[ad_1]

Supply: Callahan’s Peer-to-Peer Analytics

Supply: Callahan’s Peer-to-Peer AnalyticsCredit score union stability sheets realized file share development all through the pandemic, primarily pushed by authorities aid applications and elevated saving charges throughout quarantines. Regardless of file mortgage mortgage originations, mortgage stability development slowed by means of a mixture of early repayments and credit score unions promoting low-interest loans to secondary market consumers.

Within the first half of 2022 nonetheless, these tendencies have turned. After annual mortgage development outpaced deposit development within the first quarter of the yr, all eyes had been on whether or not this pattern would proceed. The mid-year numbers didn’t disappoint, with credit score union mortgage balances rising 16.2% on an annual foundation, nearly doubling the 8.2% price for shares. After all, this meant credit score union property flooded out of investments – principally extra money balances – and into loans.

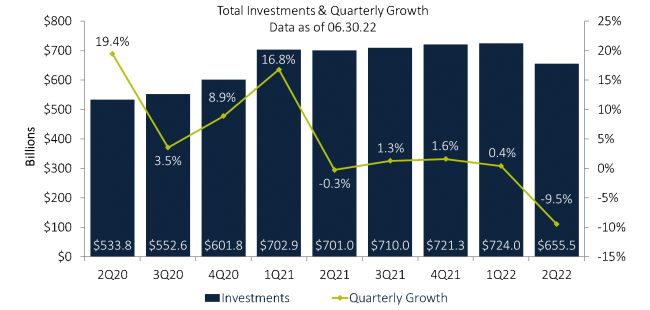

Whole Credit score Union Investments Fall 9.5%

Whole investments held by credit score unions, together with money balances, fell 9.5%, or $68.6 billion, over the previous three months to complete $655.Four billion excellent on the finish of the quarter. That is essentially the most important quarterly share decline within the final 20 years, however that superlative is deceptive with out trying on the greater image. Credit score union investments boomed prior to now two years, rising from $389.Three billion in December 2019 to a excessive of $724.Zero billion in March 2022, principally pushed by extra deposits being held as money. Even after this current decline, complete business investments are nicely above the place they stood initially of the pandemic.

Mortgage balances elevated $86.Eight billion within the second quarter, inflicting web liquidity to lower $82.Three billion. This was by far the business’s largest quarterly liquidity discount on file and was 3 times larger than the latest important drop within the second quarter of 2018. After persistent share development the previous two years, liquidity was sure to reverse ultimately. Greater prices of dwelling lowered financial savings, whereas accelerating asset value development pushed mortgage demand to file highs in greenback phrases. These dynamics pushed the loan-to-share ratio up 4.5 share factors from final quarter to 74.7%, a welcome signal for credit score union curiosity margins. Solely $7.5 billion in mortgages had been bought to the secondary market within the quarter, a 73.8% decline from the identical interval final yr. Credit score unions are holding extra mortgages on their stability sheets as increased charges make holding these loans extra engaging. All instructed, much less deposits and extra held loans goes to equate to much less property held as investments. Low-yielding money balances had been the principle casualty, as money balances fell $65.9 billion in the course of the quarter, 96.0% of the entire decline in funding balances.

Credit score Unions Favor the Entrance of the Curve

The yield curve flattened after the Fed raised charges 75 bps in each June and July. Brief-term Treasuries, that are most delicate to Fed motion, priced in expectations for added price hikes. The 2-year yield elevated 40 foundation factors in June after some dramatic intra-month swings. It settled at 2.95% at month finish after reaching as excessive as 3.45%. The market struggled to cost in each recession danger and extra Fed price will increase on the identical time, as the 2 forces counteract one another. The two-year/10-year unfold completed the month at 6 foundation factors, threatening inversion.

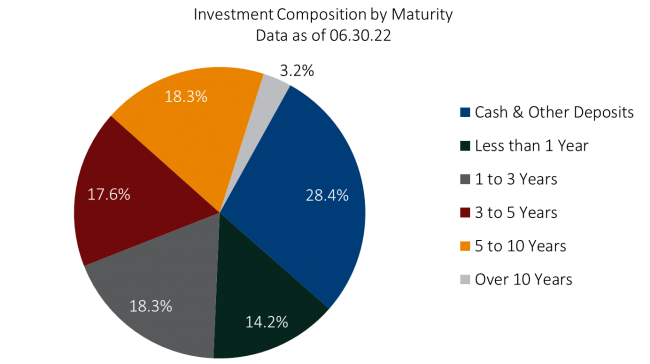

Portfolio allocators took benefit of the rise in shorter-term yields and reinvested funds into securities of extra near-term maturity. The one-to-three-year maturity class took in $4.2 billion from credit score union buyers since March, good for a 3.6% improve and sufficient to develop into the most important non-cash class. Investments in securities are unfold comparatively evenly throughout every of the maturity classes throughout the one-to-10-year vary, comprehensible given current adjustments to the yield curve. Money contains 28.3% of complete investments, down from its all-time excessive of 42.9% in March 2021. Credit score unions used these giant money balances to fund increased lending exercise in 2022, and step by step elevated their allocations to securities.

Supply: Callahan’s Peer-to-Peer Analytics

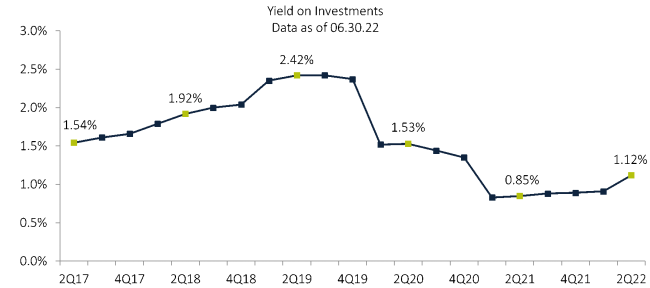

Supply: Callahan’s Peer-to-Peer AnalyticsBusiness Yield Up 21 Foundation Factors

The typical yield on investments elevated 21 foundation factors quarter-over-quarter, as much as 1.12% by means of June. Whereas this marked the fifth straight quarterly improve, it was essentially the most important change in yield because the first quarter of 2019. Declining money balances and a rising rate of interest setting pushed by the Fed had been the principle causes for the spike. This stands in marked distinction to tendencies from 2020 and early 2021, when the Fed lowered charges to spur demand and subsequently lowered yields, and deposits drove low-yielding money to file parts of the portfolio. After all, with rising yields come unrealized losses on available-for-sale securities, and these, maybe short-term, losses now complete $28.Three billion year-to-date all through the business. Wanting ahead, rates of interest are projected to extend even additional within the coming months with the Fed’s dedication to deliver down inflation.

Supply: Callahan’s Peer-to-Peer Analytics

Supply: Callahan’s Peer-to-Peer AnalyticsJay Johnson is President of Callahan Monetary Providers, Distributor of the Belief for Credit score Unions, in Washington, D.C.

Jay Johnson

Jay Johnson[ad_2]

Supply hyperlink