[ad_1]

Credit score union earnings have been flat within the second quarter regardless of report mortgage manufacturing and rising web curiosity margins, Callahan & Associates reported Wednesday.

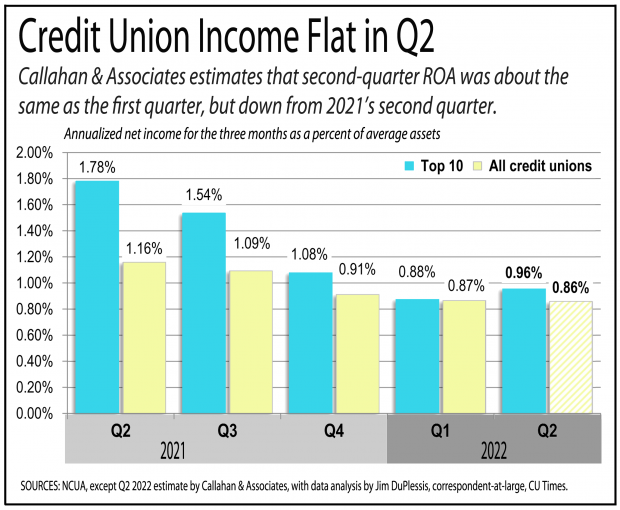

Through the Washington, D.C., credit score union firm’s quarterly Trendwatch webinar, it confirmed credit score unions’ web earnings was an annualized 0.86% of their common property within the second quarter, down from 1.16% a 12 months earlier and 0.87% in the primary quarter.

The decline from a 12 months in the past was associated to low provisions for mortgage losses in early 2021 as credit score unions reclaimed overly pessimistic provisions made in 2020 initially of the COVID-19 pandemic. Outcomes for the primary and second quarters have additionally been lowered by heavy write-downs in funding property to mirror market downturns.

However the underlying developments have been optimistic.

Web curiosity margins have been 2.66%, up from 2.53% a 12 months in the past and a couple of.57% within the first quarter.

Credit score unions originated a report $412.7 billion in loans within the three months ending June 30, up 6.2% from $388.7 billion in 2021’s second quarter and $192.Three billion within the first quarter.

Actual property originations have been $174.Three billion, down 1.5% from $177 billion a 12 months earlier. Nonetheless, non-real property originations, which embrace autos and different shopper loans, rose 12.6% to $238.Four billion.

Oblique lending contributed to a spike in auto lending. Credit score unions’ stability of whole oblique loans on June 30 was 24.4% larger than a 12 months earlier, its highest annual progress fee in not less than 5 years.

Credit score unions offered about $17.Eight billion in first mortgages to the secondary market, or 14.4% of mortgage originations. It was on par with first-quarter gross sales of $17.6 billion, however down from about $30 billion in 2021’s second quarter. Gross sales peaked within the fourth quarter of 2020 at 37.2% of mortgage originations, however have been declining since as rising rates of interest have lowered quantity and the profitability of gross sales.

Credit score unions have additionally been shopping for fewer mortgage participations as their natural mortgage progress has accelerated. Credit score unions purchased $8.5 billion in mortgage participations within the second quarter, down from $9.Four billion within the first quarter, however up from $6.Four billion in 2021’s second quarter.

Through the top of the COVID-19 pandemic financial savings have been rising at double-digit annual charges, whereas loans have been rising a lot slower. This 12 months the other pattern has been true. The 12-month acquire in mortgage balances was 16.2% by June 30, whereas financial savings grew 8.2%.

Consequently, the loan-to-share ratio spiked to 74.7% as of June 30, up from 70.1% a 12 months earlier and 70.6% on March 31.

Greater than 5.5 million individuals joined a credit score union prior to now 12 months. Membership rose 4.3% to 134.1 million.

Credit score unions employed about 347,600 full- and part-time staff on June 30, up 4.8% from a 12 months earlier.

The typical credit score union member had a complete of $23,379 in loans and financial savings with their credit score union, a “relationship” worth that’s 6.3% larger than a 12 months earlier. The typical loans per member was $9,386, up 9.5% from $8,575 a 12 months earlier, whereas the common shares per member rose 4.4% to $13,993.

[ad_2]

Supply hyperlink