[ad_1]

I get questions on a regular basis from buyers, on all method of subjects. Over the previous weekend, a bunch of emails stacked up in my inbox. Many have been generated by the Federal Reserve’s announcement that extra financial ache is in retailer—and naturally the inventory market’s 1,000-point tumble on Friday, Aug. 26.

My husband thinks I’m a idiot for holding my IRA invested in shares lately. He bought most of his personal shares late final yr, and he tells me that if he hadn’t achieved that, he would have misplaced greater than $75,000.

I usually disagree with how he handles his private investments, and I’ve been cautious to verify to maintain him from managing mine. I do know we’re imagined to take the lengthy view and keep the course whereas we maintain including to our IRAs whatever the market. (My husband and I each have good salaries within the medical discipline.)

Nonetheless, he appears to have a degree. My account is down $37,00Zero up to now this yr. I hate to suppose how onerous I labored to earn that cash—after which see it vanish.

The information lately appears notably dreary, with inflation and rates of interest heating up simply when inventory costs are tumbling. My husband and I don’t discuss a lot about our investments. I requested him final evening if he’s going to maintain all his cash in money completely, and he mentioned “After all not.”

However once I requested him how he’ll know when it’s the precise time to place his a reimbursement into inventory funds, he bought an offended look on his face and ended the dialog.

Perhaps he’s proper and I’m flawed. Typically a state of affairs strays exterior the bounds of “regular,” and you need to do stuff you wouldn’t ordinarily do. Do you suppose I ought to take my husband’s recommendation?

—erplexed.

Perplexed,

First, let’s get this out of the best way: I don’t suppose you’re a idiot.

Second, you’re removed from the one investor who’s afraid that the present state of affairs could also be past the bounds of regular.

Nonetheless, I feel your husband’s method is asking for hassle. Your query to him was very astute, and his response suggests he is aware of it.

When the inventory market turns round and heads upward, that may in all probability occur when few persons are anticipating it. No person will ring a bell to announce that “all is protected.”

The reality is, no one can know that.

It’s additionally true that final Friday’s inventory market decline was startling, with the S&P 500

SPX,

down about 3%. Nonetheless, by historic requirements, that’s gentle. Within the fall of 1987, in all probability lengthy earlier than you and your husband have been paying consideration, the market misplaced 23% in simply at some point.

So my recommendation to you is straightforward: Hold doing what you’re doing. And for certain, maintain including to your IRA if that’s your plan. If something, contemplate growing your common month-to-month investments. That’s at all times a good suggestion, and when you do it now, you’ll get the benefit of shopping for property at their present low costs.

Officialdata.org

I can’t assist including this: Have some empathy to your husband. No matter you or I would consider his promoting determination, it was an try to attain some peace of thoughts. Apparently he has achieved it—at the least for now.

Sadly, when the market begins to get well and his portfolio remains to be in money, peace of thoughts could elude him. No matter he does at that time, it’s prone to really feel flawed—and there’s no straightforward method out.

That’s when chances are you’ll be tempted to remind him that emotion-driven selections nearly at all times produce grief. I hope you’ll resist that temptation, as a result of he’ll determine this out for himself.

Expensive Paul,

My son, who’s 31, has currently come into some cash, about $20,000, from his aunt and uncle. He has requested my recommendation on the way to make investments it, however solely after the market stops falling.

I attempted to inform him {that a} falling market is an efficient time to speculate, as a result of costs are typically decrease. You already know, the entire “purchase low and promote excessive” factor. However he isn’t comfy doing that and desires to carry off.

What ought to I inform him?

—Wish to be mother

Expensive Mother,

As you undoubtedly have noticed, many individuals must be taught essential classes the onerous method. Your son could also be in that spot now.

You’ll be able to present him my reply to the earlier query. You’ll be able to lecture him all you need, and in the long run he’ll do what he’s going to do. Presumably, your son could have that cash invested for at the least the following 30 years, and fairly probably longer.

With that in thoughts, I’ve two concepts for you.

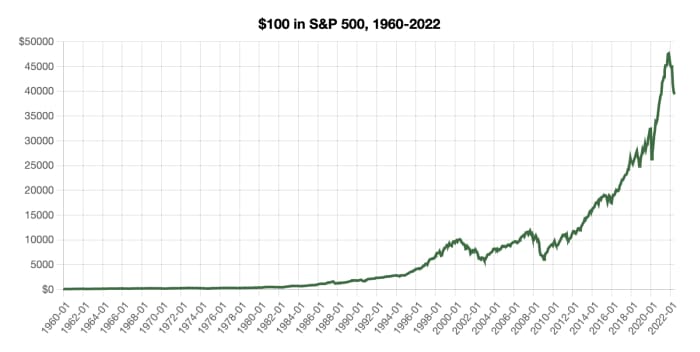

First, discover a line graph of the U.S. inventory marketplace for the final 60 years or so. It should present the ups and downs, with just a few noticeable dips in years like 1974.

Ask your son to look again at these previous instances when the market suffered main losses, and to contemplate that mid-2022 will doubtless grow to be a kind of intervals.

Wanting again, would he have suggested anyone in 1974 to carry off? Or can he see that, practically half a century later, 1974 would which were a wonderful time to speculate cash?

The purpose is that this: The long-term bias of the market is upward, and bear markets have at all times introduced shopping for alternatives for long-term buyers.

Second, give your son a replica of the e-book referenced on the backside of this text. It should present him that success is made from many substances which are far more essential than what the market is doing at any given time.

You’ll be able to’t make your son do one thing he doesn’t wish to do. However you wish to be mother, and my solutions will enable you do this.

Learn to shake up your monetary routine on the Greatest New Concepts in Cash Competition on Sept. 21 and Sept. 22 in New York. Be part of Carrie Schwab, president of the Charles Schwab Basis.

Richard Buck contributed to this text.

Paul Merriman and Richard Buck are the authors of We’re Speaking Thousands and thousands! 12 Easy Methods to Supercharge Your Retirement. Get your free copy.

[ad_2]

Supply hyperlink