[ad_1]

Iurii Garmash

Power shares have been the primary sector available in the market to this point in 2022, and this follows upon its primary efficiency in 2021. What ought to we make of that and what does it portend for the longer term? We should always most likely begin with the truth that vitality was the worst performing sector in 2020. There are two methods of taking a look at this. It could be straightforward for traders to resolve that the 2021-2022 efficiency by vitality shares is just a part of an enormous catchup rally which will now have overshot the mark. Power shares had fallen to a degree the place they have been grime low cost, in accordance with this view, and have since recovered to a degree the place they’re absolutely priced. The opposite standpoint is that one thing elementary has modified within the vitality market and the rally beginning in the midst of 2020 was only the start because the market progressively acknowledged the implications of that change. Deciding which manner to have a look at the 2 12 months monster rally is the important thing to understanding whether or not vitality continues to be a great purchase proper now.

The connection between vitality shares and extremely risky oil costs is much less necessary than it has been over the previous decade. Most oil and gasoline corporations have taken benefit of the excessive costs over the primary half of 2022 to restore their steadiness sheets and cut back monetary leverage. That is true of all of the shares talked about on this article. All can function profitably and supply strong future shareholder returns at costs across the common worth for 2021 which was about $68 per barrel. That is most likely within the low finish of the band upon which oil corporations base their ahead expectations. Costs bouncing round $90 per barrel most likely don’t be concerned vitality firm CEOs to almost the diploma that brief time period volatility appears to fret traders and the market. The underlying assumptions for corporations talked about on this article are roughly based mostly on 2021 oil costs and stage of volatility.

Power Sector Efficiency Over A number of Time Frames

On April 20, 2020, the expiring worth of WTI futures dropped to unfavorable $37 per barrel in order that in idea the futures market was prepared to pay you $37 to make a barrel of oil go away. Each long run and brief time period elements led to that second of unfavorable oil worth. Going into 2020 the dominant long run narrative was that carbon vitality was in a secular decline. The foremost oil corporations have been just about written off as corporations in run-off. It would not have been the primary business to undergo that destiny. Within the 19th century, 90% of American staff have been farmers. At this time the quantity concerned in farming has fallen to 1%. That is what secular decline appears like. We nonetheless have farms, after all, however they’re vastly bigger in scale. Over a interval of 100 years this form of decline is nearly definitely the way forward for carbon vitality, however the query for traders is whether or not that decline is measured in a couple of years or a couple of many years. The probabilities are superb that carbon vitality will nonetheless be round and produced by companies working on the current mannequin for many years.

By early 2020 the mega-cap oil majors have been beleaguered on all sides. Inexperienced vitality activists have been making proposals at annual conferences and looking for seats on their boards. Three really gained seats on the board of ExxonMobil (NYSE:XOM) in 2021. The oil majors have been straightforward targets for political leaders due to their longstanding denial of local weather change. Unfriendly authorities insurance policies have been on the way in which. Then in February 2020 the COVID pandemic appeared and successfully shut down the economic system. The enterprise of main clients like airways fell radically in order that decrease costs have been compounded by decrease quantity. The ultimate straw was the OPEC worth warfare within the first half of 2020.

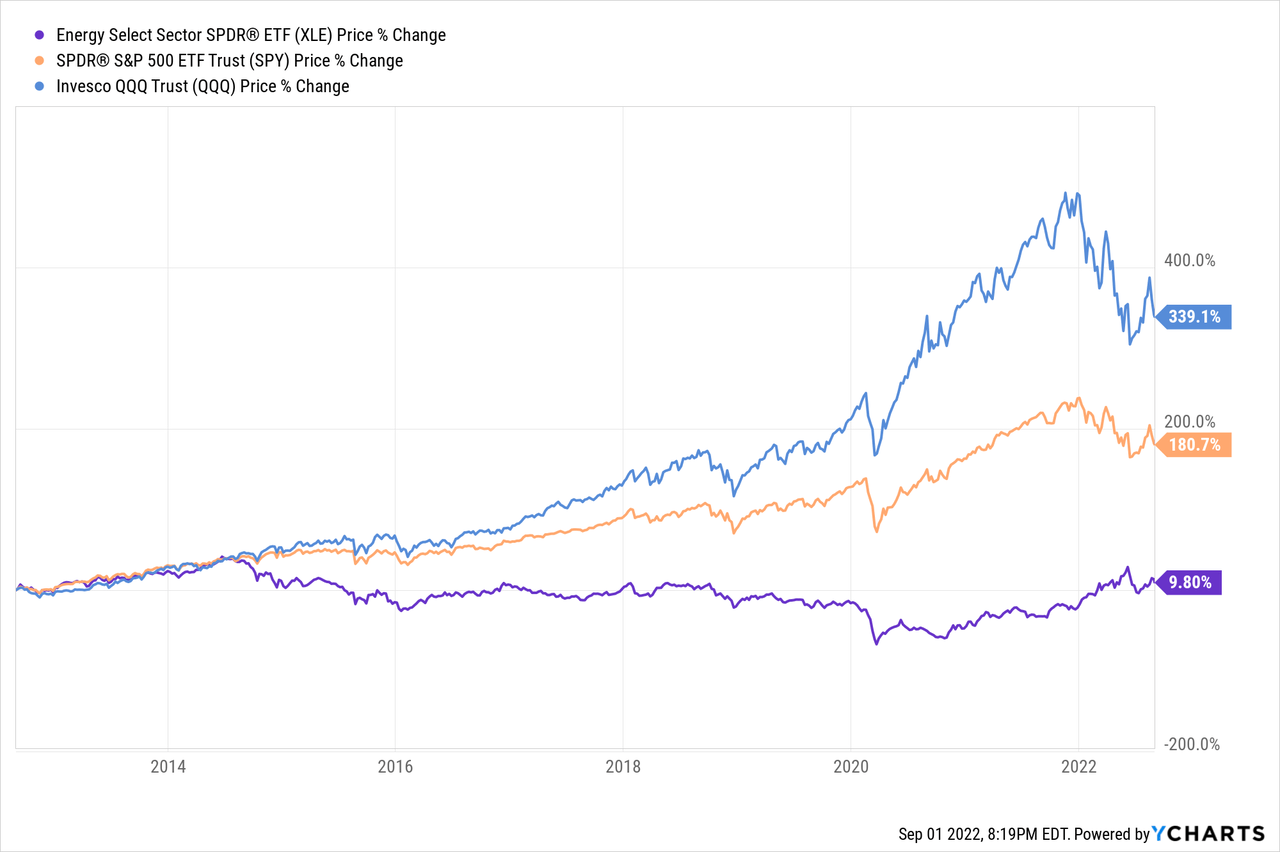

These elements all contributed to the vitality crash in April 2020, however within the longer perspective essentially the most critical problem to the oil majors was the straightforward impossibility of changing their reserves. An vitality firm which might’t change the oil it processes and sells finally goes out of enterprise. On March 29 I wrote about this downside intimately. The brief model is that the 4 largest worldwide oil majors spent $11.5B from 2010 to 2020 versus $6.5 billion from 2000 to 2010 to seek out roughly the identical $40 billion of reserves. All 4 failed to take care of their stage of reserves, and as a gaggle they changed solely 85%. That strongly means that the oil majors are actually within the early stage of the run-off part. The ten-year chart under compares the Power Choose Sector Spider (XLE) to each the S&P 500 (SPY) and the tech-heavy Invesco QQQ Belief (QQQ). What it exhibits is the truth that vitality fell steadily behind the broader market with know-how shares being the large winner.

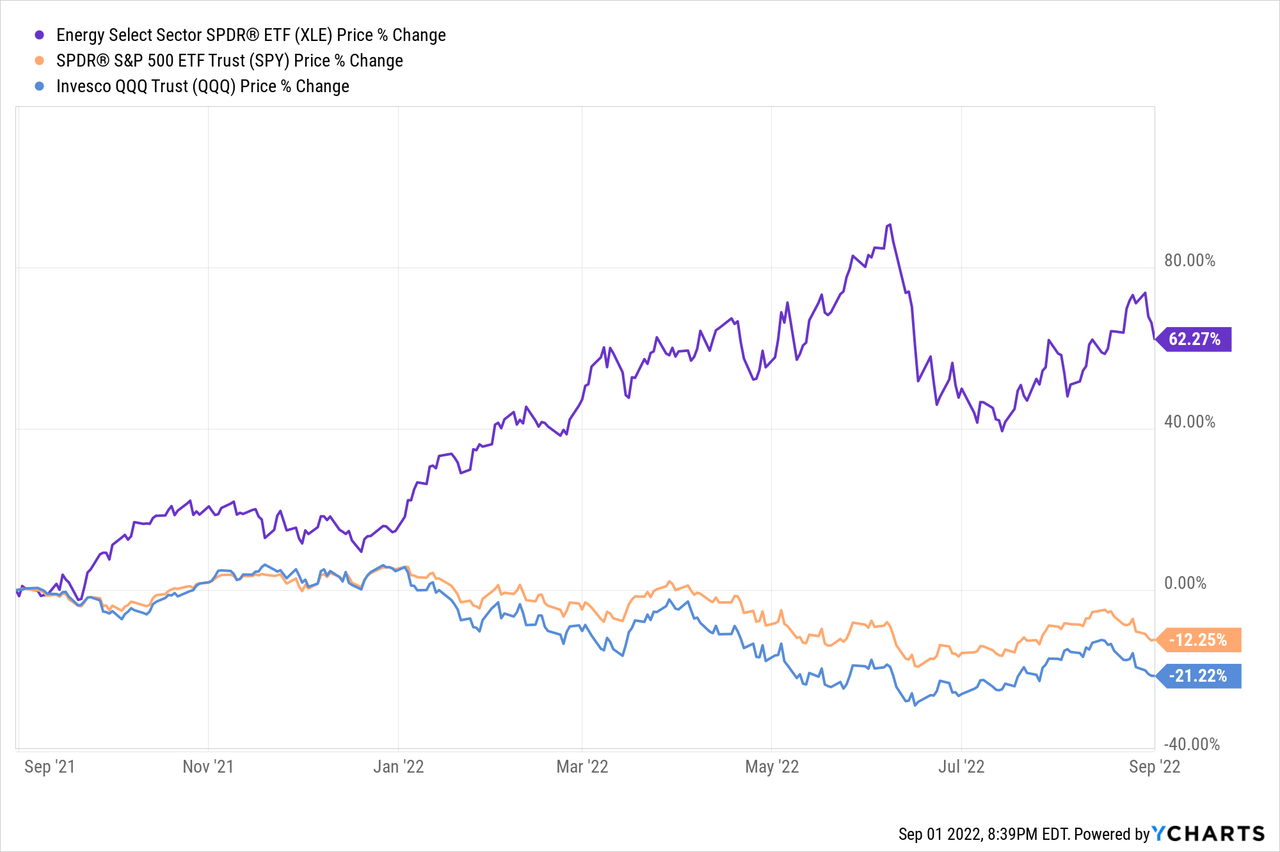

The sharp dip in all three charts exhibits that by March 2020 most traders had thrown within the towel on vitality. I can not recall any predictions at the moment that the vitality sector would lead the market over the subsequent two years, however that is precisely what it did. Does it make any sense that the vitality sector has rallied furiously for 2 years beating know-how and all different industries? Trying intently on the chart you’ll be able to see that after two years of main the market, vitality continues to be effectively under its stage in 2014 when oil costs have been about the place they’re proper now. What does that imply for traders who’re contemplating vitality shares proper now? The chart under exhibits simply how powerfully vitality shares rallied over the previous 12 months and seized market management whereas the market as a complete, with draw back management by tech, was sinking.

To this point in 2022 (as I write this line) the Power Choose Spider ETF (XLE) is up about 40% for the 12 months after having been up as a lot as a lot as 60% at its June peak. For 2021 it was up 54%. Since its low level in March 2020 the XLE is up 200%. From its low level in November 2020 the proportion weight of vitality within the S&P 500 has greater than doubled from slightly below 2% to only over 4.4%. It is price noting that in historic phrases that is nonetheless a small quantity because the market is accepting the brand new vitality story with some hesitancy.

The truth that the vitality sector bucked the market down pattern carries necessary info. The fast assist for vitality outperformance is that the working outcomes of oil and gasoline corporations have additionally outperformed. Current Wall Road projections have the vitality sector offering about 10% of S&P 500 earnings in 2022. It is hitting far over its 4percentish weight. This piece by Factset notes that whereas S&P 500 earnings have been up 6.7% for the primary half of 2022 they’d have been unfavorable 3.7% with out vitality.

On the very least the narrative predicting the fast demise of carbon vitality has been proven to be exaggerated. In his 2020 Shareholder Letter, Warren Buffett, a powerful supporter of going inexperienced rationally, identified the difficulties in delivering renewable sources to the big cities that are the most important customers of vitality. Buffett ought to know, having taken no dividends from Berkshire Hathaway’s (BRK.A)(BRK.B) BHE unit whereas it devotes all of its earnings to developing the required grid for renewables. Buffett’s goal date for finishing this challenge is 2030 and BHE has a considerable head begin in comparison with different utilities. The inescapable implication is that whereas using carbon vitality will decline within the very long term, the decline might be gradual. Nothing may have put this in focus extra clearly than the provision squeeze stemming from the Russian invasion of Ukraine.

The premise of this text is that oil and gasoline will proceed to be the most important supply of vitality for fairly some time – lengthy sufficient for present vitality traders to do extraordinarily effectively. The narrative of carbon vitality’s secular decline bought a few many years forward of itself. The foremost alternative lies in the truth that even after a robust rally the positives within the vitality narrative appear to not be absolutely factored into vitality inventory costs. Bucking the pattern in what more and more appears like a bear market is a robust trace that the vitality shares could proceed to be leaders within the subsequent bull market.

Is Now The Time To Purchase Power Shares?

Considered one of two key questions is the way to weigh the a number of time frames at work with oil and gasoline and the vitality sector. Within the longest time-frame the vitality sector has fallen from a bloated 28% in 1980, when it had been the chief for the lengthy 1970s commodity inflation cycle. That 28% was a transparent overshoot, and people who thought that vitality shares solely went up have been in for an enormous disappointment. Beginning in 1980 most elements of the market did higher. In 2000 the burden of vitality rallied again to 15% and it tagged that 15% stage once more in 2010. Since then, whereas tech led the market, vitality stalled after which fell under 2% in November 2020. It’s round twice that immediately. In the long term vitality will lose floor to technological innovation, however for the second it seems to be tech which is overextended whereas vitality makes a comeback.

The necessary query for traders is whether or not the 2020 reversal needs to be considered as a serious turning level. Are we about to see a sequence of long run highs in vitality costs or do present vitality costs merely mirror a variety of brief time period elements? The very issue of changing reserves and the comparatively modest current capital expenditures for exploration and manufacturing counsel that such a long run turning level was due. The goal will not be the 28% S&P weighting of 1980 however it may method the 15% of 2000 and 2010.

What this implies is that within the longer perspective, vitality shares are most likely low cost. That being stated, it is normally clever to be prudent when the value of an asset has lately tripled because the Power Choose Sector ETF has accomplished since April 2020. The current market could also be within the strategy of offering a dip-buying alternative as vitality has succumbed to the final market slide for the previous few days. Traders may look ahead to a chance to purchase in the midst of the current market correction.

Chevron (NYSE:CVX) or ExxonMobil For Revenue Traders

The query of what to purchase relies upon to some extent on an traders targets and threat tolerance. The 2 largest positions within the Power Choose Sector ETF, making up greater than 45% of XLE holdings, are ExxonMobil and Chevron. Whereas some traders may be attracted by the diversification of XLE, each Chevron and Exxon have greater yields at 3.6% and three.7% respectively and seem capable of proceed rising their dividends for the foreseeable future. SA Dividend Rankings give CVX an edge with Dividend Security at B-, Dividend Progress at B+, and Consistency at A+, all three a notch above XOM. Buffett seems to suppose so too, having established a big place in Chevron, greater than $26B per Berkshire’s final report.

The draw back is that the vitality mega-caps don’t have any progress in quantity, with current enchancment in metrics being pushed by rising oil costs. One must also not overlook that the vitality mega-caps have been unable to interchange their reserves and each have income strains reflecting a long run decline. Chevron touches out Exxon once more in SA Issue Rankings with an edge in Worth as XOM has lately gone up extra in worth. Chevron is also rated a notch higher for Progress. Each obtain Quant Rankings of Robust Purchase. XOM is ranked #1 of 19 Built-in Oil and Gasoline Shares with CVX rated #4, however the distinction within the numerical rating is 4.99 (out of 5) for Exxon versus 4.98 for Chevron. They’re just about the identical firm relating to primary statistical measures.

For the oil majors, dimension will not be their buddy. Their enormous dimension makes it extraordinarily exhausting to maneuver the needle by acquisition or profitable drilling. Additionally it is price declaring that the current route of rates of interest makes protected Treasury Notes more and more aggressive to dividend yields within the 3.5% space. Earlier than lengthy this can be an element for all shares favored by traders as bond substitutes.

For traders extra targeted on potential capital features and prepared to imagine a bit extra threat the next two shares appear extra prone to improve earnings and dividends with rising working quantity and revenue margins. Each are much less constricted by the difficulties of reserve substitute and each have the potential to take a serious leap in earnings and money move accompanied by a rise in valuation.

Occidental (NYSE:OXY): A Particular Scenario With Large Upside

Occidental has been written about often on this web site, and I actually have included it in three articles from numerous views. The foremost topics have needed to do with OXY’s success in beating out Chevron for the property of Anadarko and Buffett’s persistent shopping for of OXY shares which some see as prelude to a takeover. The present focus, nonetheless, needs to be on OXY’s transformation as an organization following the Anadarko acquisition.

Amongst oil majors, Occidental advantages by being sufficiently small that an acquisition could make a distinction. Chevron is nearly 5 occasions bigger and ExxonMobil is six occasions bigger. The acquisition of Anadarko would have had modest influence on Chevron, however for OXY it added about 70% to its reserves. The nice luck of rising oil costs exhibits simply how transformative this has been as annual revenues by means of Q2 2022 are up about 70% from 2013 when oil costs have been roughly at the moment stage.

The extra particular developments contain debt and capital construction. The Anadarko acquisition ran up OXY’s long run debt from $10.2B to about $39B plus the $9.76B most well-liked inventory held by Berkshire Hathaway. With its market cap as little as $20B for a lot of 2020 OXY regarded frighteningly leveraged. The gusher of money move during the last six months has enabled OXY to uptempo its debt discount to $8B for 2022 to this point, bringing web long run debt down to only beneath $20B. Together with rising market cap that has diminished debt as a proportion of capital (together with Berkshire’s most well-liked) to about 33% of enterprise worth, bringing credit score rankings upgrades. The plan for future debt discount is to take LTD all the way down to $18B by the tip of the 12 months and let debt roll off at maturity sooner or later.

Together with its $3B scheduled share repurchases, CFO Robert Peterson famous within the Q2 convention name that money from execution of warrants can be used for share repurchases to mitigate the rise in shares excellent. Additionally price noting is that scheduled capital expenditures for exploration and manufacturing for the rest of 2022 have been set at a minuscule $75 million for Q3 and $215 million for the second half. This can be a firm which has made its giant play for reserves and is laser targeted on speedy enchancment on capital construction and profitability. CEO Vicki Hollub reassures {that a} rising dividend can proceed if oil falls to $40 per barrel. A fast have a look at metrics for 2021 exhibits that the brand new and reworked OXY might be extremely worthwhile at oil costs much like these in 2021.

Some extent about OXY which needs to be talked about is its Low Carbon Ventures initiative with building of a carbon seize challenge scheduled for this fall as reported by SA Information. Helped partially by its modest dimension that places OXY effectively out in entrance of different built-in oil corporations. CEO Hollub appears critical about this initiative which may align OXY with the evolution of vitality sources in the long term. Hollub is an impressive no-nonsense CEO who’s attentive to particulars however also can suppose when it comes to the large image. She survived a warfare with Chevron to purchase the Anadarko property which have reworked Occidental. Her management is among the causes to really feel snug proudly owning it.

Occidental’s present SA Quant Ranking of Maintain doesn’t absolutely mirror its speedy steadiness sheet and earnings progress enchancment. The higher measures are its issue rankings of A for Progress, up from C six months in the past, and A+ for profitability. Whereas one should not usually try to entrance run Quant Rankings, potential traders ought to be aware that the gorgeous enchancment in its debt scenario because of gushing money move has taken place over about 18 months with the biggest pop within the first six months of 2022. The next Quant Ranking appears prone to comply with. Whereas I’m agnostic as regards to Buffett shopping for the entire firm (see this article) I do not rule it out. I personal OXY and charge it a Robust Purchase.

Cheniere Power (NYSE:LNG): A Area of interest Progress Firm

Should you simply have a look at the working statistics with out being instructed it is an vitality firm you may think that Cheniere is a younger tech firm with earnings and money move simply flipping from unfavorable to optimistic. Revenues have exploded together with long run debt, though debt went down a bit over the previous six months because of its tremendously elevated money move. The share rely has elevated because it does with progress corporations. Money move simply turned optimistic in 2021 and has grown explosively within the first six months in order that Cheniere now sells at about eight half of occasions free money move per share. What occurred?

The plain reply is that a lot greater gasoline costs occurred and with out something main will increase in value, greater revenues dropped to the underside line. There’s rather more to Cheniere, nonetheless. Cheniere is the biggest US firm and second largest globally within the transportation and storage of liquid pure gasoline. The gasoline disaster in Europe ensuing from the Russian invasion of Ukraine has compelled Europe to rethink its vitality insurance policies, and Germany now has six new LNG terminals within the works. As a result of European gasoline costs are greater than costs within the US this presents a chance for Cheniere.

Wonderful current outcomes clearly do not inform the entire story as Cheniere is looking for FERC approval to broaden its LNG plant in Texas. It has no actual competitor in manufacturing and transportation of LNG, together with the specialised ships required. There aren’t any current numbers for the influence this can have on future earnings and money move, however the market appears to not absolutely grasp the chances.

Cheniere has an SA Quant Rating of Maintain, which can appear beneficiant given its Issue Rankings of F for valuation, B- for Progress, and C+ for Profitability. As with OXY, nonetheless, these Rankings will quickly learn like historical historical past. Most attention-grabbing is its Quant Rating of 29 out of 61 within the Oil And Gasoline Storage and Transportation Business. Due to the current developments with gasoline provide in Europe it may be extra related to rank Cheniere 1 out of 1 or presumably 1 out of two (globally) in its specialised area of interest.

Cheniere is extra speculative than the opposite three names, however I charge it a Robust Purchase. Whereas I do not personal it, I’ll purchase it in an extra market pull again.

Backside Line

Power has been the strongest market sector for the previous 12 months and a half. Over a two-year interval the worth of the Power Choose Sector SPDR ETF rose 200% but vitality stays a small weighting within the S&P 500 given its persevering with significance to the economic system. All the shares urged above had single digit P/E ratios and single digit worth to free money move ratios. Whereas there are numerous dangers which maintain down the P/E ratios of vitality shares, their valuation appears low given the excessive chance of fine future prospects. The foremost dangers embrace a deep recession or a sudden and surprising answer to all of the world’s main issues. Take the extra pessimistic home place on that one. One may throw within the threat that vitality prices and shortages proceed and excessive vitality costs persist politicians may even see profitable vitality corporations as targets for numerous sorts of taxes.

The vitality sector has many corporations with numerous sizes and enterprise fashions. Chevron and ExxonMobil appear supreme for revenue seekers. Occidental Petroleum provides capital features as its giant makeover transforms the corporate. Cheniere is a considerably greater threat firm with fairly a little bit of debt, however excessive gasoline costs have enabled it to start paying down that debt whereas the prospect of promoting liquid pure gasoline to Europe provides a excessive upside. The core case is that Cheniere’s enterprise is ideally aligned with the present surroundings. After the lengthy run-up from 2020, traders may select to be affected person and see if the present market decline will pull the vitality sector down a bit extra and current a great dip-buying alternative. Power regardless of basic market weak point suggests vitality could effectively emerge as an enormous winner within the subsequent main bull market.

[ad_2]

Supply hyperlink