[ad_1]

krblokhin

Earnings of Zions Bancorporation, Nationwide Affiliation (NASDAQ:ZION) will obtain help from reasonable mortgage development by way of the tip of 2023. Additional, the highest line will profit from the rising fee surroundings as a majority of the mortgage portfolio contains variable-rate loans. Alternatively, larger provision bills will drag earnings. General, I am anticipating Zions Bancorporation to report earnings of $5.89 per share for 2022, down 13% year-over-year. In comparison with my final report on the corporate, I’ve barely lowered my earnings estimate as I’ve elevated the supply expense estimate for this 12 months. For 2023, I am anticipating earnings to develop by 17% to $6.88 per share. The year-end goal worth suggests a small upside from the present market worth. Primarily based on the whole anticipated return, I am sustaining a purchase ranking on Zions Bancorporation.

Mortgage Progress to Doubtless Stay Near the Historic Development

The mortgage portfolio grew by a outstanding 2.2% fee within the second quarter of 2022 (8.7% annualized), which surpassed my expectation. Going ahead, the expansion fee will doubtless decelerate from the second quarter’s stage on account of excessive rates of interest that can curtail credit score urge for food.

Alternatively, robust job markets will doubtless maintain mortgage development. Zions Bancorporation operates in eleven western states particularly Arizona, California, Colorado, Idaho, Nevada, New Mexico, Oregon, Texas, Utah, Washington, and Wyoming. Because the economies of those states are assorted, the nationwide common is suitable for Zions Bancorporation.

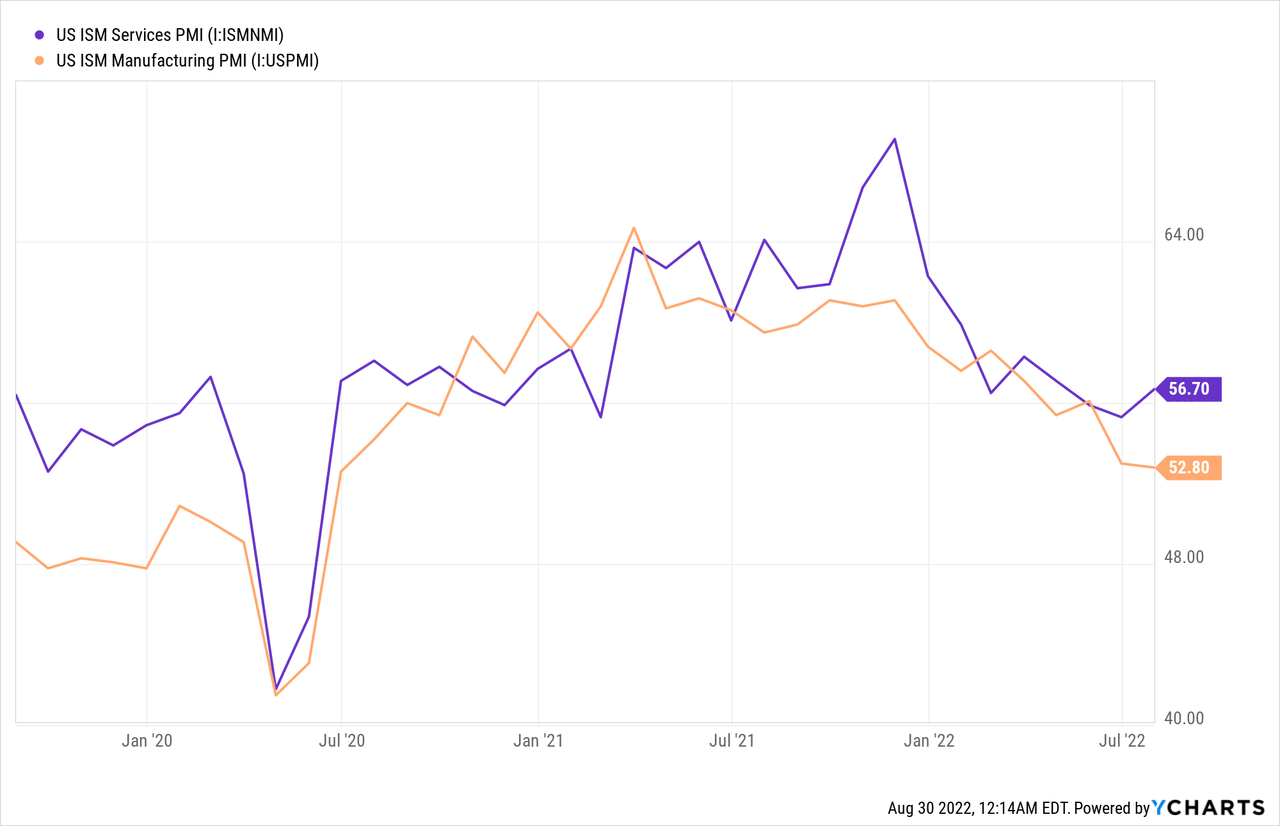

As a big a part of the mortgage guide contains industrial loans, the buying managers’ index can also be a superb gauge of credit score demand. As proven beneath, the index continues to be within the expansionary territory (above 50) which bodes nicely for industrial mortgage development.

General, I am anticipating mortgage development to return to the historic vary of mid-single digits. I am anticipating the portfolio to develop by 1% in each quarter (4% annualized) until the tip of 2023.

Charge-Delicate Mortgage E-book to Allow Margin Enlargement

The mortgage guide is sort of delicate to rate of interest adjustments as it’s heavy on variable-rate loans. Round 40% of the mortgage guide will reprice inside three months of a fee hike and one other 10% will reprice in between Four to 12 months (contemplating hedging), as talked about within the earnings presentation.

Sadly, the deposit guide can also be fairly rate-sensitive. Round 51% of the deposit guide is made up of non-interest-bearing deposits, which can make the common deposit price upwards sticky in a rising fee surroundings. Additional, securities made up a hefty 32% of complete incomes property on the finish of June 2022. This portfolio had a length of 4.Four years; due to this fact, solely a small a part of the portfolio might be anticipated to mature and re-price this 12 months. Consequently, the securities portfolio will maintain again the common earning-assets yield as charges rise.

The outcomes of the administration’s interest-rate sensitivity evaluation given within the presentation present {that a} 200-basis factors hike in rates of interest may enhance the online curiosity earnings by 11% over twelve months. Contemplating these components, I am anticipating the margin to extend by 30 foundation factors within the second half of 2022 earlier than stabilizing in 2023.

Above-Common Provisioning Doubtless for the Second Half

Zions Bancorporation reported a excessive web provision expense of $41 million within the second quarter of 2022, which negatively stunned me. Nonperforming property and accruing loans 90 days overdue made up 0.40% of complete loans on the finish of June 2022. As compared, allowances for mortgage losses made up 1.05% of complete loans. The allowance protection was passable on the finish of June; nevertheless, it is going to really feel a bit tight within the coming quarters. That is due to a excessive inflation surroundings and threats of a recession that can improve credit score threat. Consequently, I consider Zions Bancorporation should make additional sizable contributions to provisions for anticipated mortgage losses.

General, I am anticipating provisioning to be above regular for the second half of 2022 earlier than declining to virtually a traditional stage in 2023. I am anticipating the supply expense to make up 0.16% of complete loans (annualized) within the second half of 2022. For 2023, I am anticipating the online provision expense to make up 0.07% of complete loans. As compared, the online provision expense averaged 0.06% of complete loans within the final 5 years.

In my final report on Zions Bancorporation, I estimated a web provision reversal of $Three million for 2022. I’ve elevated my provision expense estimate as a result of the second quarter’s efficiency negatively stunned me. Additional, I’ve a worse credit score outlook than earlier than.

Anticipating Earnings to Dip in 2022 Earlier than Rising by 17% in 2023

Average mortgage development and margin growth will doubtless drive earnings by way of the tip of 2023. Furthermore, as talked about within the convention name, the administration is near finishing a know-how challenge that can change the present mortgage and deposit programs. Not solely will the project-related bills taper off as soon as the challenge is accomplished, however core working bills must also decline because of a extra streamlined system.

Alternatively, a better provision expense will doubtless drag the underside line. General, I am anticipating Zions Bancorporation to report earnings of $5.89 per share for 2022, down 13% year-over-year. For 2023, I am anticipating earnings to develop by 17% to $6.88 per share. The next desk reveals my earnings assertion estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Revenue Assertion | ||||||||||

| Internet curiosity earnings | 2,230 | 2,272 | 2,216 | 2,208 | 2,433 | 2,670 | ||||

| Provision for mortgage losses | (39) | 39 | 414 | (276) | 48 | 40 | ||||

| Non-interest earnings | 552 | 562 | 574 | 703 | 661 | 704 | ||||

| Non-interest expense | 1,678 | 1,742 | 1,704 | 1,741 | 1,870 | 1,941 | ||||

| Internet earnings – Frequent Sh. | 850 | 782 | 501 | 1,088 | 888 | 1,038 | ||||

| EPS – Diluted ($) | 4.08 | 4.16 | 3.02 | 6.79 | 5.89 | 6.88 | ||||

|

Supply: SEC Filings, Writer’s Estimates (In USD million until in any other case specified) |

||||||||||

In my final report on Zions Bancorporation, I estimated earnings of $5.92 per share for 2022. I’ve decreased my earnings estimate as I’ve elevated my provision expense estimate following the second quarter’s efficiency.

Precise earnings might differ materially from estimates due to the dangers and uncertainties associated to inflation, and consequently the timing and magnitude of rate of interest hikes. Additional, a stronger or longer-than-anticipated recession can improve the provisioning for anticipated mortgage losses past my estimates.

Increased Curiosity Charges Result in Fairness Erosion

Zions Bancorporation’s tangible fairness guide worth has dipped from $40.54 per share on the finish of June 2021 to $27.76 per share on the finish of June 2022, as talked about within the 10-Q Submitting. This drop was primarily attributable to unrealized losses on the available-for-sale securities portfolio. As rates of interest elevated, the market worth of the securities dropped. These losses bypassed the earnings assertion and straight lowered the fairness guide worth.

I am anticipating additional strain on fairness guide worth as I am anticipating a 75 foundation factors hike in rates of interest within the the rest of this 12 months. I am anticipating charges to be secure within the first half earlier than trending downwards within the second half of subsequent 12 months.

Alternatively, retained earnings will doubtless carry the fairness guide worth. The next desk reveals my stability sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Monetary Place | ||||||||||

| Internet Loans | 46,219 | 48,214 | 52,699 | 50,338 | 52,904 | 55,053 | ||||

| Progress of Internet Loans | 4.4% | 4.3% | 9.3% | (4.5)% | 5.1% | 4.1% | ||||

| Different Incomes Belongings | 18,836 | 16,753 | 23,553 | 37,360 | 30,378 | 31,611 | ||||

| Deposits | 54,101 | 57,085 | 69,653 | 82,789 | 80,650 | 83,925 | ||||

| Borrowings and Sub-Debt | 6,377 | 3,835 | 2,908 | 1,915 | 1,723 | 1,793 | ||||

| Frequent fairness | 7,012 | 6,787 | 7,320 | 7,023 | 5,569 | 6,354 | ||||

| E-book Worth Per Share ($) | 34.0 | 36.1 | 44.7 | 45.7 | 36.9 | 42.1 | ||||

| Tangible BVPS ($) | 29.0 | 30.7 | 38.5 | 39.1 | 30.2 | 35.4 | ||||

|

Supply: SEC Filings, Writer’s Estimates (In USD million until in any other case specified) |

||||||||||

Adopting a Purchase Ranking As a result of a Average Whole Anticipated Return

Given the earnings outlook, I am anticipating Zions Bancorporation to extend its dividend by $0.02 per share within the third quarter of 2023. My dividend and earnings estimates for 2023 counsel a payout ratio of 24%, which is near the five-year common of 28%. My dividend estimate suggests an honest ahead dividend yield of three.0%.

Zions Bancorporation’s capital ratios are presently a bit low because of the current fairness guide worth erosion. The entire risk-based capital ratio stood at 12.3% on the finish of June 2022, versus the minimal regulatory requirement of 10.5%. Nonetheless, for my part, capital adequacy necessities won’t have an effect on the dividend development subsequent 12 months.

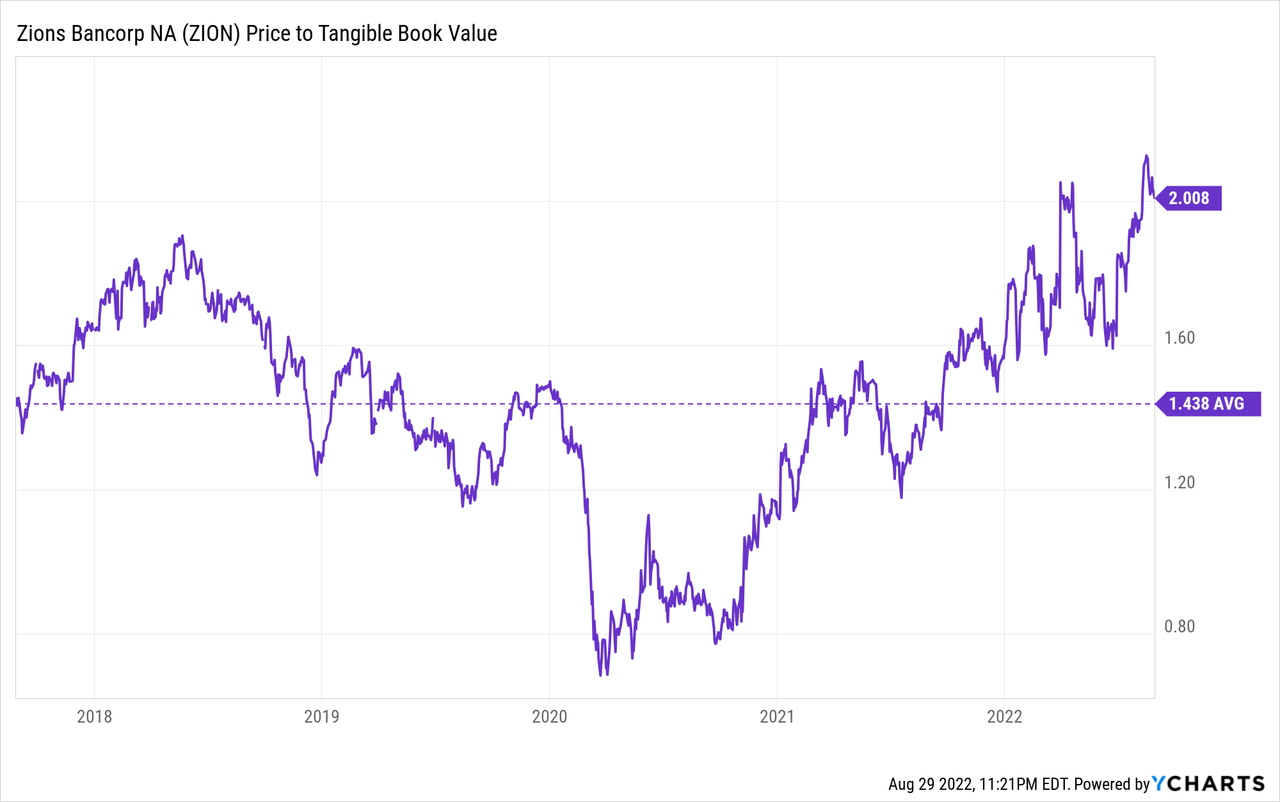

I’m utilizing the historic price-to-tangible guide (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Zions Bancorporation. The inventory has traded at a mean P/TB ratio of 1.44 prior to now, as proven beneath.

Multiplying the common P/TB a number of with the forecast tangible guide worth per share of $30.2 offers a goal worth of $43.Four for the tip of 2022. This worth goal implies a 22.1% draw back from the August 29 closing worth. The next desk reveals the sensitivity of the goal worth to the P/TB ratio.

| P/TB A number of | 1.24x | 1.34x | 1.44x | 1.54x | 1.64x |

| TBVPS – Dec 2022 ($) | 30.2 | 30.2 | 30.2 | 30.2 | 30.2 |

| Goal Worth ($) | 37.4 | 40.4 | 43.4 | 46.4 | 49.5 |

| Market Worth ($) | 55.8 | 55.8 | 55.8 | 55.8 | 55.8 |

| Upside/(Draw back) | (32.9)% | (27.5)% | (22.1)% | (16.7)% | (11.3)% |

| Supply: Writer’s Estimates |

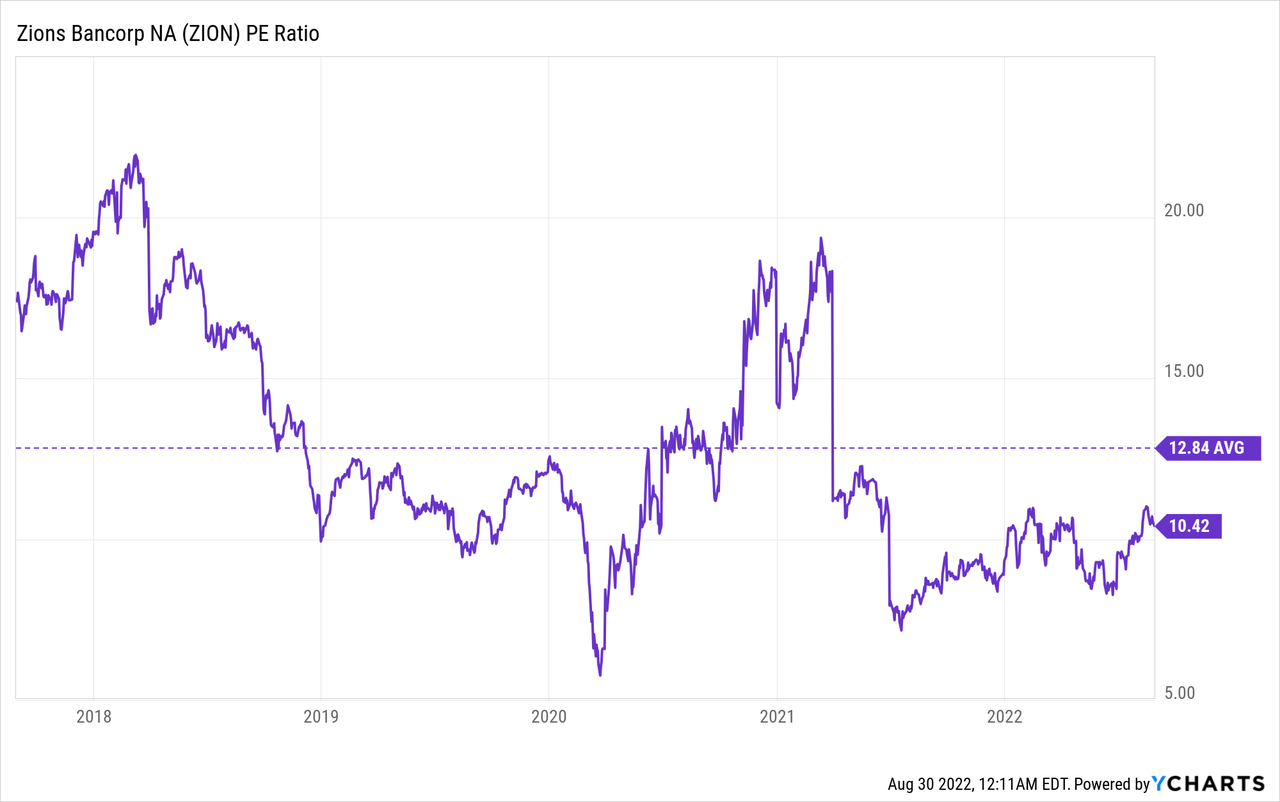

The inventory has traded at a mean P/E ratio of round 12.8x prior to now, as proven beneath.

Multiplying the common P/E a number of with the forecast earnings per share of $5.89 offers a goal worth of $75.6 for the tip of 2022. This worth goal implies a 35.6% upside from the August 29 closing worth. The next desk reveals the sensitivity of the goal worth to the P/E ratio.

| P/E A number of | 10.8x | 11.8x | 12.8x | 13.8x | 14.8x |

| EPS 2022 ($) | 5.89 | 5.89 | 5.89 | 5.89 | 5.89 |

| Goal Worth ($) | 63.8 | 69.7 | 75.6 | 81.5 | 87.4 |

| Market Worth ($) | 55.8 | 55.8 | 55.8 | 55.8 | 55.8 |

| Upside/(Draw back) | 14.5% | 25.1% | 35.6% | 46.2% | 56.7% |

| Supply: Writer’s Estimates |

Equally weighting the goal costs from the 2 valuation strategies offers a mixed goal worth of $59.5, which suggests a 6.7% upside from the present market worth. Including the ahead dividend yield offers a complete anticipated return of 9.8%. Therefore, I’m adopting a purchase ranking on Zions Bancorporation.

[ad_2]

Supply hyperlink