")

[ad_1]

Altayb/E+ by way of Getty Photographs

Thesis

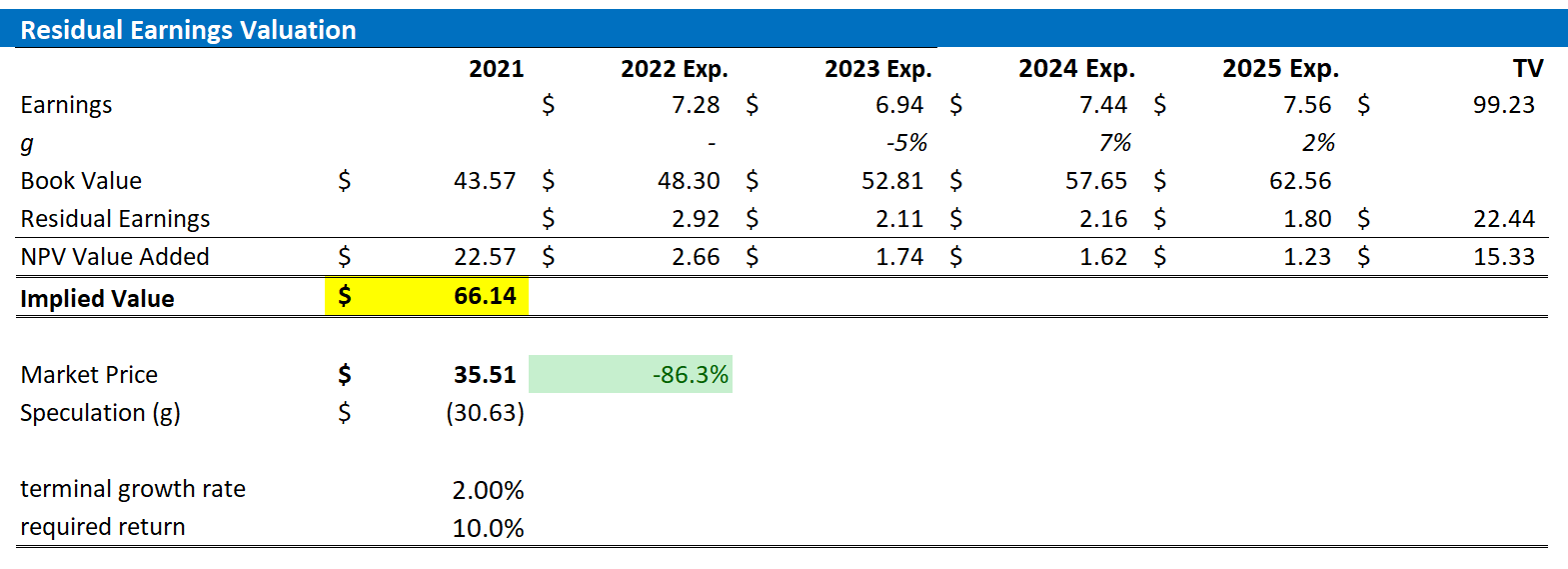

Berkshire Hathaway Inc.’s (BRK.A, BRK.B) SEC 13F submitting for the June quarter revealed that Warren Buffett is betting huge on Ally Monetary Inc. (NYSE:ALLY). Buffett elevated his stake in the corporate by 234.47%, now valued at roughly $390 million, and with a 9.7% stake within the firm. This makes Berkshire certainly one of Ally’s greatest shareholders. Is there a price thesis? The brief reply is sure. Ally trades at a one-year ahead P/E of about x5 and a P/B of beneath x1. Personally, I imagine Ally must be valued at roughly $66.14/share and I see about 85% upside. I anchor my thesis on the outcomes of a residual earnings mannequin primarily based on analyst consensus EPS estimates till 2025.

For reference, Ally inventory is down about 35% YTD, versus a lack of almost 15% for the SPX.

About Ally Monetary

To simplify, Ally is primarily centered on sourcing, structuring and working auto loans and financing throughout the mortgage cycle. In recent times, Ally has additionally pushed a digital banking initiatives and has managed to build up substantial numbers of shopper deposits.

Ally Monetary is without doubt one of the United States’ largest auto lenders and financial institution holding corporations. The corporate was based by Basic Motors (GM) in 1919 and was a subsidiary of GM till 2006, shortly earlier than the corporate wanted to be bailed out as a consequence of the monetary disaster by the US authorities.

The corporate operates 4 key segments: Automotive Finance, Insurance coverage, Company Finance and Mortgage Finance. Automotive Finance is by far Ally’s largest and most vital section, accounting for about 65% of whole gross sales. Insurance coverage is the second largest with roughly 20% of revenues. Company Finance and Mortgage Finance are chargeable for barely extra of 5% of gross sales every. Ally Financials primarily operates in the USA.

Engaging Fundamentals vs Valuation

Ally’s financials are very sturdy – it’s thus simple to see why Buffett likes the inventory. From 2018 to 2021, Ally’s revenues jumped from $7 billion to $8.9 billion, rising at a 3-year CAGR of about 8%. Over the identical interval, internet earnings greater than doubled: from $1.5 billion in 2018 to $2.9 billion in 2021 (margin 33%). Ally has not seen a fabric slowdown amidst the latest macro-economic developments. For the trailing 12 month, the corporate generated revenues of $9.four billion and internet earnings of $2.7 billion (margin 28%).

As a “financial institution,” Ally’s stability sheet shouldn’t be over-levered. As of June 2022, Ally had $140.four billion of buyer deposits and $129.Three billion of whole loans. Complete belongings had been valued at $185.7 billion.

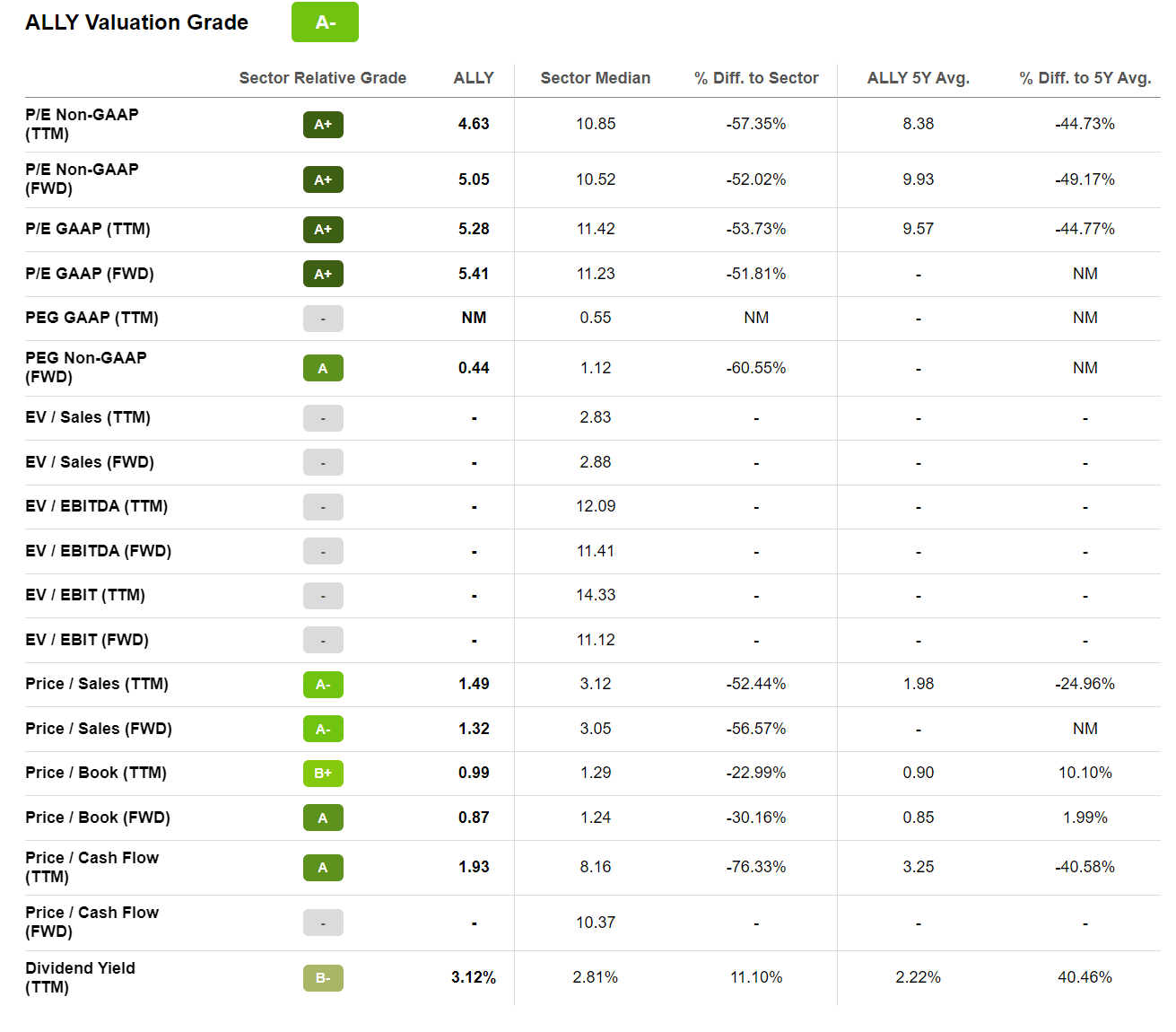

Regardless of sturdy financials, Ally is buying and selling comparatively low-cost. The inventory’s one-year ahead P/E is estimated at x5 and the P/B x0.9. these multiples usually are not solely beneath the business common, but in addition beneath All’s personal historic common buying and selling multiples for the previous 5 years. Based on knowledge by Bloomberg as of August 17, Ally’s P/E a number of versus business friends is 1.5 customary deviation beneath the 5-year historic common and as in comparison with Ally’s personal historical past, the a number of is buying and selling at a 1.7 customary deviation low cost—which signifies 30% upside.

Searching for Alpha

Residual Earnings Valuation

For my part, banks are prime candidates to be valued with a residual earnings (“RE”) valuation, provided that the RE framework anchors on each the earnings assertion and the stability sheet in addition to accrual accounting. That mentioned, I apply the next assumptions:

- To forecast EPS, I anchor on consensus analyst forecast as accessible on the Bloomberg Terminal ‘until 2023. For my part, any estimate past 2023 is simply too speculative to incorporate in a valuation framework – particularly for banks.

- To estimate the price of capital, I exploit the WACC framework. I mannequin a three-year regression towards the S&P 500 to search out the inventory’s beta. For the risk-free charge, I used the U.S. 10-year treasury yield as of August 15, 2022. My calculation signifies a good required return of about 10%.

- To derive Ally’s tax charge, I extrapolate the 3-year common efficient tax charge from 2019, 2020 and 2021.

- For the terminal development charge, I apply 3% proportion factors, roughly the nominal GDP development, which I believe is a good assumption for an business chief.

Based mostly on the above assumptions, my calculation returns a base-case goal value for Ally of $66.14/share, implying materials upside of greater than 85%.

Analyst Consensus EPS; Creator’s Calculation

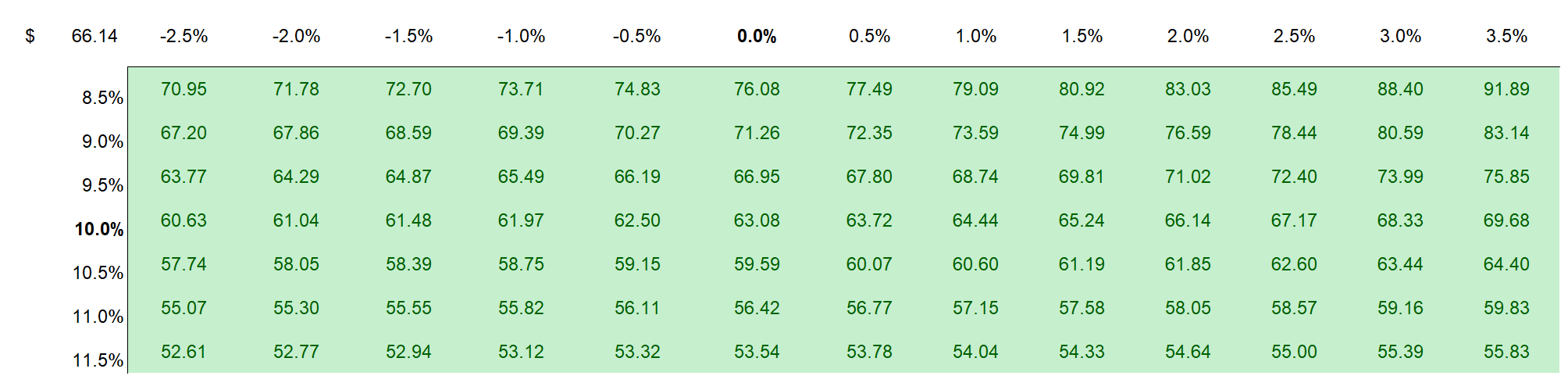

I perceive that buyers might need completely different assumptions on the subject of Ally’s required return and terminal enterprise development. Thus, I additionally enclose a sensitivity desk to check various assumptions. For reference, pink cells suggest an overvaluation as in comparison with the present market value, and green-cells suggest an undervaluation.

Analyst Consensus EPS; Creator’s Calculation

Dangers

Whereas I imagine that investments in banks are much less dangerous than the market implies, the tail-risk publicity remains to be elevated and if materialized this would possibly depreciate Ally’s share value considerably. Keep in mind, in the course of the nice monetary disaster Ally wanted to be bailed out by the federal government. Accordingly, regardless of Ally’s low-cost valuation, buyers shouldn’t be disregarding any data that may probably point out adversarial growth for Ally.

Conclusion

Warren Buffett likes to hunt for high quality corporations at an inexpensive value. And Ally Financials suits the display. Taking a look at Ally’s fundamentals in relation to its valuation, it’s no shock that the Oracle from Omaha has taken a 9.7% stake within the firm – as Ally inventory is buying and selling very low-cost. Personally, I believe Ally inventory must be pretty valued at $66.14/share. Robust Purchase.

[ad_2]

Supply hyperlink