

Past the numerous alternative within the US, we count on our world enlargement to contribute meaningfully exterior of the US starting in 2025. Whereas our present TEPEZZA peak annual web gross sales estimate doesn’t assume a launch in Europe, we’re finalizing our evaluation of that chance and count on to be ready to supply an replace later this yr. We count on this can present upside to our peak annual web gross sales expectations for TEPEZZA.

This could considerably add to Tepezza’s long-term development potential as Europe is a a lot bigger alternative than Japan.

Going again to this yr’s industrial setback in the USA, the corporate has recognized the problems and believes it might efficiently tackle them:

We perceive the dynamics impacting the tempo of development of TEPEZZA, and we’re executing on our technique to handle them, together with a extra vital enlargement of our TEPEZZA discipline power and implementing initiatives to drive additional penetration. We’re excited in regards to the future prospects for Horizon, with our development drivers, our increasing pipeline, and our world enlargement initiatives.

The elevated spending is not going to improve the general prices and there shall be a slight profit going ahead as a result of wind-down of the irritation enterprise unit within the fourth quarter.

With an annualized web gross sales run charge of near $2 billion, and with a number of development drivers within the following years, from power TED information subsequent yr to worldwide enlargement, I don’t see a purpose why this product shouldn’t considerably exceed the corporate’s peak gross sales steering of $3.5 billion (consisting of $Three billion within the U.S. and $500 million ex-U.S., primarily Japan). That’s the reason I’m sustaining my estimate vary of $5 billion to $6 billion, however with the popularity it could come later than I initially anticipated – now by 2026.

To get to $5 billion in annual gross sales, roughly 17,000 sufferers have to take a therapy course of Tepezza per yr. There are roughly 20,000 sufferers with energetic TED coming to market in the USA yearly, and the corporate estimates the power TED affected person pool in the USA is roughly 80,000 sufferers. And every of the 20,000 sufferers which can be identified yearly who don’t get handled goes into this pool and stays accessible to take Tepezza within the following years.

So, to get to $5 billion in annual gross sales in the USA alone, market penetration can be round 17-18%, assuming a web worth per affected person per yr of roughly $300,000. I ought to notice that the affected person pool shrinks as every affected person is handled, however so long as the variety of sufferers per yr doesn’t exceed 20,000, this pool will get replenished every year with energetic TED sufferers who don’t obtain a therapy course.

This isn’t an aggressive assumption as a result of the market penetration in energetic TED is already near 20% and it’s at the moment within the low single digits within the power TED market. I count on energetic TED market penetration to proceed to extend going ahead, and for the power TED penetration to rise in a extra significant means after section Four information within the first half of 2023.

Horizon Therapeutics investor presentation

And whereas the therapy course of six months is taken into account a one-and-done, some sufferers relapse, and re-treatment is one other alternative the corporate, analysts, and I will not be relying on, but. That is one other potential upside driver for Tepezza, however we’d like extra long-term information to have the ability to estimate how massive the retreatment alternative is.

Open-label follow-up information point out that 56% of responders maintained a response 48 weeks after therapy cessation. And though the affected person numbers are small at simply Eight to 9, retreatment has resulted in a 62% response charge.

With greater than 40% of sufferers relapsing a yr after the preliminary therapy course, the potential retreatment charge may conservatively be within the 20-30% vary within the first yr off-treatment. If the retreatment charge is 20% within the second yr for every affected person, this might symbolize an incremental alternative of 20% of web gross sales within the prior yr – $400 million in 2023 if gross sales are $2 billion this yr, and $1 billion if web gross sales are $5 billion by 2026.

Earlier than transferring on, I ought to notice that I described addressable market is U.S.-only. I imagine the corporate can exceed its worldwide peak gross sales steering of $500 million, simply because it did its personal preliminary steering – when it acquired River Imaginative and prescient, the corporate’s peak gross sales steering for Tepezza was solely $250 million. So, realistically, Horizon may get to $5 billion in annual gross sales by attending to roughly 14-15% market penetration in the USA and producing $Four billion in annual gross sales, and both attaining related market penetration in Japan plus the extra modest contribution from different nations to get the extra $1 billion, or low single-digit ex-U.S. market penetration if Europe is included.

I ought to add that I’m together with a possible aggressive impression within the mid/late 2020s as a number of potential opponents have emerged, attracted by the early and vital industrial success of Tepezza. However this market has room for a number of gamers, and I imagine it’s a type of that has the potential for very excessive penetration charges, and never simply to get to 15% or 20%, particularly within the energetic TED inhabitants the place Tepezza’s market penetration is already approaching 20%. Extra on potential competitors within the threat part of the article.

Krystexxa to see improved gross sales momentum after the approval of the mixture with methotrexate

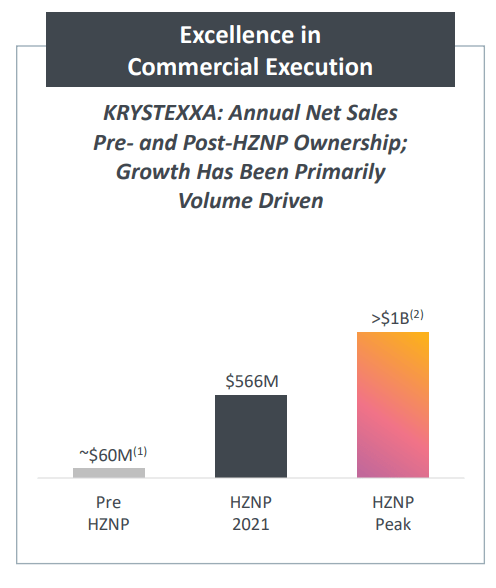

Krystexxa is an asset Horizon acquired in 2016 by means of the $550 million acquisition of Crealta. On the time of the acquisition, Krystexxa was a $60 million a yr product and it was not rising a lot, if in any respect.

Horizon Therapeutics investor presentation

Horizon has put the correct infrastructure in place, and it positioned quite a lot of effort on educating physicians in regards to the efficacy and, extra importantly, the security of the product, as a result of Krystexxa initially had a nasty fame as a result of issues of safety like extreme infusion reactions. Introducing stopping standards after the lack of serum uric acid management was important to keep away from these issues of safety.

And it later emerged that the addition of immunomodulators to Krystexxa may considerably enhance each efficacy and security and Horizon sought to generate placebo-controlled information by evaluating Krystexxa monotherapy to Krystexxa together with a well known, low-cost, and generic immunomodulator methotrexate. The outcomes have been excellent:

- Krystexxa plus methotrexate achieved a 71% response charge in comparison with a 39% response charge for Krystexxa and placebo (Krystexxa monotherapy). Full response charge is outlined as serum uric acid lower than 6mg/dL at the very least 80% of the time throughout month 6 of therapy.

- At 12 months, the response charge of the mixture was 60% versus 31% for sufferers on Krystexxa and placebo.

- Infusion reactions dropped to solely 4% of sufferers taking the mixture versus 31% of sufferers on Krystexxa and placebo.

- Amongst sufferers with validated tophi at baseline, 54% of sufferers on the mixture had a whole decision of at the very least one tophus, no new tophus, and no single tophus exhibiting development at week 52 versus 31% of sufferers randomized to Krystexxa and placebo.

These are exceptional enhancements in each efficacy and security (considerably decreased infusion reactions). The outcomes have been identified for fairly a while and physicians have responded by rising the prescribing of Krystexxa together with methotrexate, but in addition different immunomodulators, and Horizon reported that greater than 50% of sufferers have been already being prescribed the mixture. This can be a purpose to not count on an enormous gross sales inflection level.

Nevertheless, Horizon is lastly capable of promote the efficacy and security outcomes of the mixture, due to the early July approval. The considerably elevated promotion efforts ought to end in improved gross sales momentum of Krystexxa. The year-over-year web gross sales development in the previous few quarters was round 30%, and Krystexxa will seemingly generate near $700 million in web gross sales this yr. I count on it to grow to be Horizon’s second blockbuster product as quickly as subsequent yr and imagine Horizon will improve its annual peak gross sales steering of greater than $1 billion subsequent yr.

My estimate is for Krystexxa to achieve at the very least $1.5 billion and as much as $2 billion in annual web gross sales by 2026, and that there’s room for upward revisions assuming there may be development acceleration pushed by the expanded label. And there are two methods to attain gross sales development acceleration:

- Elevated variety of new affected person begins, pushed by the numerous ramp in promotion by Horizon and physicians changing into extra snug with the mixture information being included within the product label.

- With extra sufferers being prescribed the mixture, the typical size of therapy ought to proceed to pattern larger. As we are able to see within the 12-month information, the variety of responders on the mixture is double the variety of responders on monotherapy. That is vital as a result of the lack of response triggers the stopping of therapy. With the typical therapy period rising, the online gross sales per affected person ought to improve as effectively.

Extra and unaccounted-for development drivers for Krystexxa are:

- Shorter infusion time, both 45 minutes or 30 minutes versus 60 minutes. As well as, Horizon is testing each four-week administration of the mixture with methotrexate versus the prevailing each two weeks routine. I don’t count on this effort to make a big impression, however the improved comfort may provide advantages to some sufferers and inspire others to begin therapy if the dosing schedule is spaced out to each 4 weeks. These are separate open-label trials with outcomes from each anticipated in 2023.

- Retreatment. One of many points with Krystexxa is the event of anti-drug antibodies. As soon as that occurs, the affected person should cease taking Krystexxa attributable to lack of efficacy or threat of opposed reactions to the drug because the physique’s immune system begins to assault the drug. The corporate is conducting a trial the place it’s introducing Krystexxa with immunomodulators comparable to methotrexate, and it’s believed that this might result in renewed efficacy and would imply sufferers may very well be retreated with Krystexxa. Outcomes from this trial are additionally anticipated in 2023. This may very well be a big improvement and will convey again many sufferers who misplaced response or haven’t responded earlier to Krystexxa monotherapy.

With all of the concentrate on Tepezza, Krystexxa is now an ignored development asset and one that also has a protracted runway with the three above-mentioned alternatives for additional enhancement of its medical profile that would improve its peak gross sales potential in 2024 and past. Particularly, if the retreatment trial is a hit, I imagine Krystexxa’s peak gross sales potential can be at the very least within the $2 billion to $2.5 billion vary.

Pipeline investments to begin paying off in 2023 with a number of readouts

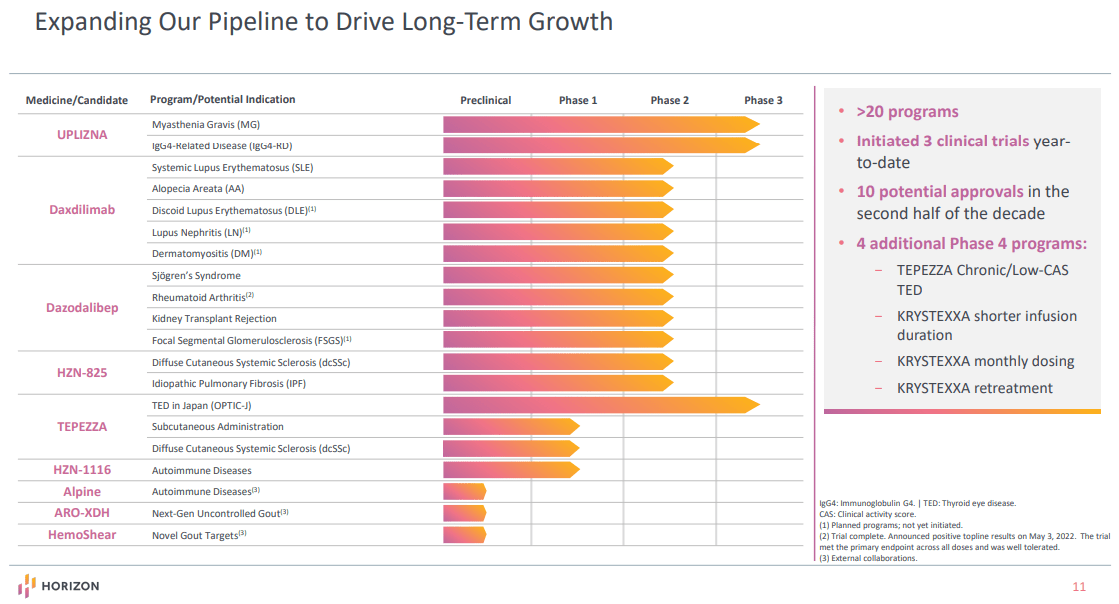

Horizon has made vital efforts to increase its pipeline within the final two years. Previous to 2020, the pipeline primarily consisted of Tepezza and the label-expansion alternatives for Krystexxa. The corporate now has greater than 20 packages with annual peak gross sales potential of $10 billion and it expects 10 potential approvals within the second half of the last decade.

The acquisition of Viela Bio final yr introduced an authorized product Uplizna, and a really respectable pipeline centered on autoimmune ailments. Uplizna itself has two further photographs on objective and dazodalibep and daxdilimab are each pipeline drug candidates with a number of indications in improvement.

The entire pipeline may be seen within the presentation slide beneath.

Horizon Therapeutics investor presentation

Since this presentation slide is a bit older, I also needs to point out the newest deal Horizon made this month. The corporate introduced a collaboration and choice settlement with Q32 Bio to develop ADX-914 for the therapy of autoimmune ailments. ADX-914 is a totally human anti-IL-7Rα antibody that re-regulates adaptive immune perform by blocking signaling mediated by each IL-7 and TSLP. Q32 has just lately accomplished a biomarker-enabled section 1 examine characterizing pharmacokinetics, pharmacodynamics, and security of ADX-914 that demonstrated pharmacological impact on T cells in wholesome volunteers. Q32 expects to provoke a section 2 trial in atopic dermatitis later this yr and is planning a section 2 trial in a second autoimmune illness subsequent yr.

Beginning in 2023, we must always begin to see the outcomes from these expansionary efforts. There are seven anticipated mid to late-stage readouts subsequent yr. Along with the readouts of Tepezza (power TED trial) and Krystexxa (shorter infusion trials, therapy each month trial versus two weeks, and retreatment trial), there further readouts are deliberate for 2023:

- Section 2 outcomes of daxdilimab in alopecia areata.

- Section 2 outcomes of daxdilimab in systemic lupus erythematosus.

- Section 2 outcomes of dazodalibep in Sjogren syndrome.

The variety of readouts ought to additional improve in 2024 as many trials are ongoing or about to be initiated quickly. Of notice are the 2 section Three trials of Uplizna in generalized myasthenia gravis and IgG4-related illness with each now anticipated to generate information in 2024 attributable to enrollment difficulties that just lately surfaced as a result of battle in Ukraine.

Dazodalibep is a fusion protein designed to focus on the CD40 ligand (‘CD40L’), thereby blocking CD40L’s interplay with CD40 and different binding companions. This has the potential to end in lowering autoimmune and inflammatory responses.

A number of autoimmune ailments comparable to Sjögren’s syndrome and kidney transplant rejection are related to the overactivation of immune cells by means of cell-cell or co-stimulatory interactions. CD40L is “a soluble or surface-bound protein expressed on T cells that interacts with CD40, a receptor protein expressed on quite a lot of immune cells comparable to B cells, dendritic cells, and macrophages.” The overstimulation of those immune cells triggered by the CD40/CD40L interplay results in an immune response cascade and overproduction of molecules that mediate irritation, leading to autoimmune ailments. Dazodalibep was additionally designed to keep away from thromboembolic unwanted side effects, which was an issue for earlier-generation monoclonal antibodies.

Dazodalibep was examined in two section 1 medical trials – a section 1a examine in wholesome volunteers and a section 1b examine in sufferers with rheumatoid arthritis. The candidate was effectively tolerated in each research with no proof of platelet aggregation that resulted in thromboembolic unwanted side effects with earlier-generation antibodies. A dose-dependent discount in autoantibody ranges was achieved and so was medical exercise in rheumatoid arthritis sufferers, which suggests dazodalibep might successfully block CD40/CD40L interplay.

The above-mentioned indications, Sjögren’s syndrome and kidney transplant rejection have been chosen for analysis. A section 2b examine in Sjögren’s syndrome was initiated in late 2019 and so was a section 2 examine in kidney transplant rejection. Outcomes from the Sjögren’s syndrome trial are anticipated in 2023.

Dazodalibep was additionally profitable in a section 2 trial in rheumatoid arthritis sufferers, however we’re but to see particulars past the topline press launch that solely famous the trial was profitable. Nevertheless, rheumatoid arthritis is just a proof-of-concept examine that was used to search out the suitable dose for future trials and Horizon will focus the event of dazodalibep on uncommon ailments and never rheumatoid arthritis.

Since buying Viela Bio, Horizon has expanded the medical program of dazodalibep to incorporate focal segmental glomerulosclerosis or FSGS, although the trial has not began but.

Daxdilimab is a humanized monoclonal antibody in improvement for the therapy of autoimmune ailments the place the pathology is pushed by the overproduction of kind 1 interferons and different cytokines secreted by plasmacytoid dendritic cells, or pDCs. Daxdilimab is designed to focus on and bind to ILT7, a cell floor molecule particular to pDCs, resulting in their depletion.

Viela has accomplished a section 1a single-ascending dose trial in sufferers with six completely different autoimmune ailments: systemic lupus erythematosus (‘SLE’), cutaneous lupus erythematosus (‘CLE’), Sjögren’s syndrome, systemic sclerosis, polymyositis, and dermatomyositis. The trial demonstrated that daxdilimab was typically well-tolerated and that it diminished pDC ranges. The section 1b a number of ascending dose trial features a cohort of sufferers with the identical ailments and separate cohorts of sufferers with CLE within the presence or absence of SLE.

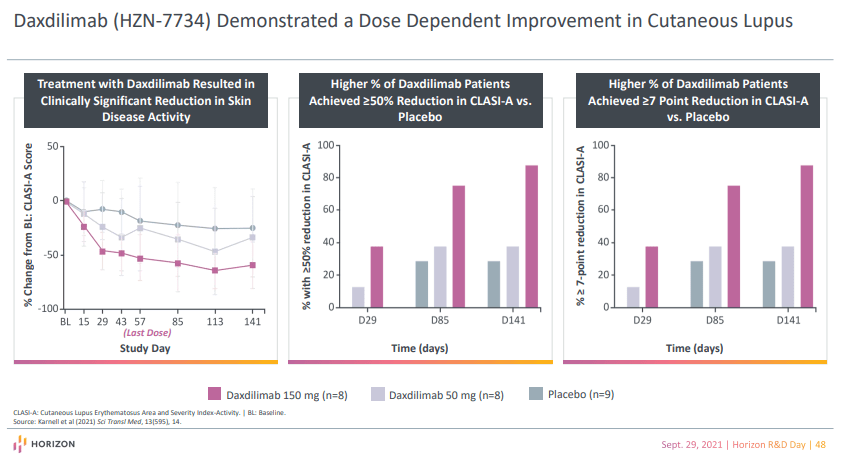

Daxdilimab successfully diminished blood and pores and skin pDCs, resulting in diminished kind I interferon ranges within the blood and within the infected pores and skin of sufferers with CLE. And extra CLE topics handled with daxdilimab than with placebo had a clinically vital enchancment within the CLASI-A scores (it is a scale that quantifies pores and skin illness exercise). Charges of opposed occasions have been related between daxdilimab and placebo teams.

Horizon Therapeutics investor presentation

Based mostly on the outcomes from the section 1b examine, Viela has chosen SLE because the lead indication and the section 2 trial and Horizon accomplished enrollment on this trial in Q2 2022, and topline outcomes are anticipated in 2023.

The rationale for the examine is that pDCs are believed to be central to the pathogenesis of SLE:

- They infiltrate goal tissues comparable to pores and skin and kidneys.

- They relocate from circulation to focus on tissues throughout SLE flares.

- They activate the immune system by means of IFN-dependent and impartial organic pathways.

For the reason that acquisition of Viela Bio, Horizon has considerably expanded the medical program of daxdilimab to incorporate the next indications:

- Alopecia areata, an autoimmune dysfunction characterised by nonscarring hair loss. A section 2, open-label trial was initiated in Could 2022. Outcomes are anticipated in 2023. The rationale for the examine is that pDCs have been detected in alopecia areata lesions and Sort 1 interferon signatures are elevated in these lesions.

- Discoid lupus erythematosus (‘DLE’), a uncommon, power, inflammatory pores and skin situation characterised by lesions that end in scarring. A section 2, randomized, placebo-controlled trial will begin quickly, and we’ll most likely see leads to 2024. Much like alopecia areata, pDCs are reported to be considerable in DLE pores and skin lesions, and Sort 1 interferon exercise current in DLE is considerably elevated in comparison with wholesome tissue.

- Lupus nephritis, a uncommon, autoimmune, and inflammatory situation of the kidney. A section 2 trial can be deliberate to begin quickly, and we’ll most likely see the leads to 2024. Horizon says that early research present decreased frequencies of pDCs within the blood and elevated numbers within the kidneys, suggesting that pDCs are recruited from the circulation to areas of energetic irritation within the kidney. Additional, pDCs product Sort 1 interferon which promotes kidney harm and is related to extra superior illness when detected in kidney tissue.

- Dermatomyositis, a uncommon autoimmune dysfunction characterised by rashes, debilitating muscle weak spot, and interstitial lung illness. A section 2 trial can be deliberate to begin quickly with outcomes no sooner than 2024. Dermatomyositis additionally shares the excessive interferon phenotype and excessive exercise correlates with illness exercise.

Daxdilimab seems like one of many highest-potential property in Horizon’s pipeline contemplating the addressable markets it’s concentrating on – if profitable in additional than two indications, its worth may eclipse Krystexxa’s within the second half of the last decade.

HZN1116 is a monoclonal antibody designed to lower the quantity and performance of antigen-presenting dendritic cells. A primary-in-human medical trial is anticipated to begin in mid-2021. There may be not a lot data accessible about this candidate.

HZN-825 got here from the 2020 acquisition of Curzion Therapeutics. Horizon paid $45 million upfront and dedicated to further funds contingent on attaining improvement and commercialization milestones.

HZN-825 was initially found and developed by Sanofi, which is eligible to obtain contingent funds and commercialization milestones, and royalties on web gross sales.

HZN-825 is being developed for the therapy of diffuse cutaneous systemic sclerosis (dcSSc), a uncommon, power autoimmune illness marked by fibrosis, or pores and skin thickening, in areas together with palms, forearms, higher arms, and thighs. In contrast with restricted types of the illness, folks with dcSSc are sometimes at larger threat of inside organ involvement, together with interstitial lung illness (‘ILD’), and kidney and bowel illness. The U.S. incidence is roughly 30,000.

In 5 section 1 research carried out by Sanofi, HZN-825 was protected and effectively tolerated and a short-term exploratory section 2a examine in dcSSc was accomplished and confirmed proof of potential medical profit in sufferers. I appeared on the outcomes (the candidate was referred to as SAR100842 when it was in Sanofi’s palms) and HZN-825 was solely numerically superior with out reaching statistical significance, however it was a small examine and of quick period (the placebo-controlled portion was simply Eight weeks).

For the reason that acquisition, Horizon has initiated the section 2b trial in dcSSc, and extra just lately, a section 2b trial in idiopathic pulmonary fibrosis.

I’ve not seen sufficient proof to essentially like HZN-825’s prospects, however each indications provide vital upside. The clinicaltrials.gov entries state each trials will full in 2023, however administration mentioned we must always not count on the outcomes earlier than 2024 for both trial.

Gout franchise within the making

I imagine that gout shall be a big franchise for Horizon within the second half of the last decade and that the expansion potential is larger than Krystexxa may doubtlessly obtain. The subsequent-generation therapies are nonetheless in preclinical improvement, however with potential to increase the addressable market.

I imagine essentially the most promising method is thru RNAi with ARO-XDH that Horizon in-licensed from Arrowhead Prescribed drugs (ARWR). As I defined in final yr’s article to subscribers, I considered this as a win-win deal for the 2 corporations. Arrowhead will full preclinical trials and ship the candidate to Horizon, and Horizon will conduct medical trials. Arrowhead obtained a $40 million upfront fee and is eligible for as much as $660 million in further improvement, regulatory and industrial milestones, and low to mid-teens royalties on web gross sales.

XDH is a genetically validated genetic goal for ARO-XDH. Heterozygous lack of perform mutation is related to a 40% discount within the threat of gout. And we must always see medical de-risking of this mechanism and goal later this yr when competitor Alnylam (ALNY) experiences section half of outcomes of ALN-XDH in wholesome volunteers and gout sufferers. The goal is similar, the mechanism is similar (RNA interference), solely the candidates are completely different and optimistic outcomes of ALN-XDH would provide a optimistic read-through to ARO-XDH and would make me incrementally extra bullish on this candidate.

There may be additionally medical validation for the goal as allopurinol and febuxostat (Urolic) are authorized for the therapy of gout, and each are xanthine oxidase (‘XO’) inhibitors. Each XDH and XO are single-gene merchandise, and so they exist in separate however interconvertible varieties. Many of the protein within the liver exists within the type of XDH the place will probably be focused by RNAi therapies, however it will also be transformed to XO.

Not like allopurinol and febuxostat, RNAi candidates are liver-specific and Alnylam believes its candidate can tackle an unmet want – potent urate-lowering with tonic management, higher security, and tolerability, and all that with rare subcutaneous dosing (seemingly each three or each six months). For the reason that mechanism of motion is similar, these are the potential benefits of the Horizon/Arrowhead RNAi candidate as effectively.

And the unmet want is there. Fewer than 50% of allopurinol sufferers obtain serum uric acid ranges beneath 6mg/dL and febuxostat has a black field warning since 2019 attributable to elevated threat of demise in comparison with allopurinol. Offered there may be superior efficacy in comparison with allopurinol together with good security, it is a multibillion-dollar marketplace for corporations like Horizon/Arrowhead and Alnylam. And superior efficacy to allopurinol is a should as there may be in any other case no marketplace for a dearer drug over a generic drug like allopurinol.

Past ARO-XDH, Horizon has a collaboration with HemoShear for the invention of latest targets for the therapy of gout and this collaboration is making progress, however particulars are scarce. And I believe the corporate will proceed to be energetic on the enterprise improvement entrance to convey new and promising modalities to positively impression the lifetime of gout sufferers.

Enterprise improvement – one other key development driver nobody is listening to recently

Horizon has constructed a robust observe file of buying and efficiently commercializing merchandise:

- Vimovo was acquired in late 2013 for $40 million and it has generated $675 million in cumulative web gross sales by means of the tip of 2021 (it’s now generic with negligible gross sales).

- Pennsaid 2% was acquired in late 2014 for $45 million, and it has generated greater than $1.Four billion in cumulative web gross sales thus far (as talked about, it too has just lately gone generic).

- Actimmune was acquired by means of the $660 million acquisition of Vidara Therapeutics in 2014. Actimmune had a big shot on objective in Friedrich’s ataxia, however it failed in a section Three trial. Nevertheless, the good thing about the Vidara acquisition was the change in tax jurisdiction to Eire and a ensuing decrease tax charge. So, this acquisition has paid off handsomely and Actimmune continues to be producing roughly $130 million in web gross sales per yr.

- Ravicti was acquired by means of the $1.1 billion acquisition of Hyperion in 2015 and Procysbi by means of the $800 million acquisition of Raptor Prescribed drugs in 2016. These two investments haven’t led to vital returns (though they’ve generated greater than $2.2 billion in cumulative web gross sales thus far), however have, together with Actimmune shaped the premise of the orphan illness enterprise, and the elevated EBITDA has led to the corporate’s elevated borrowing capability to make further offers. I might say these two offers have been reasonably profitable.

- Krystexxa was acquired by means of the $550 million acquisition of Crealta in 2015, and that is one other funding that has paid off handsomely as Krystexxa has generated greater than $2 billion in cumulative web gross sales thus far and is on observe to grow to be a $1 billion-plus product for Horizon in 2023 or 2024 on the newest.

- Tepezza was acquired by means of the $145 million acquisition of River Imaginative and prescient and a few downstream commitments in 2017. Horizon has subsequently acquired two-thirds of those downstream commitments for $110 million and it’s protected to say that that is (up to now) the corporate’s finest acquisition as Tepezza has already generated $3.46 billion in cumulative web gross sales by means of Q2 2022 and at the moment has an annualized web gross sales run charge of slightly below $2 billion.

This offers confidence that the enterprise improvement workforce at Horizon actually is aware of what it’s doing. The newer acquisitions are but to repay, however up to now, they’re wanting good.

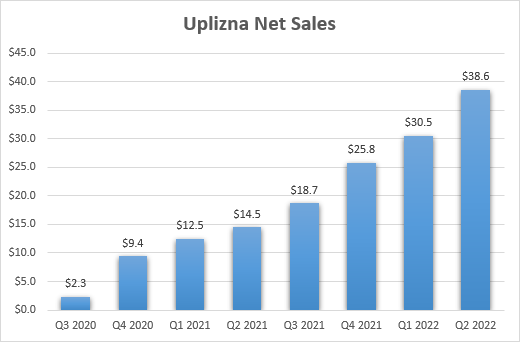

It’s too early to estimate the impression of the newest offers because the success or failure stay to be decided, and the one different bigger one is Viela Bio final yr for $3.2 billion. And up to now, this deal is wanting good as Uplizna is on observe to grow to be Horizon’s third largest product and with two further photographs on objective past the authorized NMOSD indication, and the pipeline was considerably expanded with pipeline in a drug candidates daxdilimab and dazodalibep, and there may be additionally HZN-1116 which has just lately entered the clinic.

Horizon Therapeutics earnings experiences

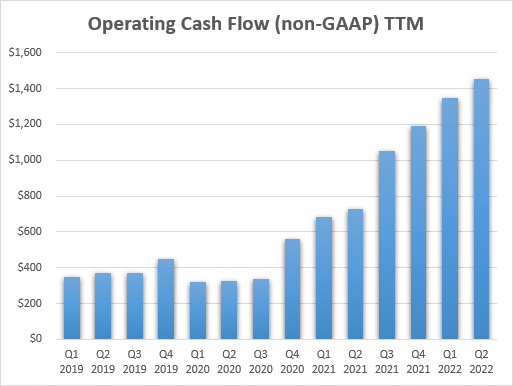

With the gross sales of Tepezza ramping in the previous few quarters, Horizon’s money flows have elevated, and this could result in continued enterprise improvement exercise and additional pipeline and/or product portfolio enlargement.

Horizon Therapeutics earnings experiences

This leaves me assured Horizon can proceed to create substantial shareholder worth, but in addition lower the aggressive dangers to its present merchandise and candidates by diversifying the product portfolio and pipeline, but in addition by in-licensing and buying merchandise and candidates that would additional strengthen the corporate’s portfolio and increase from a product like Krystexxa for gout to a gout franchise.

Dangers

No funding is risk-free and Horizon isn’t any completely different. Essentially the most vital threat for the corporate, in the long term, is competitors.

With Tepezza being Horizon’s key asset, I’ll notice that whereas no competitor is anticipated to achieve the market earlier than 2025 and doubtlessly 2026, there are some threats longer-term. Essentially the most notable risk is coming from Viridian Therapeutics (VRDN), which is creating VRDN-001 that shares the mechanism of motion with Tepezza – it too is an IGF-1R antibody.

I’m lengthy Viridian as effectively, not as a hedge on Horizon, however as a means for “pure-play” participation within the massive and rising TED market. Viridian can be creating VRDN-002 and VRDN-003, additionally IGF-1R antibodies however with an prolonged half-life and the potential to be dosed as subcutaneous injections versus IV administration of Tepezza and VRDN-001.

Viridian has just lately reported promising information from the section half of trial of VRDN-001, however the trial was small, consisting of six sufferers receiving VRDN-001 and two sufferers receiving placebo. The information have been solely out to 6 weeks, making it more durable to interpret them, however the information counsel VRDN-001 acts sooner than Tepezza because it reached larger efficacy ranges at six weeks. I absolutely count on VRDN-001 will attain the market and take market share within the massive TED market, and that’s a part of my gross sales estimate vary for Tepezza and I anticipate the TED market will additional increase with further entrants.

There are different IGF-1R antibodies in improvement, however they’re additional behind Viridian’s candidates.

However Horizon isn’t standing by and watching. The corporate is creating subcutaneous variations of Tepezza, by itself and thru collaboration with Halozyme (HALO), the go-to companion for conversion of IV-administered biologics to subcutaneously administered medicine. We’re but to listen to extra about these efforts as the corporate is protecting the small print near the chest for aggressive causes, however administration mentioned we must always see a subcutaneous Tepezza in the marketplace in 2025. I additionally doubt these efforts mark the tip of Horizon’s potential response to opponents like Viridian and different corporations creating competing IGF-1R antibodies.

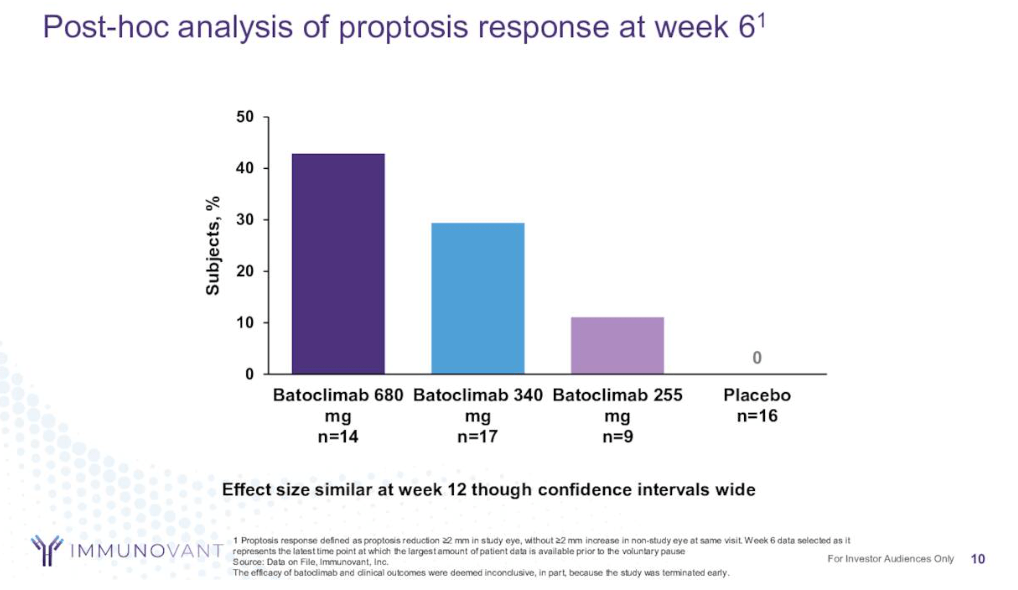

The opposite potential competitor is Immunovant’s (IMVT) batoclimab, an anti-FcRn monoclonal antibody. Nevertheless, the info Immunovant generated have been inconclusive and appeared inferior to Tepezza compared on the similar time level. Batoclimab’s proptosis response is within the 10% to 40% vary at week 6, whereas Tepezza’s is already within the mid-50s on the time and rising above 80% after 24 weeks of therapy.

Immunovant investor presentation

Immunovant itself appears conscious of the problems and whereas they declare some sufferers shall be handled with batoclimab first, its function appears to be extra applicable as a second-line therapy, for sufferers who don’t reply to Tepezza or different IGF-1R antibodies like VRDN-001.

Immunovant investor presentation

Alternatively, Krystexxa’s place within the refractory gout market seems robust and is unlikely to be threatened in a significant means within the subsequent 4-5 years. Selecta Biosciences (SELB) and companion Sobi are creating SEL-212, with the identical objective – including an immunomodulator to an antibody with the identical mechanism of motion as Krystexxa. The distinction is the antibody Selecta is utilizing is a extremely immunogenic antibody that doesn’t work effectively by itself, and the addition of Selecta’s proprietary immunomodulator ImmTOR solely brings the efficacy numerically barely above Krystexxa monotherapy ranges (54% versus 47% within the section 2 trial). And as we all know now, Krystexxa together with methotrexate has considerably higher efficacy and fewer infusion reactions than Krystexxa monotherapy. As such, I don’t see SEL-212 as a reputable risk to Krystexxa.

Essentially the most notable long-term risk to Krystexxa is Alnylam’s ALN-XDH, however Horizon too has a candidate with the identical mechanism of motion due to the collaboration with Arrowhead Prescribed drugs. Horizon and Arrowhead will not be too far behind, and it stays to be seen precisely the place this mechanism shall be positioned – upstream or downstream of Krystexxa, however I see it as earlier line remedy than Krystexxa, and the success of those candidates may truly increase the addressable market and create a gout franchise for Horizon. And Horizon is already entrenched on this market with Krystexxa, and it’ll seemingly leverage its relationships with physicians and key opinion leaders to ascertain ARO-XDH because the market chief forward of Alnylam, even whether it is considerably behind Alnylam now.

The corporate’s responses to potential aggressive threats to Krystexxa present how it’s taking a proactive method:

- The specter of SEL-212 was addressed by the addition of methotrexate to Krystexxa that resulted in a lot better efficacy than Krystexxa monotherapy and SEL-212.

- The potential long-term risk of Alnylam’s ALN-XDH was addressed by the in-licensing of ARO-XDH from Arrowhead Prescribed drugs.

And as talked about, this doesn’t mark the tip of the corporate’s efforts in gout because it has the objective of making an entire franchise with ARO-XDH, by means of the HemoShear collaboration and certain by means of further enterprise improvement exercise.

Extra dangers embrace:

- Pipeline failures going ahead. Nevertheless, at this level, there may be little to no market appreciation for Horizon’s pipeline, and this can threat will grow to be a extra pronounced threat when Horizon will get extra investor appreciation for its pipeline.

- M&A dangers – Horizon may overpay for property or entire corporations, or the merchandise or candidates it in-licenses or acquires may fail in medical trials or fail to achieve the required gross sales ranges to generate a optimistic return on funding.

- Patent expiry. However for essentially the most half, it is a reality, not a threat. The irritation phase will shut by the tip of the yr as almost all merchandise that mattered are already generic – Duexis, Vimovo, and Pennsaid 2%. Ravicti will go generic in 2025 and is not included in my valuation. However crucial product ought to take pleasure in market exclusivity effectively into the 2030s. Tepezza has biologics regulatory exclusivity till 2032, which means no biosimilar may enter the market by then, and the extra patents Horizon has or that shall be issued ought to defend its exclusivity till the late 2030s. Krystexxa’s final patents expire in 2030, however the firm is prosecuting further patents, and the addition of methodology of use patents with methotrexate ought to provide further patent safety past 2030.

Valuation and upside potential

I’m sustaining my view that Horizon is price greater than it was price at its $120 peak final yr. Sure, Tepezza’s development shall be considerably slower within the subsequent few quarters, however I’ve little doubt its development trajectory will resume within the second half of 2023 and particularly in 2024 with a higher push into the power TED market, and in 2025 attributable to worldwide enlargement.

Krystexxa stays an underappreciated asset. And so is the corporate’s pipeline and enterprise improvement capabilities, each of which ought to improve the corporate’s development profile within the following years, and particularly so within the second half of the last decade.

Horizon has all of the traits of a long-term winner. And it’s no longer buying and selling as an organization with vital development potential with a price-to-sales ratio of lower than Four and a ahead P/E of lower than 13 as of this writing. These multiples are means too low for a corporation with a development profile it at the moment has and with unaccounted-for upside drivers within the following years.

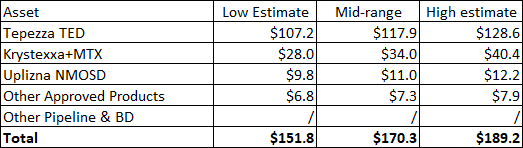

My valuation vary is $152 to $189 and is predicated on:

- Tepezza reaching $5 billion in world web gross sales by 2026 on the low finish of the vary and $6 billion on the excessive finish of the vary. This shall be achieved by continued market penetration within the energetic TED market, deeper enlargement into the power TED market, and worldwide enlargement, and regardless of opponents coming to the market.

- Krystexxa reaching $1.5 billion to $2 billion in U.S. web gross sales by 2026, though I believe this might come a lot sooner contemplating the expansion charges in the previous few quarters and the approval of the expanded label to incorporate mixture therapy with methotrexate.

- Uplizna producing $500 million to $600 million in world NMOSD web gross sales by 2026.

- Different merchandise contributing $300 million to $350 million in web gross sales. These are primarily Procysbi and Actimmune, and any residuals from Ravicti which can go generic in 2025.

The worth of every asset is summarized beneath. The valuation is predicated on the sum of the elements with a 15% annual low cost charge from 2026.

Writer’s estimates

This implies annual gross sales ought to attain $7.Three billion by 2026 on the low finish of the vary and as much as $9 billion on the excessive finish of the vary. And as lined beforehand, the valuation doesn’t embrace any further contribution from pipeline property, and I’m certain the corporate can have at the very least a couple of further merchandise on market by then, be it by means of inside pipeline progress and de-risking, or by means of M&A.

This compares favorably to the present Wall Avenue income consensus of $5.Three billion for 2026 and the analyst worth goal vary of $71 to $144. I imagine analysts are actually far behind the curve as they’re extra influenced by recency bias and damaging sentiment and don’t wish to have outrageous views in comparison with their friends. My objective is to not be conservative however as correct as potential.

Throughout the subsequent few years, Horizon may also generate billions in money circulation, and though it would seemingly spend it on M&A, the money flows within the subsequent 4-5 years may quantity to greater than half of the corporate’s present market cap of $13.7 billion, even when the present TTM charge of $1.45 billion in working money circulation is maintained.

I even have a excessive diploma of confidence that the corporate will have the ability to make up for any shortfall in Tepezza and/or Krystexxa revenues by means of present pipeline maturation and thru M&A.

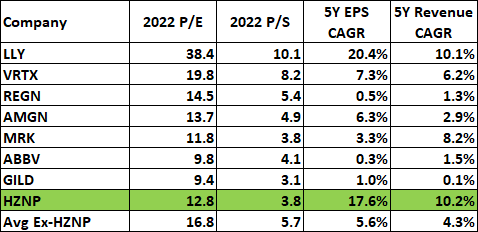

Lastly, it is unnecessary that Horizon ought to commerce at decrease or related price-to-earnings and price-to-sales multiples to massive biopharma corporations which have low or no development profiles. Beneath is a desk of such multiples and the anticipated gross sales and earnings development charges within the subsequent 5 years.

In search of Alpha, creator’s calculations

As such, I imagine that not solely the upside is important, however that draw back dangers are low – the danger of Horizon changing into a low/no development biopharma firm going ahead. It’s already buying and selling beneath the valuation vary of this group and is roughly 25% faraway from the valuation of the corporate with the bottom multiples – Gilead on the 2022 P/E aspect and fewer than 20% on the 2022 P/S aspect.

This is unnecessary in any respect, and I imagine this case is not going to persist for lengthy and that Horizon will re-rate considerably larger within the following quarters and years. It actually deserves to commerce at Vertex or Eli Lilly multiples.

With all the pieces taken under consideration, I imagine the risk-reward is very skewed to the lengthy aspect.

Horizon is among the most tasty M&A targets itself

Whereas Horizon is a serial acquirer, the corporate is changing into an more and more enticing buyout goal itself. Huge pharma is ravenous for development property and Horizon suits the invoice completely given the anticipated development and money flows it would generate within the following years, and its increasing pipeline with what the corporate claims is $10 billion in potential peak gross sales and doubtlessly 10 approvals within the second half of the last decade.

And I imagine that historic offers assist a a lot larger valuation in a buyout in comparison with the corporate’s present market cap of $13.7 billion (or enterprise worth of $14.Four billion if $700 million in web debt is included).

Taking a web page out of my latest article on the potential buyout of Seagen (SGEN) by Merck (MRK), the 5-year ahead income a number of is among the methods funding bankers use to evaluate the worth of the to-be-acquired firm. The median 5-year income a number of is 8.2, based mostly on the newest submitting of Acceleron Pharma which was acquired by Merck. Nevertheless, since these are principally youthful corporations, I argued then that Seagen is unlikely to get these sorts of multiples, and the identical applies for Horizon which can be a extra mature firm.

Making use of a 5x income a number of to Horizon’s 2027 income consensus of $5.Eight billion, I get a deal worth within the low 120s. And pushing it to 6x leads to a deal worth of as much as $145 per share.

Nevertheless, it’s arduous to think about Horizon is prepared to promote itself whereas its valuation is so depressed, and it’s also arduous to think about administration believes the present Avenue consensus is suitable. I’m certain their inside projections are at the very least in step with the decrease finish of my estimate vary, and doubtlessly above it as a result of they’re seemingly giving their pipeline correct attribution.

However any means I take a look at the state of affairs, the corporate seems considerably undervalued at present ranges and it has well-defined and vital industrial and medical catalysts in 2023, and much more so in 2024 and past.

Summarizing the catalysts within the upcoming quarters

There’s a clearly outlined path for Horizon to get again above final yr’s highs within the subsequent few quarters.

Tepezza’s return to stronger development is by far crucial catalyst for the inventory within the subsequent few quarters and consists of a number of occasions that would have a robust mixed impact on Horizon’s share worth:

- There may be now substantial doubt about Tepezza’s development potential within the subsequent few quarters, and given the depressed valuation, for the long-term as effectively. The corporate has reset expectations by decreasing this yr’s steering and for 2023 by guiding “at the very least mid-teens” income development of Tepezza. This units the stage for a collection of beat-and-raise updates within the following quarters, though extra so in 2023 than subsequent quarter, though that’s potential as effectively.

- The outcomes from the placebo-controlled trial of Tepezza in power TED sufferers are anticipated within the first half of 2023. This is a crucial catalyst as it could type the premise for development acceleration within the second half of 2023 and in 2024 as the corporate will have the ability to present the info to all stakeholders and this could improve their confidence in prescribing Tepezza to power TED sufferers which symbolize a a lot bigger inhabitants than energetic TED sufferers.

- Announcement of a sustainable path to market in Europe later this yr. That is nonetheless not a certainty, however administration hinted at this risk on the Q2 earnings name. If this seems to be the case, I count on administration to extend its $3.5 billion peak gross sales steering for Tepezza to incorporate the potential contribution of Europe which is at the very least twice as massive a possibility than Japan and different potential markets which can be included within the firm’s $500 million ex-U.S. peak gross sales steering.

- Retreatment is one other alternative that would add to Tepezza’s long-term peak gross sales potential.

Secondary catalysts embrace:

- Krystexxa’s development acceleration. Whereas I don’t count on Krystexxa to be as robust a driver of Horizon’s valuation, its contribution ought to improve going ahead as a result of just lately expanded label to incorporate mixture therapy with methotrexate which considerably will increase Krystexxa’s efficacy and improves its security. Along with the anticipated development acceleration, Horizon may also report outcomes from three trials of Krystexxa that would additional improve its medical profile – a shorter infusion trial, infusions each 4 weeks as an alternative of two, and crucial one being the retreatment trial.

- Elevated pipeline contribution in 2023. With the power TED trial readout of Tepezza, and three trials of Krystexxa producing outcomes, Horizon’s pipeline ought to begin to mature in a extra significant means in 2023 with two section 2 readouts of daxdilimab and one section 2 readout of dazodalibep.

- Continued enterprise improvement exercise. Horizon ought to proceed to be energetic on the enterprise improvement entrance to additional increase its pipeline and/or authorized product portfolio. The corporate may also not be shy to do bigger, transformational offers if the best one comes alongside. I believe the primary objective of such a transaction can be to speed up the worldwide enlargement as Horizon is at the moment principally a US-centric firm that has solely just lately began to increase with the launch of Uplizna in Europe and with the anticipated launch of Tepezza in Japan in 2024.

Conclusion

My view is that Horizon represents among the finest investments within the biopharma trade as we speak. The latest setbacks are simply that – setbacks, and the market has considerably overcompensated by sending the inventory down 50% from final yr’s highs.

Tepezza stays the important thing development driver within the subsequent few years with clearly outlined catalysts within the following quarters, carefully adopted by Krystexxa, and Uplizna’s contribution ought to steadily improve as effectively. Within the medium and long run, pipeline productiveness ought to considerably improve and end in extra merchandise reaching the market and producing further shareholder returns. To that, I ought to add Horizon’s enterprise improvement capabilities that ought to additional improve the corporate’s development profile within the following years.

Horizon itself is an more and more enticing buyout goal for growth-hungry massive pharma corporations, and if the best provide comes alongside, I imagine it’s prone to be considerably above the present ranges.

[ad_2]

Supply hyperlink