[ad_1]

syahrir maulana

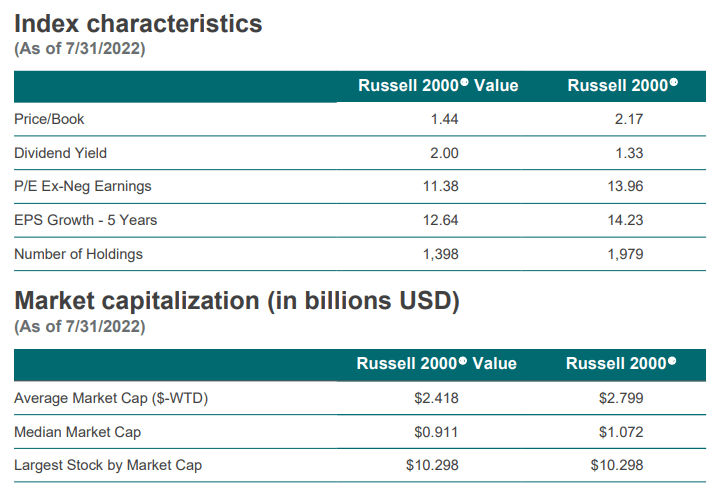

iShares Russell 2000 Worth ETF (NYSEARCA:IWN) is an exchange-traded fund whose benchmark index, the Russell 2000 Worth Index, measures the efficiency of small-cap worth shares within the U.S. fairness market. IWN basically buys shares within the Russell 2000 which might be buying and selling at comparatively low value/guide ratios, decrease two-year earnings development forecasts, and decrease five-year historic gross sales development charges. Some particulars are offered beneath, together with a value/earnings ratio of 11.38x, though this crucially excludes unfavourable earnings.

FTSERussell.com

Plenty of smaller corporations are loss making, so adjusted earnings are usually not significantly helpful for valuation functions. The truth is, the image is kind of murky on the whole for that reason. Another information supply, Morningstar, additionally appears to make use of an adjusted determine, provided that their ahead value/earnings ratio is equally low, at simply 10.52x. That may recommend, on their value/guide ratio of 1.19x, a return on fairness of about 11.3%, however that might be throughout the portfolio. That is going to be inaccurate. For instance, initially of the yr, an article within the Wall Avenue Journal reported {that a} third of the businesses within the Russell 2000 (broader index) are loss making. I might think about a better portion of the Worth phase is loss making, given the essential choice standards.

So, it’s not a very good concept to try to worth IWN in a traditional means. I’ve checked quite a few sources, and the overwhelming majority appear to regulate for unfavourable earnings. Having mentioned that, WSJ has a dwell estimate of a mean value/earnings ratio for IWN’s portfolio of 18.88x, with a mean value/guide ratio of 1.76x. It is a respectable begin. Earnings development estimates in combination by analysts (in consensus) can typically be exaggerated; nonetheless, Morningstar studies a three- to five-year earnings development potential of just about 17% per yr for IWN. This appears to contradict the choice standards of the fund although. Nonetheless, WSJ’s ratios would suggest a return on fairness within the area of 9.3%. That’s not too dangerous, and may help us type a fundamental concept of what IWN’s shares are value.

In the meanwhile, fairness danger premiums are elevated as perceived macroeconomic uncertainty is excessive. Professor Damodaran estimates that the U.S. ERP is 5.10% as of September 1, 2022. The present U.S. 10-year yield, a preferred measure of the suitable risk-free price, is 3.25% on the time of writing. IWN’s historic beta, per iShares themselves, is 1.19x. Making use of a a number of of 1.19x in opposition to the ERP of 5.10% offers us an adjusted ERP of 6.07%. Including in our risk-free price of three.25% offers us 9.32%. Let’s assume worth shares are low-growth in the long term, and rise consistent with a decrease nominal degree of inflation of circa 2%. That provides us a net-of-growth low cost price of seven.32%. Divide 1 over 7.32%, and we fetch a a number of of 13.66x.

This fundamental evaluation would suggest that IWN is on the pricier aspect. But then again, IWN’s portfolio (which by the way in which had 1,398 holdings as of August 31, 2022, which probably explains why the extent of beta is kind of low) does supply some upside potential. That’s as a result of the loss-making corporations can grow to be worthwhile, and/or they commerce on different measures past typical earnings measures (maybe on money circulate, or dividend yields). The present dividend yield per iShares for IWN is 1.95% on a 30-day SEC yield foundation. That’s not too dangerous, though it’s beneath the U.S. 10-year yield, so I might not recommend there’s a flooring to the value of IWN shares on that foundation.

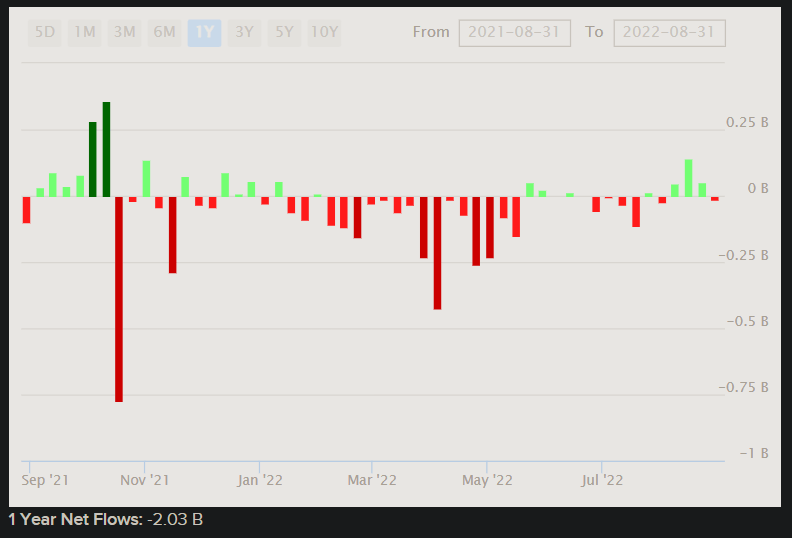

IWN had $12.1 billion in belongings beneath administration as of August 31, 2022, and that’s regardless of internet outflows of circa $2 billion over the previous twelve months or so.

ETFDB.com

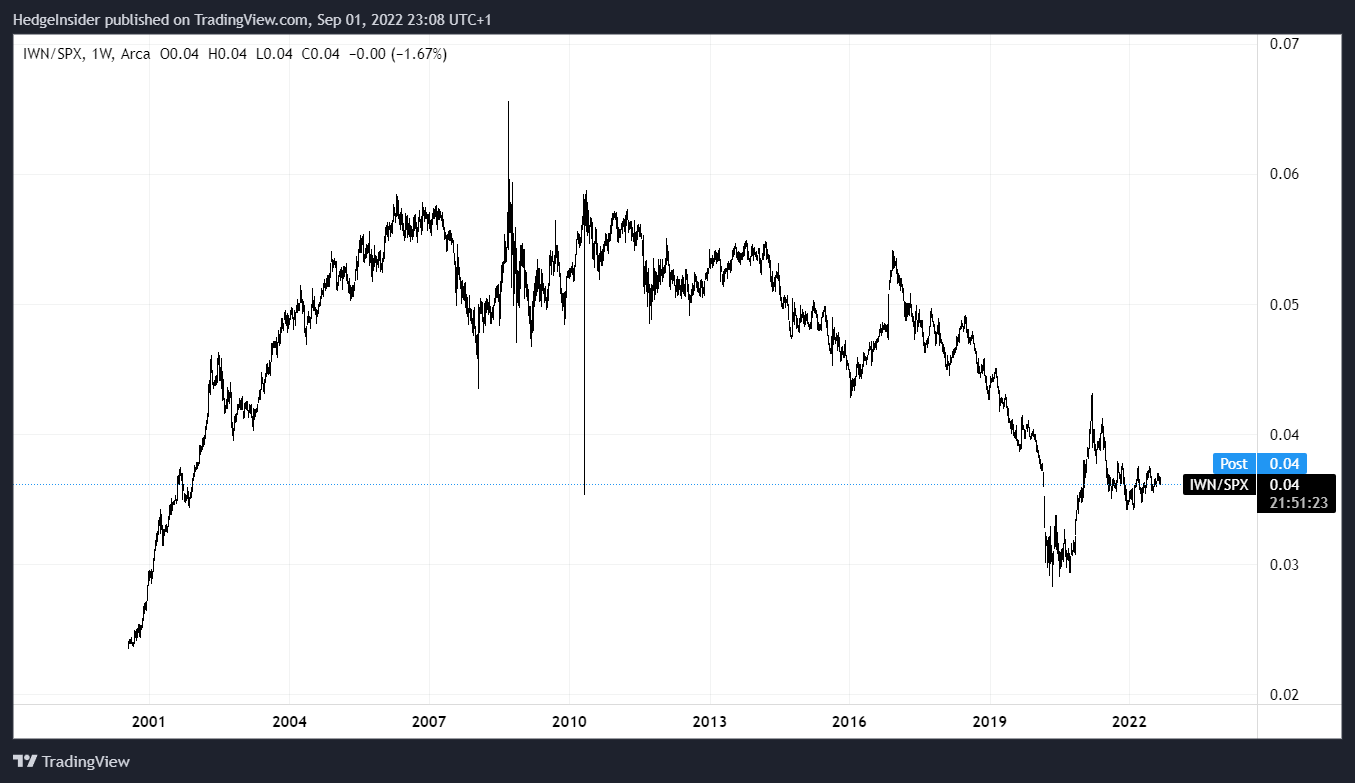

Danger just isn’t favorable in the meanwhile, however IWN has been affected by outflows for a minimum of a yr on a internet foundation. The chart beneath reveals the value of IWN by way of the S&P 500 U.S. fairness index. IWN can apparently outperform the S&P 500 earlier on within the enterprise cycle (e.g., from 2001, additionally from early 2008, and later from 2015/16, and from 2020 following the emergence of COVID-19 that induced chaos throughout the worldwide financial system and markets).

TradingView.com

Nevertheless, following a leap (early within the enterprise cycle), IWN’s capability to outperform is weaker. Additional, since 2009/10, the long-term development has been unfavourable, whereas high-performing mega-cap tech shares have taken up a a lot better proportion of the foremost U.S. fairness indices (together with the S&P 500). Danger capital tends to get pushed into these giant, liquid shares with excessive returns on fairness, not a lot riskier, small-cap shares or rising markets.

Earlier than the “tech regime” we’ve got been in for over 10 years now, the so-called “small-cap premium” has grow to be much less thrilling; the concept that small caps commerce at elevated danger premiums, and thus one can earn outsized returns if one is ready to stand up to the volatility. Rising markets additionally was once in vogue amongst pro-risk traders, however tech shares have in the end come out on prime; most particularly U.S.-based know-how corporations.

I feel given the riskier nature of IWN’s portfolio, it’s probably that long-term returns will probably be fairly good. However I feel given the long-term development whereby IWN is underperforming the S&P 500, the latter being a standard benchmark representing basically 1x beta (what must be much less risky than say, IWN), it doesn’t make a lot sense to purchase IWN over the broader indices. You tackle probably extra danger for much less return.

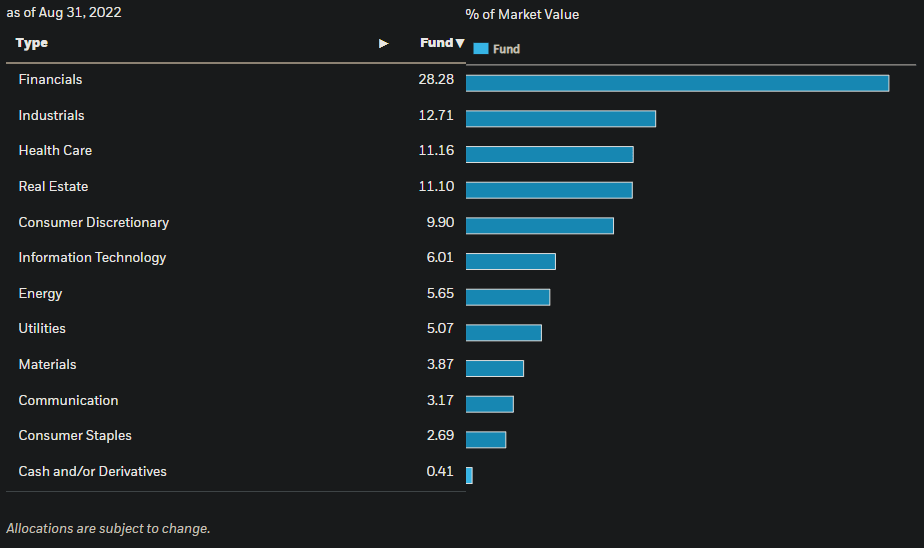

Additionally, the sector exposures are in pretty typical, mature, low-growth industries (as you’ll count on), together with Financials (28% of the portfolio as of August 31, 2022), Industrials (13%), Well being Care (11%), and Actual Property (11%). Know-how solely makes up 6% of the portfolio.

iShares.com

IWN is the sort of fund you may count on to do properly throughout instances of rising rates of interest, like now, since larger low cost charges are likely to punish higher-growth corporations (since a better proportion of their theoretical lifetime earnings are out sooner or later). Nevertheless, as my chart reveals, the IWN/SPX ratio has not budged an excessive amount of for the reason that begin of 2021 (most just lately), regardless of the U.S. 10-year yield rising throughout this era from lower than 1% to a gift 3.25%.

On an adjusted earnings foundation (value/earnings circa 10-11x on a ahead foundation), perhaps IWN is “undervalued”, however that might be giving all of the loss-making holdings credit score for future turnaround potential. Pricing IWN shares by together with unfavourable earnings (value/earnings circa 18-19x) is maybe overly pessimistic, because it assumes no development or “turnaround” potential, and I feel a lot of the level of investing in IWN is capturing the elevated danger constructed into the value given these riskier holdings. It is possible that the underlying ahead value/earnings ratio will fall someplace in between, most likely nearer to my “truthful a number of” calculation of round 13-14x.

Subsequently, I might say that in abstract, IWN might be buying and selling at near truthful worth, and anticipated returns on holding IWN over the long term (a number of years) is likely to be within the area of 9% per yr at current (whole return together with dividends), merely given elevated fairness danger premiums and present risk-free charges. Nevertheless, this assumes that we’re compensated for the extent of beta within the fund; if IWN had been to renew longer-term underperformance, returns is likely to be within the vary of 7-8.5% each year.

As rates of interest are presently rising, and will properly flip decrease into the following cycle (if or when inflationary pressures subside), and regardless since I think about these small-cap worth shares have much less pricing energy throughout inflationary instances, and moreover provided that we’re not leaping out of the early stage of a enterprise cycle, IWN doesn’t appear greatest positioned to me. I might not be bearish, however being impartial appears to make sense at this juncture.

[ad_2]

Supply hyperlink